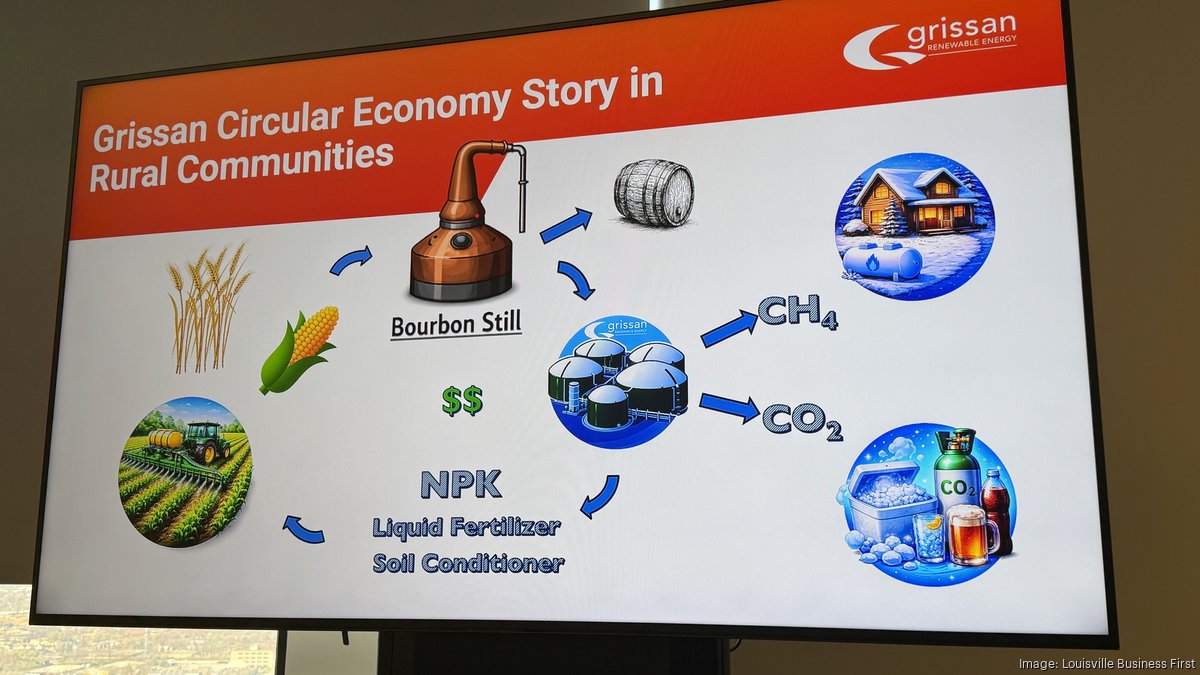

The Scotland-based firm is investing $62.7 million to build/upgrade a Marion County facility to convert bourbon byproducts into renewable natural gas, supplying energy for thousands of homes. The project represents a circular-economy, RNG-scale investment with modest regional energy supply and ESG benefits rather than market-moving implications.

This bourbon-byproduct-to-RNG conversion is more than a single project win; it exemplifies how low-value organic waste plus existing tipping fees and carbon/low‑carbon fuel credits can create negative‑cost or at‑cost RNG feedstocks that are replicable across food & beverage clusters. Over 12–36 months expect a wave of similar brownfield installs (distilleries, breweries, food processors) because the incremental capital intensity of anaerobic digestion + upgrading is moderate relative to long haul pipeline economics and benefits from localized off‑take and LCFS/45Q style credits.

Second‑order winners include RNG upgrading OEMs, local compressor/injection contractors, and regional CNG/LNG truck fuel hubs — the project converts a variable liquid mash into pipeline‑quality gas, creating demand for modular purification and interconnection services that incumbents aren’t staffed to supply. Conversely, thin‑margin local gas LDCs could see load erosion in heating/transport niches and margin compression in states with aggressive RNG credits, while long‑haul pipeline volumes are largely insulated short term but vulnerable at scale.

Key risks: project execution (feedstock variability, H2S/contaminant spikes), grid interconnection permitting and intertie capacity, and policy shifts that reduce LCFS/45Q value; any of these can flip IRRs within quarters. Catalyst cadence: construction and offtake announcements over 3–12 months, regional policy updates and credit price movements over 6–18 months, and measurable demand displacement in local gas offtake after 12–36 months.

Contrarian read: the market underestimates speed of scale because operators can cluster projects to share upgrading/compression and capture economies of scale, lowering breakevens toward $3–4/MMBtu equivalent — this makes RNG not just a premium green fuel but a disruptive lower‑cost localized substitute in transport and heating niches if credit stacks remain intact.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.30