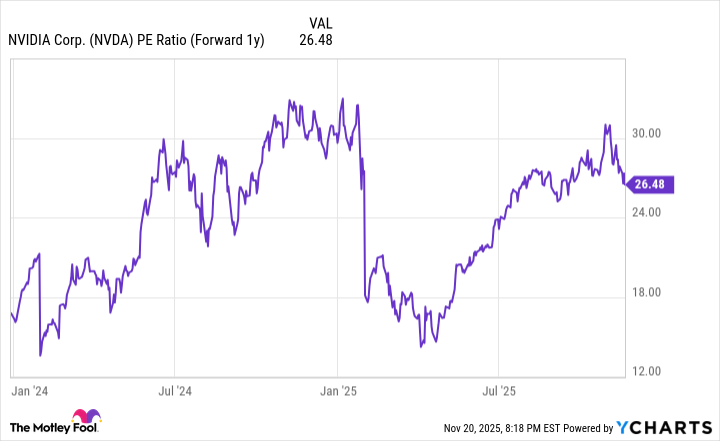

Nvidia reported Q3 revenue of $57 billion (above management guidance of $54 billion) with data-center sales of $51.2 billion, up 66% year-over-year, and projected Q4 revenue of $65 billion. CEO Jensen Huang said Blackwell GPUs and cloud GPUs are sold out, and Blackwell chips are being manufactured at TSMC's Arizona facility—reducing tariff exposure and tightening supply control. Nvidia trades at roughly 26.5x next-year earnings, comparable to large-cap peers despite materially faster growth, and management forecasts global data-center capex of $600 billion in 2025 and $3–4 trillion by 2030, underpinning continued demand.

Market structure: The scale-up of AI compute concentrates economic surplus with incumbent GPU/IP holders and advanced foundries, increasing pricing power for market leaders and upstream fabs while compressing margins for second-tier GPU makers and legacy CPU suppliers. Tight supply windows imply demand outstrips near-term capacity, supporting higher ASPs and multi-year contracted cloud spend; expect semicap and specialty materials to see sustained revenue growth over 6–24 months. Cross-asset: risk-on flows should compress IG spreads and lift tech equities; expect greater equity beta vs. bonds, modest USD strength via yield differentials, and incremental commodity demand for copper, silicon wafers and specialty gases over 3–12 months. Risk assessment: Key tail risks are intensified export controls/regulatory divestitures, a TSMC Arizona yield shortfall, or a major software adoption slowdown that reduces incremental compute intensity — each could cut TAM growth by >20% over 12–36 months. Immediate horizon (days) is volatility around guidance and order-book color; weeks–months hinge on capex cadence from cloud providers; long-term (3–7 years) depends on ecosystem monetization and alternative architectures. Hidden dependencies include cloud provider mix-shifts, customer multi-sourcing, and AI software economics that can flip unit demand dynamics quickly. Catalysts to watch: major cloud capex releases, TSMC capacity announcements, and regulatory filings over the next 30–180 days. Trade implications: Allocate risk to direct leaders while hedging operational concentration: stagger buys into NVDA via equity and LEAP calls, hedge with put spreads, and overweight advanced foundry/semicap names (TSM, ASML, LRCX) for 6–24 months. Relative-value: long leader vs. short smaller GPU peer (e.g., NVDA long / AMD short) on a 1:1 dollar basis for 6–12 months to capture share-shift; use 3–9 month call spreads to express near-term upside while selling premium when IV is rich. Rotate out of non-AI-adjacent hardware and diversify into software stacks and cloud infrastructure names to reduce single-supplier risk. Contrarian angles: Consensus underprices concentration and execution risk — market assumes linear capex cadence and consistent yield gains; a 15–25% downshock to revenue growth is plausible if cloud providers pause spend or diversify vendors. Reaction may be underdone in smaller suppliers that will lose leverage, creating short opportunities; conversely, some suppliers (TSM, ASML) may already price in excess optimism, so trim if they rally 20%+ without incremental capacity confirmations. Historical parallels to prior hardware booms show rapid margin reversion once competition or regulation emerges; position sizing must account for asymmetric downside from single-vendor exposure.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

strongly positive

Sentiment Score

0.75

Ticker Sentiment