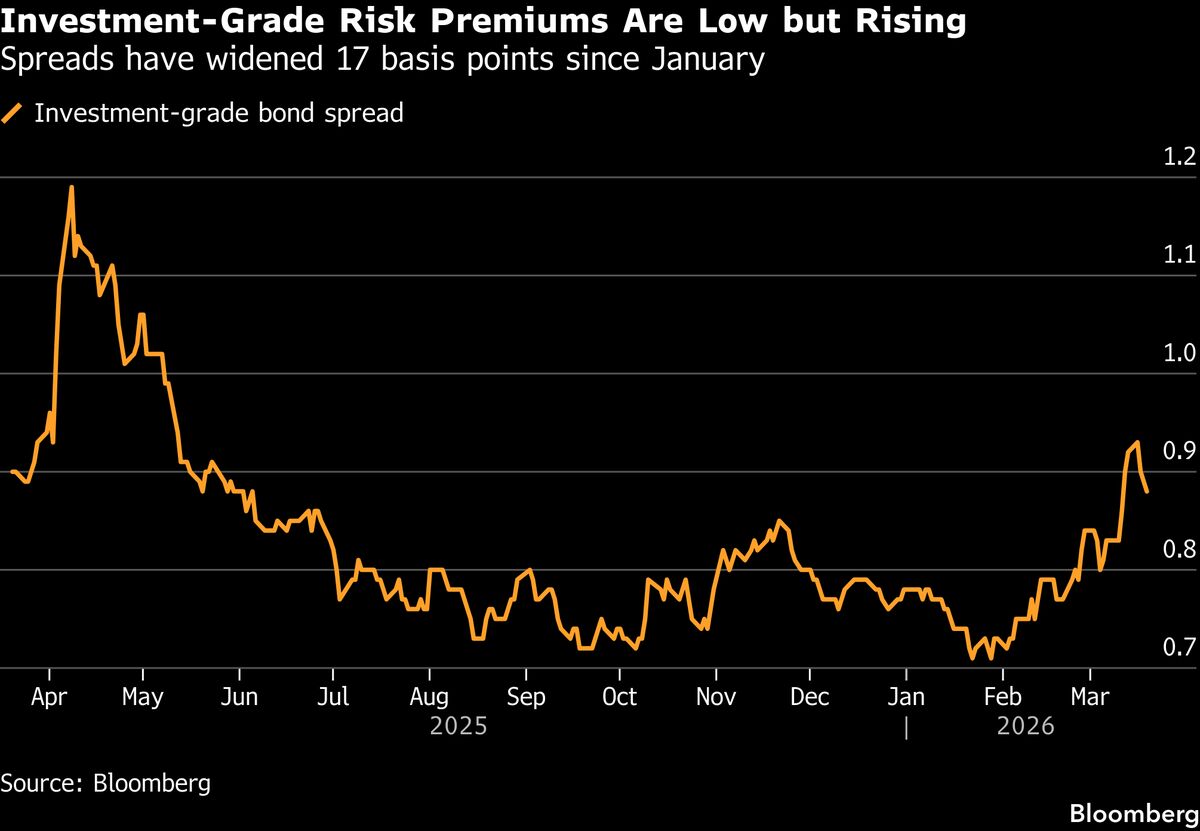

The high-grade borrowing window remains open for blue-chip issuers, but investor demand is narrowing toward more defensive, high-quality debt amid the war in Iran and rising oil prices. Jaguar Land Rover pulled a potential US bond sale citing market volatility, while tech giants continue to issue debt and a Canadian fertilizer CFO warns Iran-linked disruptions are lifting raw-material costs. Expect access to capital to persist for top-tier borrowers but with tighter investor preferences that favor higher-quality credits and defensive issuance structures.

Primary-market openness for top-tier borrowers has created a micro-market where liquidity preferences — not credit fundamentals — are driving prices. Marginal demand is concentrated in short-to-intermediate tenors and liquid, indexable lines, which compresses spreads for 3–7 year tranches while leaving tail-duration and off-benchmark issuers weakly priced; that dichotomy amplifies roll and curve trades where carry can be captured with limited credit beta.

The narrowing of investor focus to liquid high-grade instruments cascades into the leveraged-finance plumbing: banks and CLOs prefer seasoning and covenant quality, reducing refinancing options for mid-cap and covenant-light issuers. Expect a rise in idiosyncratic defaults among names that rely on continuous primary access rather than cashflow resilience — stress will show up first in loan Covenant-Lite origination, then in single-B cash bonds.

Catalysts that flip the setup are compact and front-loaded: sudden liquidity shocks (days–weeks) will blow out HY and long-IG spreads 150–300bps and 40–80bps respectively, while slower macro squeezes (3–12 months) driven by input-cost inflation or central-bank policy normalization will progressively reprice credit curves. The asymmetric payoff favors transient carry capture in liquid IG and disciplined tail protection for credit beta exposure.

Contrarian stance: the market’s defensive positioning may be overstated — continued primary supply from high-quality issuers effectively mops up liquidity and can keep IG spreads tight even amid headline volatility. Tactical buyers who accept limited spread risk for outsized carry in 3–7 year IG paper should outperform broad risk-on assets if defaults remain benign over the next 6–12 months.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.20