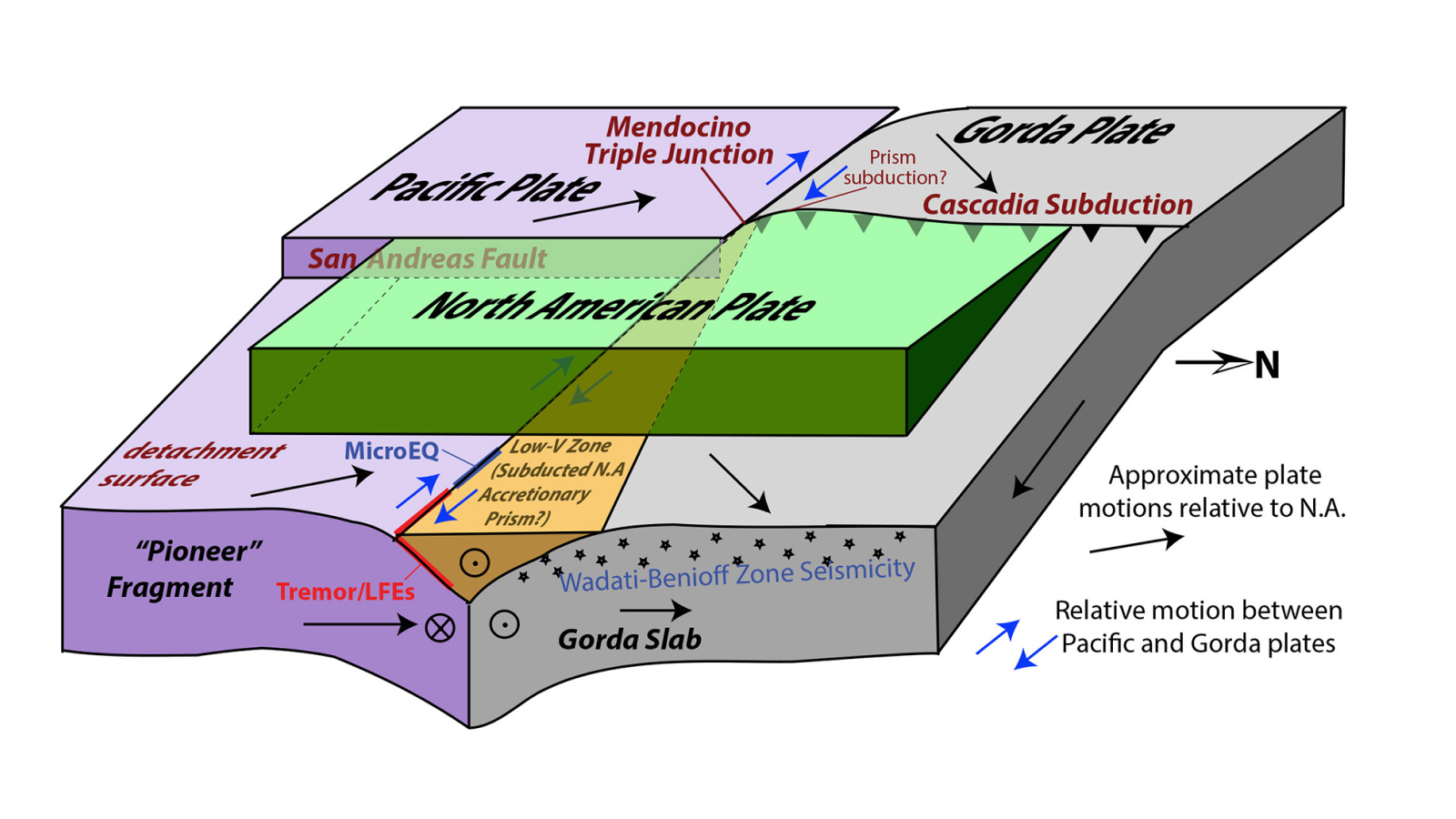

A study published Jan. 15 in Science reports discovery of the Pioneer Fragment — a remnant of the Farallon Plate stuck to the Pacific Plate near the Mendocino triple junction — sliding northwest and increasing the contact area between the Pacific Plate and the Cascadia subduction zone. The fragment creates a previously unmapped near‑horizontal fault that could alter rupture depths and earthquake dynamics, potentially prompting revisions to regional hazard models and affecting infrastructure, insurance exposure and seismic-risk assessments along Cascadia and linked San Andreas faults.

Market structure: Winners are reinsurers and specialty catastrophe-insurers (can reprice risk) and engineering/construction contractors who will capture rebuilding spend; expect reinsurance premium inflation of ~5–15% over 12–24 months if carriers re-rate Cascadia exposures. Losers are West‑Coast coastal real estate, CMBS-heavy lenders and municipal issuers in CA/OR/WA facing higher funding costs and potential downgrades; expect localized credit spread widening of 25–75bp on affected munis if hazard maps change. Risk assessment: Tail risk includes a large Cascadia event (M9+) that could create insured losses >$50–150bn and trigger systemic reinsurance losses and reinsurer capital raises; low probability (<5%/decade) but high impact. Immediate (days) market moves should be muted; short-term (weeks–months) driven by insurer filings and USGS updates; long-term (years) by infrastructure upgrades, higher insurance pricing and possible regulatory changes to building codes. Hidden dependencies: CMBS, mortgage insurers, and state budget exposure to disaster relief are second‑order transmission channels. Trade implications: Tilt modestly toward reinsurance/insurance and construction/engineering equities (2–4% tactical positions) and buy protection on CA-centric REITs and muni risk; use options to control downside (6–12 month put spreads). Cross‑asset: modest flight‑to‑safety could push 2‑year Treasury yields down 10–30bp in a shock and lift gold; commodities (cement, copper) see multi‑quarter demand lift if reconstruction occurs. Entry: initiate small positions now, scale on USGS/insurance rate announcements over 3–12 months, take profits after 12–36 months. Contrarian angles: Consensus will underprice rerating of reinsurance premiums and overprice immediate West‑Coast property doom; that creates a relative‑value opportunity to buy select reinsurers (cheap surge in ROE when rates rise) and short concentrated CA RE names that trade rich vs NAV. Historical parallels (1994 Northridge, 2011 Japan) show reinsurers recover pricing power within 12–24 months while construction/engineering firms outperform for 12–36 months. Unintended consequence: excessive regulatory tightening could reduce rebuild volumes and cap contractor upside — size positions accordingly.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25