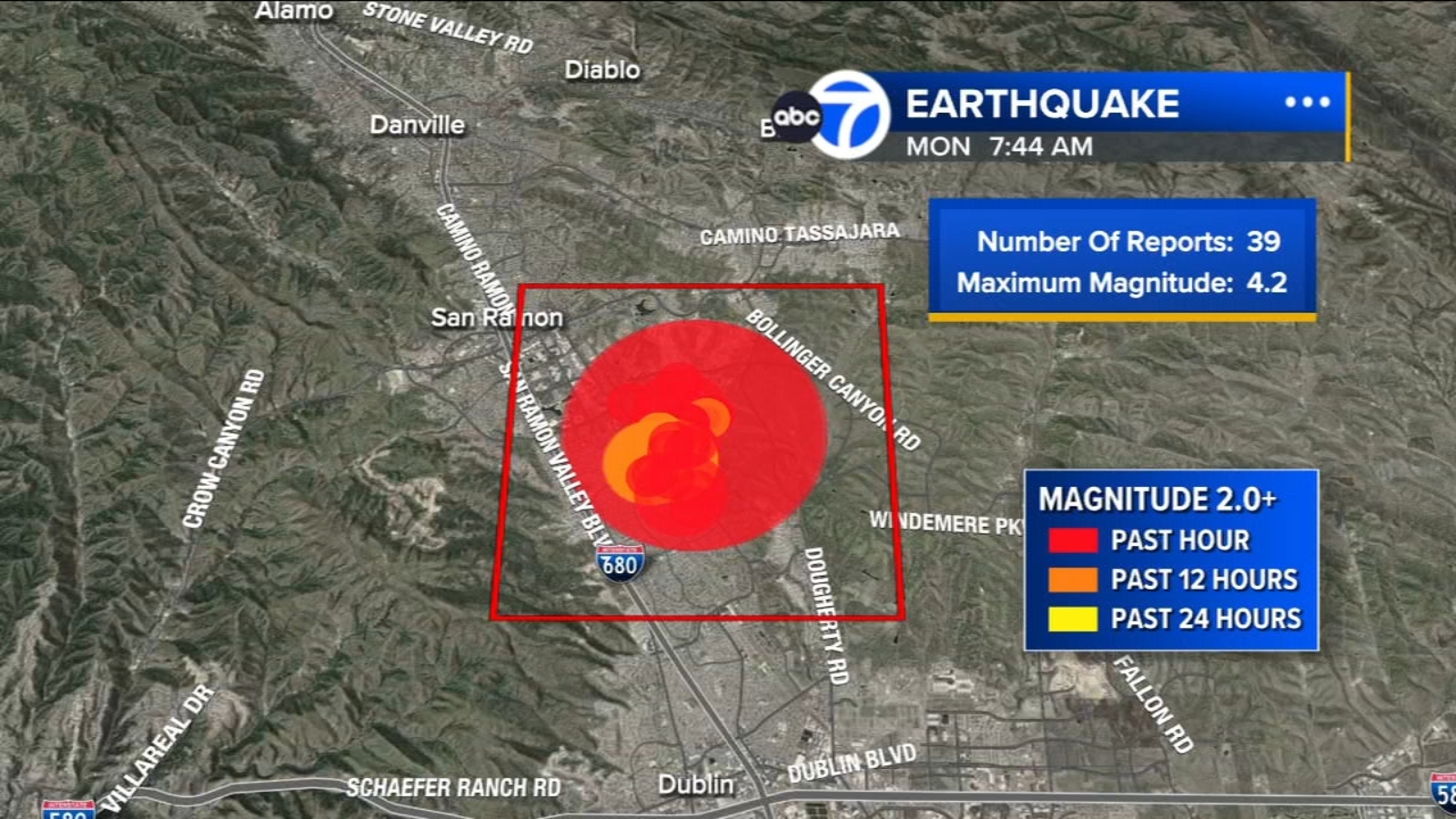

A 4.2 magnitude earthquake struck near San Ramon at 7:01 a.m. (depth ~9.4 km), following a 3.8 temblor at 6:27 a.m. and part of an ongoing swarm of more than 30 quakes in the area since November; authorities report no injuries. Local impacts included retail disruption (video shows products falling from 7-Eleven shelves) and precautionary slowdowns and inspections on BART service, implying localized infrastructure and operational checks but limited broader economic or market disruption.

Market structure: Immediate winners are home-improvement retailers (HD, LOW), seismic retrofit and civil-engineering contractors (J, ACM) and construction-materials suppliers (VMC, MLM) who can see a 5–15% demand uptick for emergency repairs and retrofits over 1–6 months. Losers are Bay‑Area‑concentrated office REITs (KRC, HPP, ARE) and small regional property insurers/reinsurers that face concentrated loss exposure and potential premium repricing. Cross-asset: expect local muni spreads to widen 5–20 bps on measured damage, a modest gold bid (+0.5–1%) on risk-off, and elevated short-dated equity IV for West‑Coast REITs and insurers. Risk assessment: Tail risk is a >6.0 quake causing >$1B insured losses and a 10–30% drawdown in local commercial real estate equities and possible muni credit pressure; probability low but non‑negligible in next 12 months given swarm pattern. Timescales: days—retail sales spikes and transit inspections; weeks–months—permitting and retrofit contract awards; quarters—insurance rate filings and municipal budget/credit impacts. Hidden dependencies include semiconductor fabs or data centers clustered in the region (operational outage risk) and reinsurance retro pricing that can amplify insurer P&L. Trade implications: Direct tactical longs: establish 1–2% positions in HD and LOW for 3–6 months to capture preparedness/repair demand; establish 0.5–1% exposure to J and ACM for 6–12 months to capture infrastructure assessment/retrofit wins. Hedges: buy 3‑month, 5–10% OTM put spreads on KRC and HPP sized 0.5–1% as insurance; alternatively buy call spreads on HD (3‑6 month). Rotate portfolio overweight into building materials/engineering and underweight Bay‑Area office REITs and small regional P&C insurers. Contrarian angle: Market may underprice sustained retrofit capex and regulatory tightening—passage of municipal retrofit funding or state grants (trigger) could lift J/ACM/MLM 10–25% over 6–12 months; conversely, if the swarm dissipates with no >5.5 event within 30–60 days, short-term retail and HD/LOW pops may fade. Use event thresholds (>=5.5 quake or >100 quakes in 30 days) to scale exposure up or down and set stop-losses at 5–10% on tactical longs to avoid mean-reversion.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

-0.05