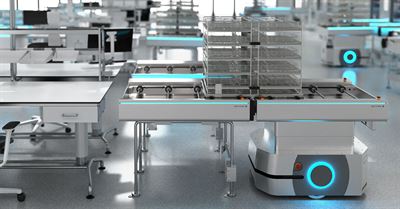

Getinge unveiled Automatiq, a modular family of automated sterile-reprocessing solutions combining a self-navigating mobile robot (Envoy), an intelligent buffer/workstation (Depot), Loaders compatible with Getinge’s 8668 Washer-Disinfector and GSS67H Steam Sterilizer, and Automatiq Hub software with T‑DOC integration to improve workflow efficiency, traceability and ergonomics in CSSDs. The launch broadens Getinge’s product portfolio and addresses hospital logistics and labor challenges worldwide, though no financial guidance or revenue figures were disclosed so near-term market impact on earnings is likely limited.

Market structure: Getinge's Automatiq creates a narrow but high-value niche — modular CSSD automation — that should boost Getinge's serviceable obtainable market in EMEA/APAC by 3–7% over 2–4 years if adoption follows typical capital-equipment replacement cycles. Direct winners: Getinge (GETIB.ST), industrial-robotics suppliers (e.g., ABBN.SW, KUKA.DE) and software/traceability vendors; marginal losers: low-skilled CSSD labor providers and legacy manual reprocessor makers with >20% revenue tied to manual workflows. Pricing power will be modest initially (pilot-driven), but recurring software and service contracts could lift gross margins 150–300bps over 3 years. Risk assessment: Key tail risks include a regulatory recall or infection incident from automation (probability low but impact high — potential >10% revenue hit and reputational damage), long hospital CAPEX cycles (adoption lag 12–36 months), and third-party integration failures with major HIS/traceability systems. Hidden dependencies: success hinges on hospital procurement budgets and T-DOC/IT integrations; a recession or tighter hospital budgets could delay rollouts by 6–12 months. Catalysts: multi-hospital pilots converting to contracts, published LOS/efficiency data showing >10% time savings, or EU procurement wins within 3–6 months. Trade implications: Tactical long GETIB.ST exposure is warranted but size it modestly (2–3% of equity risk) and scale only after 3–5 confirmed pilot-to-order conversions within 6 months; consider a defined‑risk options structure (buy 9–12 month call spread 15–30% OTM). Complement with 1–2% long in ABBN.SW or KUKA.DE to capture hardware content uplift over 12–24 months. Consider a small pair trade long GETIB.ST / short STE (Steris, NYSE:STE) 1:1 to express EMEA/APAC automation beta vs US-centric sterilization incumbents; use 10% stop-loss. Contrarian angles: Consensus will overestimate rapid adoption; most hospitals have 18–36 month procurement cycles so early revenue beats are unlikely — this argues scaling positions only after verifiable order flow (threshold: ≥5 medium/large hospital contracts or a single national procurement win). Also watch unintended consequences: automation could increase service revenue concentration risk ( >25% installed base under single software platform) and create single-point-of-failure vendor risk that could compress valuations if not diversified. Historical parallel: early OR-automation rollouts produced positive long-term returns but 12–24 month revenue volatility during installation and validation phases.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.32