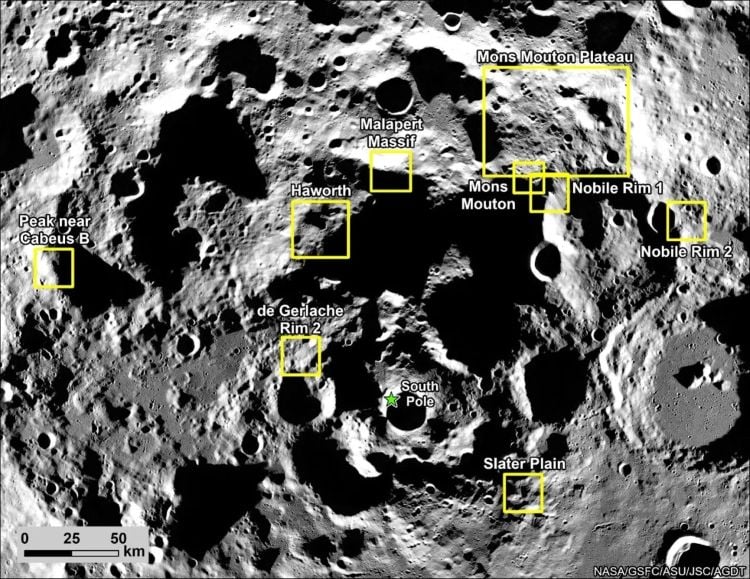

Nine candidate lunar south-pole landing regions have been downselected (from an earlier 13) with an estimated surface mission duration of 5.75–6.25 days; Artemis II is due to launch in under 48 hours as a 10-day lunar flyby. NASA has re-designated Artemis III as a 2027 orbital docking test for commercial landers, pushing a crewed lunar surface landing to Artemis IV (currently planned for 2028). Communications relay and terrain safety (intermittent line-of-sight behind crater rims) are highlighted as critical risks after the IM-2 anomaly, implying potential procurement and capex opportunities for relay/lander systems but only limited near-term market impact for public equities.

The immediate commercial levers are not the landers themselves but the enabling stack: persistent relay communications, cryogenic handling at extreme cold, and precision surface robotics. Contracts and CAPEX will flow fastest to firms that can demonstrate flight-proven relay hardware, radiation-hardened avionics, and thermal-management subsystems—these are high-margin, low-volume items that prime contractors subcontract to specialists. A subtle supply-chain price pressure will emerge in two places: (1) radiation-hardened microelectronics and space-qualified cryogenic valves — lead times measured in quarters not days — meaning selected suppliers can re-price and prioritize allocation, and (2) launch cadence for high-altitude relay satellites, which will push demand into the already tight smallsat chassis and propulsion supplier market, amplifying cost passthrough to builders within 6–24 months. Key near-term catalysts are government awards and demonstration successes; expect visible revenue recognition only after hardware-in-the-loop tests and flight demos (12–36 months). Tail risks: a high-profile test failure or budget reprioritization can wipe anticipated multi-year revenue streams, and technical pivot to optical inter-satellite links would favor different suppliers than RF-centric ones, reversing winners within a single procurement cycle. For portfolio positioning, prioritize optionality into suppliers of relay communications and space robotics, size positions modestly (single-digit percent of thematic sleeve), and hedge program execution risk with cheap out-of-the-money protection or pair trades that short broad aerospace exposure while long niche contractors.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.05

Ticker Sentiment