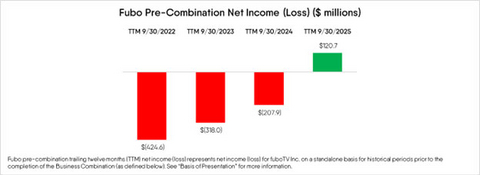

Fubo targets Pro Forma Adjusted EBITDA of $80–100M in Fiscal 2026 (midpoint $90M) and at least $300M in Fiscal 2028, implying >80% CAGR from 2026 to 2028. The company expects to be Free Cash Flow positive starting Fiscal 2027, to end FY26 (YE Sep 2026) with at least $200M in cash, and reports ~$323M of debt with no maturities until 2029 (2029 bonds trading near par). Management signals no planned equity raises through FY2028, cites contractual wholesale fee step-ups with Hulu as a key earnings driver, and highlights $59M Pro Forma Adjusted EBITDA and $(178)M Pro Forma Net Loss in Fiscal 2025 as a base.

Fubo’s trajectory shifts the bargaining leverage in streaming economics: a credible path to sustainable cash generation changes counterparty incentives during content renegotiations and ad-revenue commercialization. Rights holders and regional sports networks will face a more nuanced trade between extracting higher fees now versus broader distribution and revenue share arrangements; that dynamic should pressure smaller, fee-dependent incumbents and create arbitrage opportunities for scale players that can reprice bundles. Credit markets are likely to re-evaluate tail risk before public equity does — reduced near-term refinancing pressure and extended maturities make credit-sensitive investors more willing to tighten spreads, but any slip in execution (ad-server migration, integration of ad stacks, or missed contract rollovers) will be priced into both bonds and equity quickly. Important timing windows: near-term catalysts include the upcoming earnings cadence and ad-migration milestones (weeks-to-months), while content-renegotiation benefits will materialize over multiple contract cycles (quarters-to-years). Consensus underestimates the impact of a smaller publicly tradable float and a strategic push to cross-sell a larger bundled service: retail concentration from corporate actions can amplify volatility and make short-term squeezes more likely, while institutional acceptance should be gradual and conditional on repeatable GAAP improvement. The real inflection is execution risk — if management delivers predictable FCF conversion and demonstrable content-cost alignment, downside risk compresses materially; failure on any major integration front reverses sentiment rapidly.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly positive

Sentiment Score

0.70

Ticker Sentiment