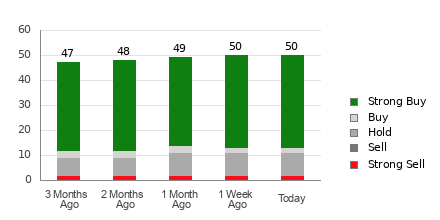

Salesforce.com (CRM) currently holds a bullish Average Brokerage Recommendation (ABR) of 1.56, indicating a strong buy consensus from 50 firms. However, the article cautions against relying solely on ABRs, citing inherent positive bias from brokerage firms' vested interests and their limited success in predicting stock movements. It advocates for the Zacks Rank, a quantitative model driven by earnings estimate revisions, which currently assigns CRM a #3 (Hold) due to unchanged consensus earnings estimates of $11.3 for the current year. This suggests that despite the bullish ABR, CRM's near-term performance may only align with the broader market.

Salesforce.com (CRM) presents a conflicting investment picture, characterized by a significant divergence between sell-side sentiment and underlying earnings estimate momentum. The stock garners a highly bullish Average Brokerage Recommendation (ABR) of 1.56, with 37 out of 50 contributing firms rating it a "Strong Buy." However, this qualitative optimism is not substantiated by quantitative data, as the Zacks Consensus Estimate for current-year earnings has remained unchanged at $11.3 over the past month. This lack of upward earnings revisions, a key driver of near-term stock performance, has resulted in a neutral Zacks Rank #3 (Hold). The analysis suggests that the strong buy recommendations may reflect inherent positive bias from brokerage firms rather than a fresh fundamental catalyst, leading to the conclusion that CRM's near-term performance is more likely to be in line with the broader market, a far more tempered outlook than the ABR implies.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly negative

Sentiment Score

-0.30

Ticker Sentiment