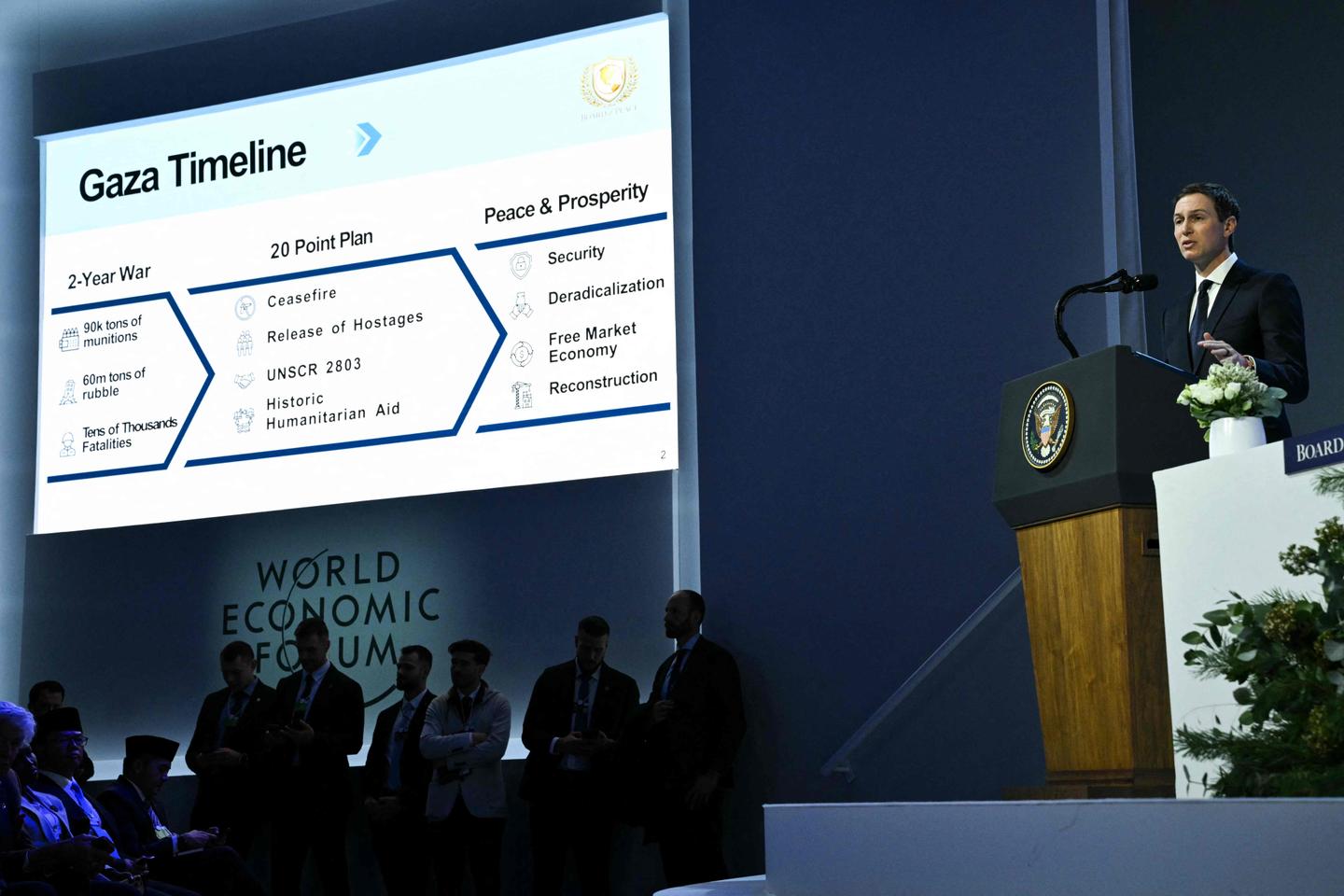

At the Davos inauguration of a U.S.-led 'Board of Peace' to oversee Gaza reconstruction, President Donald Trump and a small group of 18 founding members (from roughly 60 invited countries) presented the initiative, naming Bulgarian diplomat Nickolay Mladenov as on-the-ground representative and Ali Shaath to lead Palestinian technocrats managing day-to-day affairs. Attendance included leaders from Argentina, Hungary, Kosovo and several Arab states, with Pakistan and Indonesia represented and a proposed international force still lacking a firm timetable; notable invitee Alexander Lukashenko accepted but did not attend. The gathering highlights a U.S.-driven, politically charged reconstruction effort with uncertain international buy-in and operational timelines.

Market structure: Reconstruction governance centered on a politically fraught international “Board” creates demand hotspots: heavy materials (cement/aggregates, steel), energy services (power, pipelines), logistics and private security. Expect concentrated multi-year procurement cycles worth potentially $5–50+ billion per large donor bloc; beneficiaries include global materials suppliers and defense/security integrators with government contracting capacity, while regional consumer-facing sectors and undercapitalized local banks face disruption and credit stress. Risk assessment: Tail risks are high: renewed hostilities, unilateral sanctions, or withdrawal of Gulf funding could wipe out near-term contract pipelines. Immediate market impact is likely muted (days), medium-term (3–12 months) volatility will increase around funding pledges and contract awards, and long-term (1–3 years) winners depend on which bidders (Western vs. Chinese/ regional firms) capture scope; watch for graft/legal disputes and insurance/non-payment risk. Trade implications: Tilt into materials (CRH, VMC, MLM) and defense/security (LMT, RTX, LHX) for 6–24 month exposure; use options to cap downside and express asymmetric upside (6–12 month call spreads). Hedge tail risk with short-duration USTs and a small EM downside hedge (EEM puts or sovereign CDS) sized to 1–2% of AUM. Contrarian angles: Consensus assumes Western-led procurement — underappreciated is likely dominance by regional/Chinese contractors, which benefits commodity suppliers over marquee Western builders and creates reputational/legal risk for some U.S. names. Mispricings may appear in reinsurers/insurers and regional bank credit; act on funding-confirmation catalysts rather than headline noise.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.00