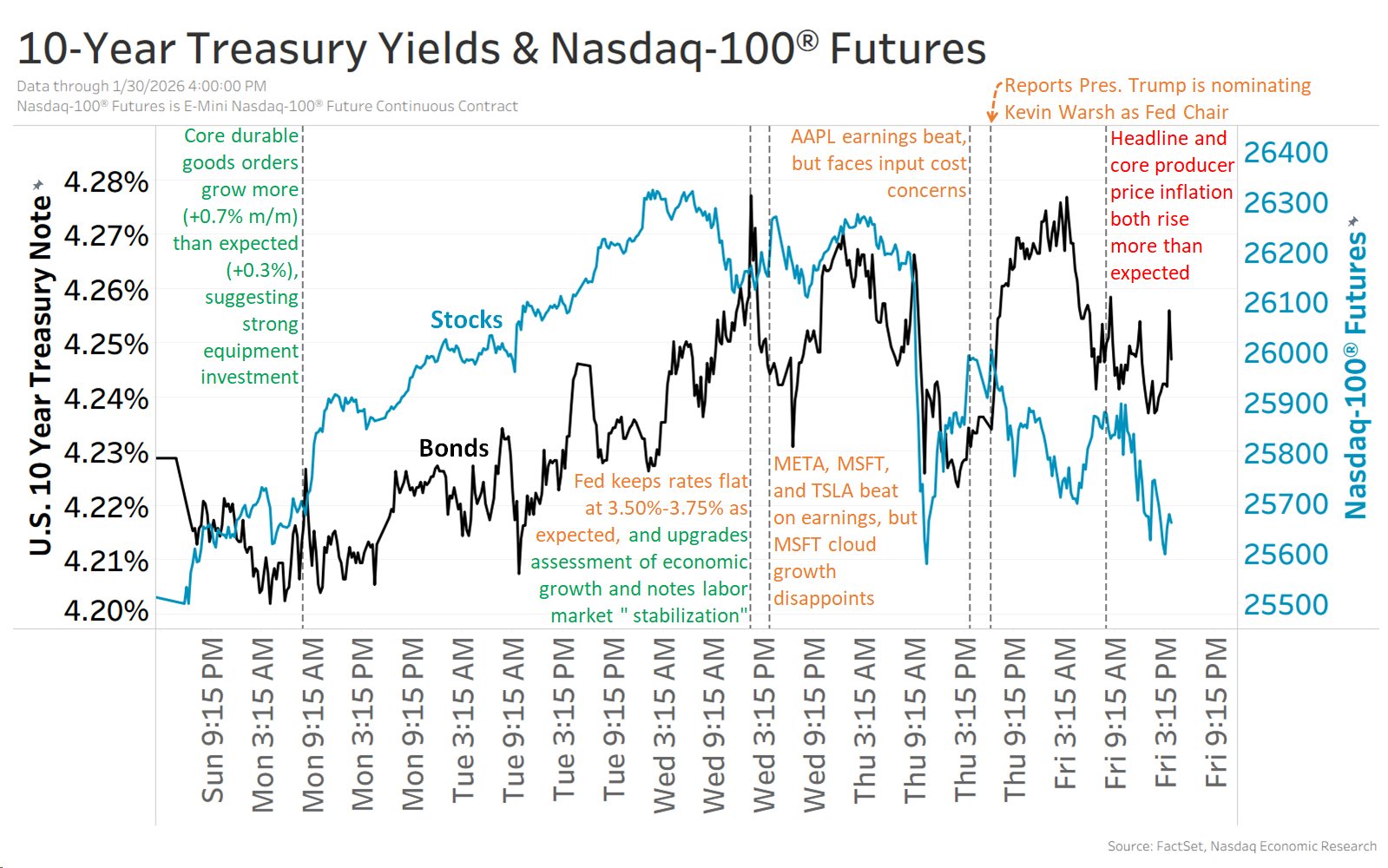

The Federal Reserve left rates unchanged but upgraded its growth assessment to “solid” from “moderate” and noted signs of labor-market stabilization, while President Trump said he will nominate former Fed governor Kevin Warsh for Fed Chair. Mega-cap results were mixed: META beat and rallied ~+10% on stronger revenue projections, MSFT beat but fell ~-10% on slower revenue guidance despite higher AI spending, and TSLA beat; the Nasdaq-100 and 10-year yield finished the week roughly flat. Key near-term market drivers include Friday’s January nonfarm payrolls, GOOG and AMZN Q4 results midweek, December JOLTS and ISM manufacturing/services data, and a possible short government shutdown.

Market structure: The week reinforces a bifurcated market — AI/ad-exposed mega-caps (META, GOOG, AMZN) and select cyclical sectors benefit from a Fed that calls growth “solid,” while firms that guided slower revenue (MSFT) are punished. Expect ad/martech pricing power to concentrate (META wins share) and cloud AI to sustain premium pricing for incumbent hyperscalers, tightening supply of high-margin capacity and keeping gross margins defended for leaders. Cross-asset: a firm growth narrative plus Fed hawkishness pins the dollar higher and keeps 10y volatility elevated; option IV on mega-cap earnings will remain rich around GOOG/AMZN prints. Risk assessment: Key tail risks are (1) a contested Fed-chair confirmation or policy shift that re-anchors hawkish policy, (2) a partial government shutdown disrupting data flow and risk appetite, and (3) disappointing AI monetization that crushes multiple expansion. Immediate drivers: payrolls and GOOG/AMZN in days; short-term (weeks) earnings re-rates; long-term (quarters) depends on measurable AI productivity (quantifiable revenue/cost offsets). Hidden dependency: strong headline AI revenue can mask increasing capex and slower free-cash-flow conversion for 2-4 quarters. Trade implications: Tactical relative-risk moves make sense: favor idiosyncratic longs in META and selective cyclicals (financials/industrials) while hedging macro with duration or index puts. Use earnings-driven option structures on GOOG/AMZN (short timing window) and size positions to 1–3% of portfolio to limit binary earnings risk. Monitor 10y yield thresholds (4.15–4.25%); a sustained break above 4.25% should trigger de-risking of duration-sensitive growth names. Contrarian angles: The market may be over-penalizing MSFT for near-term guide softness while under-discounting secular AI upside — MSFT can re-rate once cloud AI contract cadence normalizes. Conversely, META’s post-beat move may price perfection; a 10–15% pullback on any ad softness is plausible. If Warsh’s nomination leads markets to price structural disinflation from AI (6–12 months), long-duration assets could rally sharply — that scenario is underpriced now.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

0.12

Ticker Sentiment