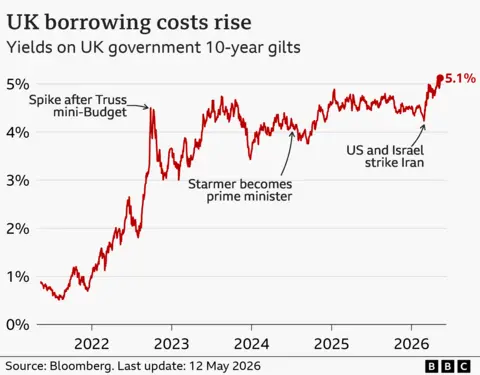

UK 10-year borrowing costs briefly hit 5.13%, while 30-year gilt yields reached 5.80%, the highest since 1998, as investors reacted to uncertainty over Sir Keir Starmer's future and fears of looser fiscal policy. The FTSE 100 fell 0.5% and the pound dropped 0.5% to $1.35, with markets also pressured by higher oil prices above $100 a barrel and renewed inflation concerns. Analysts warned that a leadership change could push UK borrowing costs higher and weaken sterling as investors demand a larger risk premium.

This is less a simple duration shock and more a credibility shock to the sovereign risk premium. When a G7 issuer starts trading like a higher-beta credit, the first-order move in gilts can quickly spill into the private cost of capital: mortgage rates, bank funding, and refinancing terms for utilities, infrastructure, and REITs all reprice off the long end with a lag of weeks to months. The 30-year move matters most because it signals investors are demanding compensation not just for near-term inflation, but for a structurally higher path of fiscal supply. The clearest second-order loser is UK financials: not because of direct sovereign exposure, but because policy uncertainty compresses multiples and raises the odds of sector-specific levies, especially if the political narrative shifts toward “fairness” measures. Domestic banks and rate-sensitive lenders are vulnerable to a bad mix of slower mortgage origination, higher deposit costs, and weaker fee income if housing activity cools. Meanwhile, UK small caps and domestically oriented cyclicals face a double hit from both tighter financial conditions and lower consumer confidence, while exporters with overseas revenue can partially offset the FX drag. The market may be underpricing how quickly a weaker pound can become a macro stabilizer. Sterling depreciation helps imported inflation, but it also improves the earnings translation for global FTSE constituents and can attract real-money inflows into large-cap UK multinationals once the political dust settles. The key contrarian point is that this may be a headfake unless leadership risk translates into an actual fiscal pivot; if that does not happen, the move in gilts could mean-revert sharply once the market sees continuity in budget discipline. Catalysts are front-loaded over days to weeks: leadership headlines, any statement on fiscal rules, and the next inflation/rates print. Over months, the real driver is whether the Treasury is forced into either tighter spending or higher issuance; if neither changes materially, the current risk premium can unwind. The tail risk is that markets start treating the UK as the test case for post-war fiscal slippage in a high-rate world, which would keep term premia elevated even if the PM noise fades.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly negative

Sentiment Score

-0.55