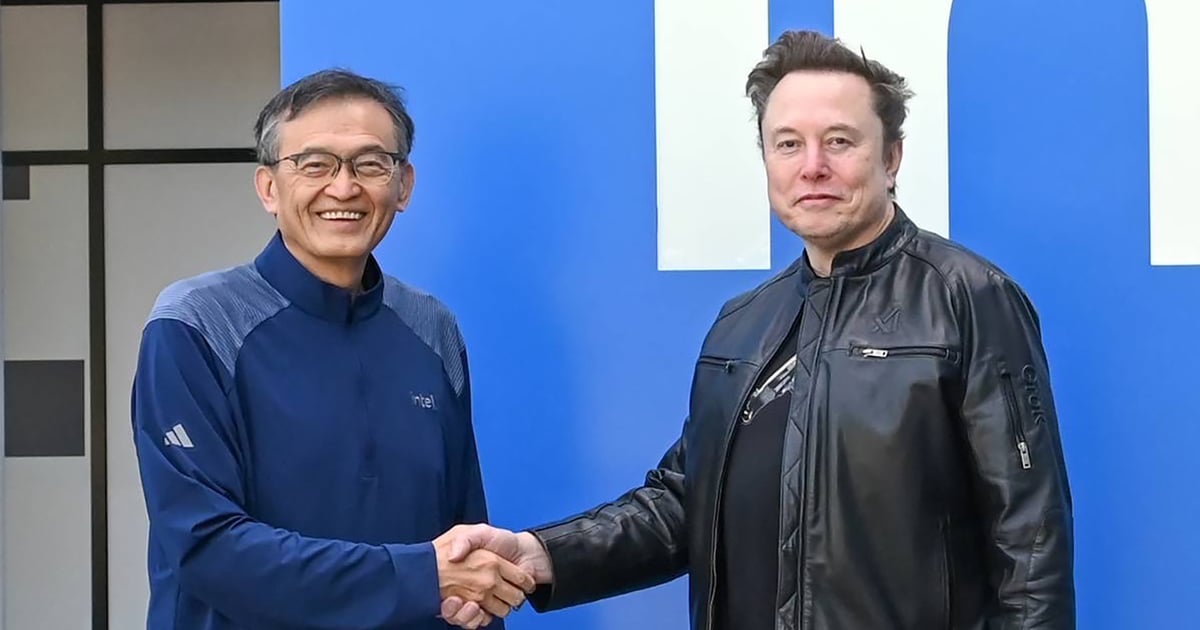

Intel announced it is joining Elon Musk’s Terafab initiative to help “refactor silicon fab technology” and support a target of producing one terawatt of compute annually for AI and robotics. The partnership signals a strategic shift toward vertical integration—aligning chip design, fabrication and packaging with end demand—which could materially reshape AI infrastructure but requires extraordinary capital, supply-chain coordination and execution discipline. Intel brings rare U.S. fabs expertise, but the move ties the company to a high‑risk, long‑timeline bet (and follows governance turmoil after CEO Pat Gelsinger’s 2025 ouster); space-based compute goals remain speculative and far-term.

The strategic pivot from buying scarce GPU hours to owning production implies a multi-year capital and contracting cycle that will reprice where AI margin accrues. Building leading-edge fabs plus advanced packaging capacity at scale is a multi-decade cashflow decision; rough order-of-magnitude math: a single advanced fab + packaging campus runs tens of billions capex and requires multi-year ramp to meaningful utilization, so market re-rating will be driven more by visible equipment orders and offtake contracts than by PR cycles. Second-order supply-chain winners are likely to be equipment and packaging specialists, substrate/chemicals suppliers, and logistics firms able to absorb high-volume, onshore throughput; cloud software stacks and model optimizers will capture more indirect value by extracting efficiency from any new hardware. Incumbent GPU vendors retain a non-linear advantage through software stacks and ecosystem lock-in — any reduction in unit demand for their products could compress pricing, but their software-led gross margins and time-to-validated-model create a long tail that delays that effect for 2–5 years. Tail risk is execution: missing tool orders, yield issues, or a fracture with major OSATs could convert narrative gains into multi-quarter drawdowns for partners. Near-term catalysts to watch on a 0–24 month cadence are: announced long-term offtake agreements, equipment booking disclosures, first silicon yield metrics, and capital raise or government permitting milestones; reversals will be signaled by renewed supply guarantees from hyperscalers or a visible acceleration at alternative foundries.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment