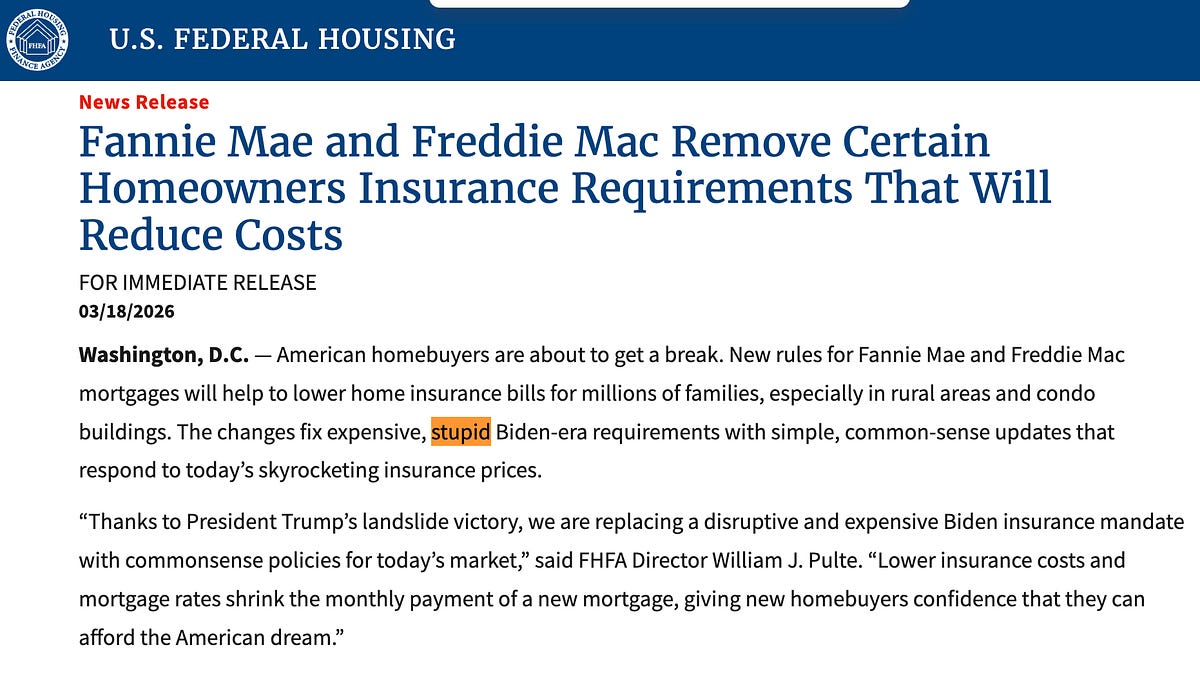

FHFA reversed its replacement‑cost homeowners insurance requirement, reverting underwriting standards to pre‑2024 rules and allowing cheaper, basic policies for some borrowers. The rollback removes a visible climate‑risk mitigation step, increasing institutional and federal exposure to weather/climate losses while offering limited real affordability relief. The move appears driven by political and industry pushback rather than actuarial or systemic‑risk solutions, signaling weaker climate oversight in housing policy.

The policy rollback is a near-term negative for homeowners insurers’ revenue mix: replacement‑cost endorsements typically carry ~10–25% higher premiums and are concentrated in newer/condo portfolios where loss-adjusted margins are highest. Pulling that business levers down will compress insurer ARPU and force carriers to either raise rates elsewhere or accept margin erosion; that transmission should show up in quarterly premium growth and loss ratios within 2–4 quarters. For the mortgage finance ecosystem the second‑order effect is asymmetric. Lower upfront insurance cost is a small, discrete affordability gain that could lift originations by a few percent in price‑sensitive pockets (2–5%) over 6–12 months, benefiting private mortgage insurers and originators, while simultaneously worsening collateral protection for agency loans — a subtle stress that widens expected-loss assumptions for MBS investors over years, not days. Politically driven regulatory backsliding raises tail risk: if a major coastal catastrophe occurs, expect abrupt re‑tightening of rules, retroactive underwriting scrutiny, and rating‑agency downgrades of insurers/reinsurers. That regime uncertainty creates a high convexity trade window — insurers and builders priced for the “optics win” now may be repriced violently on a disaster or renewed FHFA mandate within 6–24 months. Catalysts to watch: state insurance rate filings (next 3–9 months), mortgage origination data and private MI premiums (quarterly), and any congressional hearings or GAO reviews that can force a reversal. A disciplined pair approach (beneficiaries vs. exposed carriers/builders) captures asymmetric outcomes while hedging the political headline risk.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

moderately negative

Sentiment Score

-0.60

Ticker Sentiment