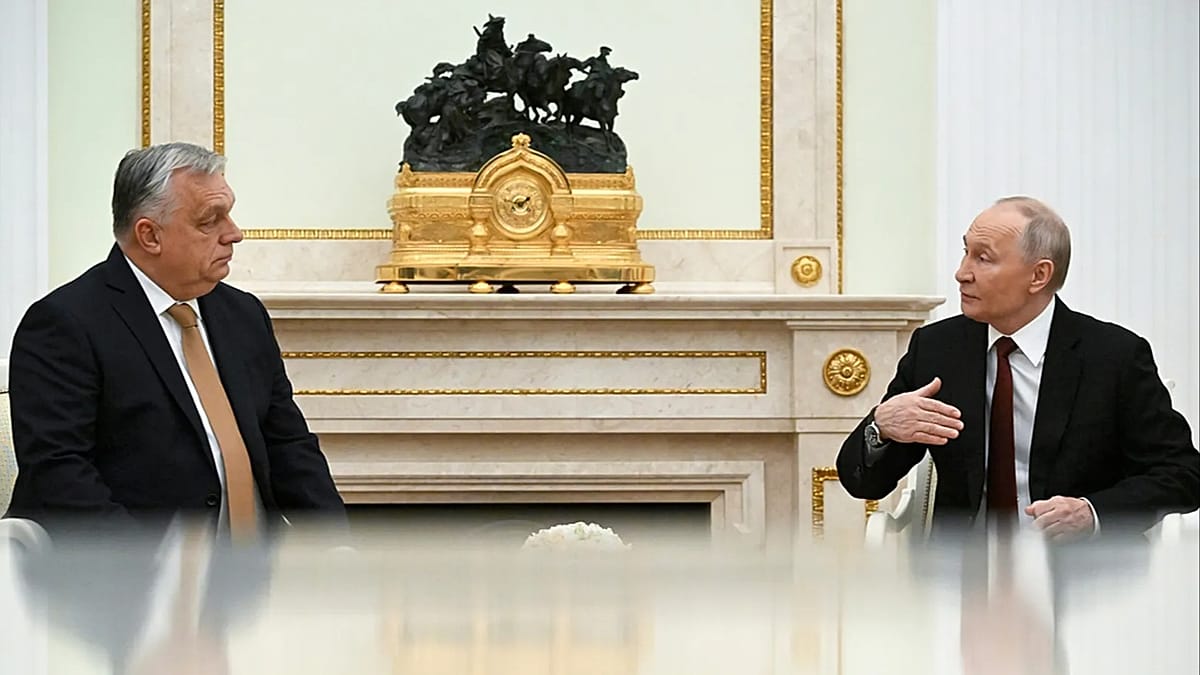

Hungarian Prime Minister Viktor Orbán met Vladimir Putin in Moscow to secure additional oil and gas supplies after receiving a US sanctions exemption that allows Hungary to continue purchasing from Lukoil and Rosneft despite US measures. Hungary is resisting EU plans to phase out Russian fossil fuels by 2027, arguing continued Russian energy is essential to avoid economic disruption, while the visit and Washington’s carve-out raise questions about the efficacy of Western sanctions and near-term energy security in Central Europe. The meetings — and potential US envoy Steve Witkoff’s visit to Moscow — could blunt sanction pressure on Russian producers and create political and energy-market frictions that hedge funds should monitor for regional supply and policy risk.

Market structure: Hungary securing continued Russian oil/gas flows materially benefits Hungarian integrated players (MOL) and physical traders who can arbitrage Urals/Brent discounts; Russian producers and sanctioned-exempt intermediaries see preserved regional demand. losers include marginal LNG suppliers to CEE and European importers who have priced capacity expansion; expect localized downward pressure on TTF and Brent spreads versus Urals by $2–$6/bbl in near term if flows persist. Risk assessment: Tail risks include US/EU re-tightening (secondary sanctions or EU legal action) that could cut Hungarian exemptions — a low-probability/high-impact shock raising Brent +15–30% in 1–3 months. Immediate (days) volatility driven by headlines; short-term (weeks–months) driven by sanction enforcement and winter demand; long-term (quarters) by EU 2027 phase-out policy and diversification capex. Hidden dependency: Hungary’s fiscal support and EU fund access can flip politics and energy flows quickly. Trade implications: Expect dispersion: central-EU refiners/refiners with Russian crude access (MOL) outperform large Western refiners and LNG shipping over 3–12 months; TTF downside risk is capped but winter tail risk persists — favor small, asymmetric option positions. Cross-asset: EUR/HUF moves will be headline-driven; sovereign spread volatility (HU sovereign) may tighten if energy costs fall but widen if EU funding is withheld. Contrarian angle: Market consensus treats Hungarian flows as marginal; this underestimates profit capture by local refiners and traders over 6–12 months and overestimates immediate EU coordination to punish buyers. Historical parallels: 2009/2014 gas disputes show political fixes can be temporary; unintended consequence — longer reliance delays capex into renewables in CEE, creating 2–4 year demand for discounted fossil fuel imports.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25