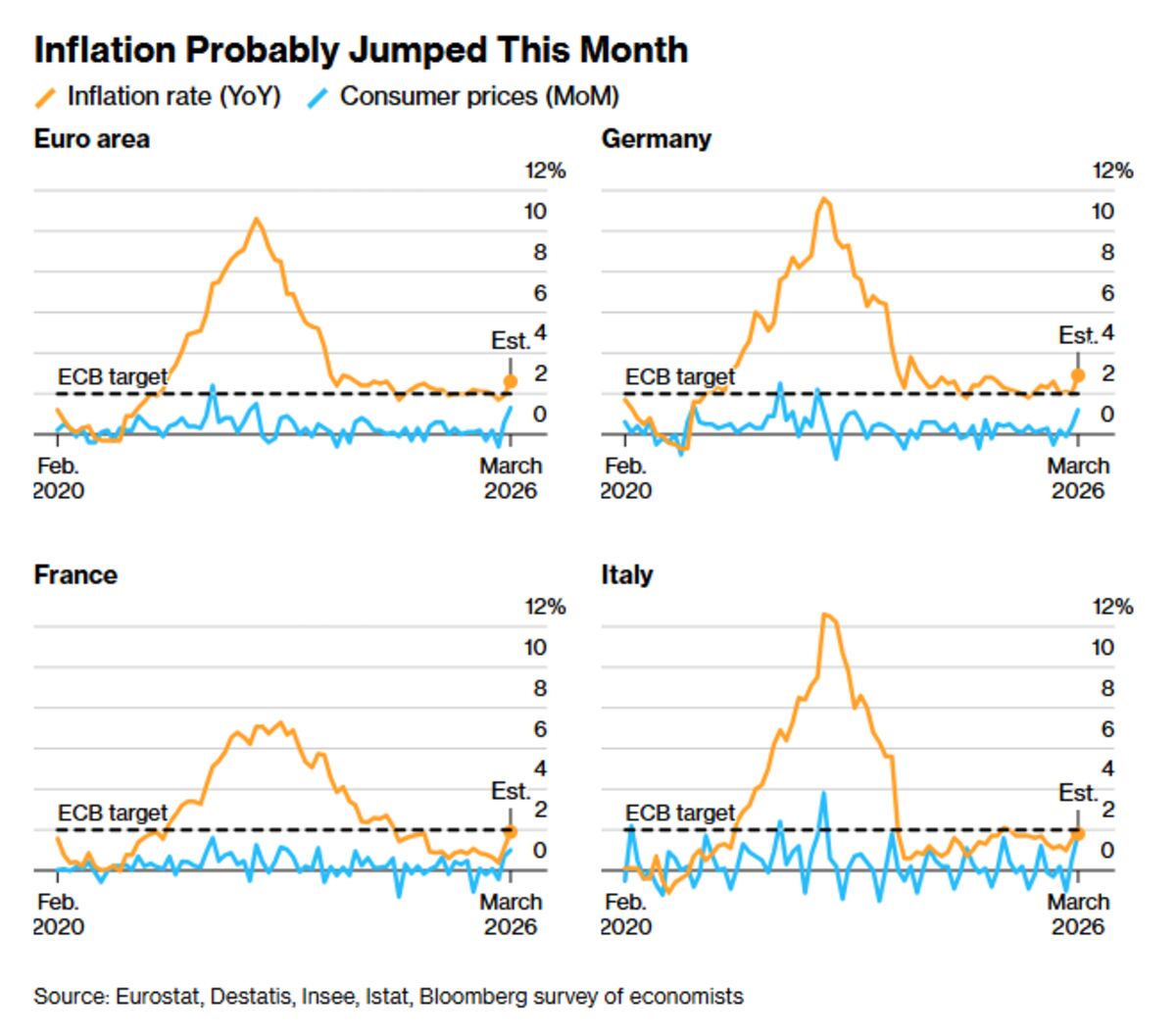

Euro-zone consumer-price growth is seen to have surged by 0.7 percentage point in the first batch of March G-20 data — the largest monthly jump since Russia's 2022 invasion — driven by fallout from the Middle East conflict and a US attack on Iran. The unexpected inflation spike heightens upside risks to inflation, could push the ECB toward a hawkish stance and may trigger risk-off moves across markets.

This shock behaves like a supply-side cost-push that will amplify near-term headline prints while forcing a policy arithmetic problem for the ECB: stickier inflation increases the odds of a renewed tightening bias within 3–6 months even as growth slows. Mechanically, higher imported energy raises input costs for manufacturing and services with a 4–8 week lag into producer prices, then another 6–12 weeks into consumer services where pass-through is highest, which keeps core inflation elevated beyond headline volatility.

Second-order winners include large integrated energy majors with European-centric upstream exposure and banks with repricing power on new loans; losers are net energy importers, low-margin exporters and households carrying variable-rate mortgages. Expect sovereign spread dispersion to widen — Italy and peripheral financing costs are most sensitive to a persistent ECB/real-yield rerate, which can feed back into bank capital and corporate credit spreads over 1–12 months.

Near-term risk is geopolitical de-escalation or coordinated release of oil reserves which would reverse the cost shock in days–weeks; medium-term risks are wage-price feedbacks and fiscal loosening that would entrench inflation, pushing the ECB into a higher-for-longer regime over 6–18 months. Watch three catalysts with tight calendars: the next ECB minutes (weeks), April/May labor prints (1–2 months), and any OPEC+ operational statements (days–weeks) — each can flip the policy and FX trajectory rapidly.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mildly negative

Sentiment Score

-0.35