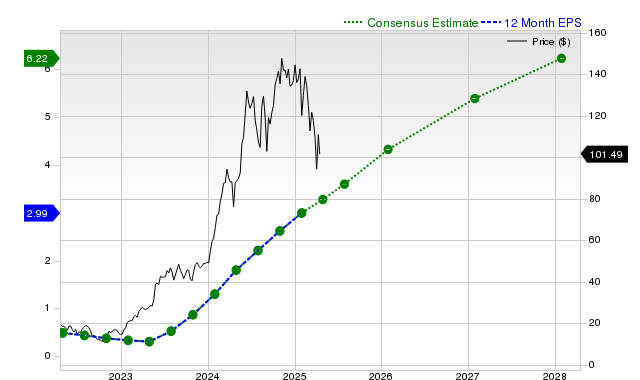

NVIDIA (NVDA) has significantly outperformed the S&P 500, returning +11.4% over the past month, fueled by strong projected earnings and revenue growth. Current quarter EPS is estimated at $0.99 (+45.6% YoY) and sales at $45.69 billion (+52.1% YoY), supported by recent positive analyst estimate revisions. While the company has consistently exceeded revenue estimates, its Zacks Rank #3 (Hold) suggests near-term performance may align with the broader market, and a Zacks Value Style Score of 'D' indicates it trades at a premium.

NVIDIA (NVDA) has demonstrated significant recent market outperformance, with its shares returning +11.4% over the past month, nearly double the Zacks S&P 500 composite's +6% gain. This momentum is supported by exceptionally strong forward-looking fundamentals, with sell-side analyst consensus projecting substantial growth. For the current quarter, earnings are forecast to increase by 45.6% year-over-year to $0.99 per share, while revenues are expected to grow 52.1% to $45.69 billion. These projections have seen positive revisions over the last 30 days, a key indicator of strengthening business trends. Historically, the company has consistently beaten revenue estimates for the past four quarters, though it notably posted an EPS surprise of -4.71% in its last report. Despite this powerful growth narrative, there are significant countervailing factors. The stock's valuation is a primary concern, as reflected by its Zacks Value Style Score of 'D', indicating it trades at a premium to its peers. Furthermore, its Zacks Rank of #3 (Hold) suggests that in the near term, the stock may perform in line with the broader market, implying that the robust growth expectations could already be priced in.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

0.25

Ticker Sentiment