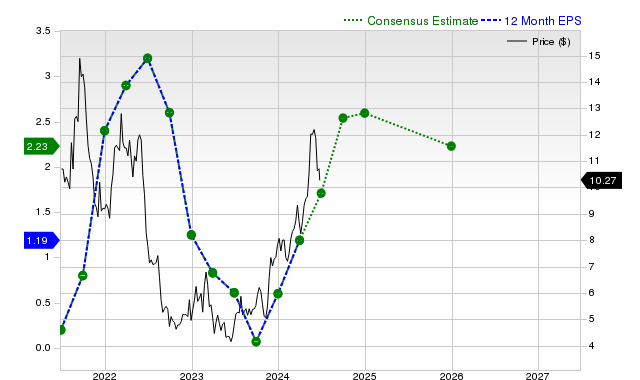

Seanergy Maritime (SHIP) has seen substantial estimate upgrades and investor interest, with shares up 21.9% over the past month. Zacks reports last quarter revenue of $46.99M (+5.9% YoY) and EPS $0.67 (vs $0.69 a year ago), beating consensus revenue of $44.02M (+6.75% surprise) and delivering a +45.65% EPS surprise; the company has topped revenue and EPS estimates in each of the trailing four quarters. Current-quarter consensus EPS is $0.47 (+38.2% YoY) and sales are forecast at $43.89M (+5.3% YoY); full-year estimates are $1.05 (‑55.9% YoY, but +112.2% revision in 30 days) and next fiscal year $1.46 (+39.1%). Zacks assigns a Rank #1 (Strong Buy) and an A Value Style Score, signaling the stock may be materially re-rated if positive estimate revision momentum continues.

Market structure: The Zacks-driven momentum for Seanergy (SHIP) suggests near-term buyer concentration in small-cap dry bulk names; direct winners are smaller owner-operators (SHIP, GNK, EGLE) and charter-rate beneficiaries while asset-light container operators and shippers with long-term contracts may lag. With consensus EPS lifting ~+75% q/q revisions, market share shifts are likely transient — pricing power comes from tight spot markets and high fleet utilization, not structural margin expansion. Risk assessment: Tail risks include a sudden collapse in Baltic Dry Index (BDI) (-40% shock), regulatory capex (ballast/IMO rules) or refinancing stress for microcaps that would erase current earnings beats. Immediate window (days–weeks) is momentum-driven and vulnerable to mean reversion; 3–12 months depends on Chinese industrial demand and orderbook deliveries (>10% fleet growth in 12 months would depress rates). Hidden dependency: recent estimate upgrades may reflect one-off vessel sales/charters or accounting timing rather than recurring op cash flow. Trade implications: Direct play — tactical long in SHIP sized 1–3% NAV with tight 12–15% stop, target +25–35% in 3–6 months if BDI stays above 1,800. Pair trade — long SHIP vs short GNK (equal notional) to isolate idiosyncratic momentum. Options — buy 3–6 month call spreads (buy ATM, sell +30–50% OTM) to cap premium on expected earnings-driven move. Rotate: overweight Transportation/Materials, underweight REITs and long-duration tech if inflation signal from freight persists. Contrarian angles: Consensus misses durability risks — earnings upgrades can be reversed if charters revert 10–20% or if deliveries accelerate; current Zacks Rank #1 may be momentum, not moat. Reaction is likely overdone in microcap liquidity: expect 10–25% intra-week whipsaws. Historical parallel: 2016–2018 dry-bulk snap rallies faded with newbuild deltas; unintended consequence — retail crowding could amplify volatility and slippage on exits.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.55

Ticker Sentiment