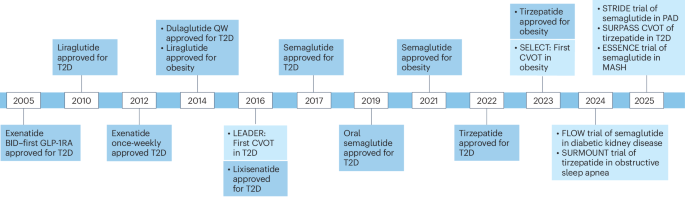

GLP-1–based medicines are described as transforming treatment for type 2 diabetes, obesity and multiple comorbidities, with newer molecules (including high-dose semaglutide, tirzepatide and multi-receptor agonists such as retatrutide) showing greater weight loss and expanded indications across cardiovascular, renal, hepatic, neurodegenerative and substance‑use disorders. The review highlights multiple positive phase‑2/3 signals (cardiorenal and metabolic benefits), ongoing trials and regulatory follow-ups, alongside safety and tolerability uncertainties (gastrointestinal effects, psychiatric signals, reproductive safety) that will shape labeling and uptake—implications that could materially expand the addressable market for leading developers (eg, Novo Nordisk, Eli Lilly) if ongoing pivotal readouts and regulatory outcomes remain favorable.

Market structure: Leadership in GLP‑1s is consolidating around market leaders (Novo Nordisk (NVO) and Eli Lilly), creating a concentrated oligopoly where the top two could capture >50% of weekly GLP‑1 revenue by 2026. Direct beneficiaries include peptide CDMOs, specialty pharmacies and leading label-holders; losers include insulin‑pump players (PODD), some legacy diabetes franchises and elective bariatric providers as medication adoption substitutes surgery. Cross‑asset: expect modest FX strength in DKK/USD on NVO flows, slight downward pressure on food/restaurant discretionary demand over years, and a small risk‑off bid in short-term sovereigns if headline safety/regulatory shocks hit the sector. Risk assessment: Primary tail risks are regulatory/safety (psychiatric, retinal, pregnancy signals) that could impose label changes and a 10–30% revenue hit in 3–12 months, and payer reimbursement pushback that could reduce realized prices 20–40% vs consensus over 1–2 years. Operational bottlenecks (manufacturing shortages) can cap quarterly growth by ~20–30% and create temporary pricing power; legal/class suits around off‑label use are a latent 12–36 month tail. Key catalysts: upcoming cardiovascular, NASH and payer policy readouts in next 3–12 months; absence of favorable outcomes would materially compress multiples. Trade implications: Tactical overweight NVO (equity + options) to capture near‑term rollout and labeling expansion, funded by trimming/shorting PODD and legacy large‑cap pharma exposure (PFE, SNY) that lack direct GLP‑1 leverage. Use 3–9 month option structures to time around trial/payer milestones: buy call spreads to limit premium and buy short‑dated puts as event hedges. Sector rotation: shift 1–3% from broad pharma into CDMOs and specialty distribution over the next 4–12 weeks; hold plays 6–12 months and re‑assess after major trial or reimbursement outcomes. Contrarian angles: Consensus underestimates payer resistance and adherence attrition — real-world discontinuation could shave 15–30% off long‑run TAM; conversely, supply scarcity could sustain premiums and margin expansion for leaders. Historical parallels: rapid adoption then payer pushback mirrors PCSK9 dynamics — initial multiple expansion can reverse sharply post‑coverage limits. Unintended consequences: safety headlines (even low incidence) have outsized equity impact; structure trades to capture upside but cap left‑tail losses.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.45

Ticker Sentiment