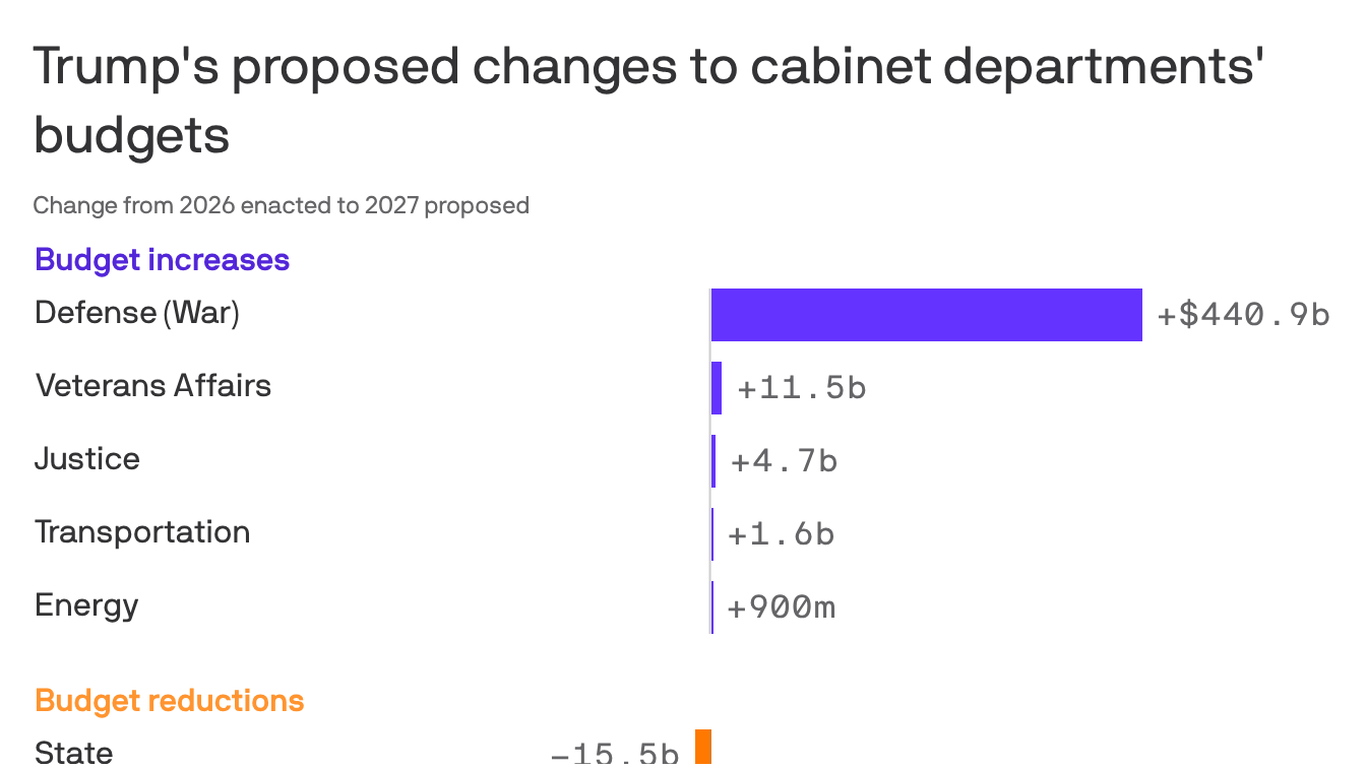

Trump's budget requests a $1.5 trillion Pentagon topline plus an extra $200 billion for Iran-related costs, boosting defense spending ~42% while cutting non-defense spending ~10% (~$73B). Steep agency cuts include EPA -52%, NSF -55%, and SBA -67%, while DOJ would rise ~13%; the plan frames cuts as fraud/waste reductions and shifts responsibilities to states. The proposal risks political backlash from working-class and older voters who rely on compressed programs and arrives amid falling approval and rising gas prices, creating potential sector rotation toward defense and broader risk-off market sentiment.

A sustained fiscal reallocation toward military capability will shift real economic activity into a multi-year procurement and industrial cycle, concentrating revenue growth at prime contractors, shipbuilders, munitions manufacturers, and upstream raw-material suppliers. Expect visible backlog growth and higher capex at suppliers within 6–24 months, with aftermarket, maintenance, and spare-parts channels generating sticky, repeatable cashflows that can support higher equity multiples even if top-line growth is lumpy. Cuts to civilian R&D and grant programs accelerate a bifurcation in technological supply chains: defense-funded, dual-use semiconductor and systems projects will retain tollbooth access to scarce specialized capacity, while commercially driven innovation dependent on public grants will see a thinner pipeline. That creates asymmetric opportunities — firms with classified IP or captive government contracts gain pricing power, and foundries/OSATs that can certify defense demand become strategic choke points over a 3–7 year horizon. The principal market risks are political and funding execution: appropriations fights, electoral backlash in affected constituencies, and a potential bond-market repricing if war-related issuance outpaces investor appetite. Near-term volatility will be driven by headlines and roll calls (days–weeks), while the durable industry winners and losers will be determined over multiple appropriation cycles (quarters–years). Reversals are plausible if the geopolitical premium collapses, bipartisan pushback forces concessions, or if higher yields choke off refinancing and M&A activity.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly negative

Sentiment Score

-0.60