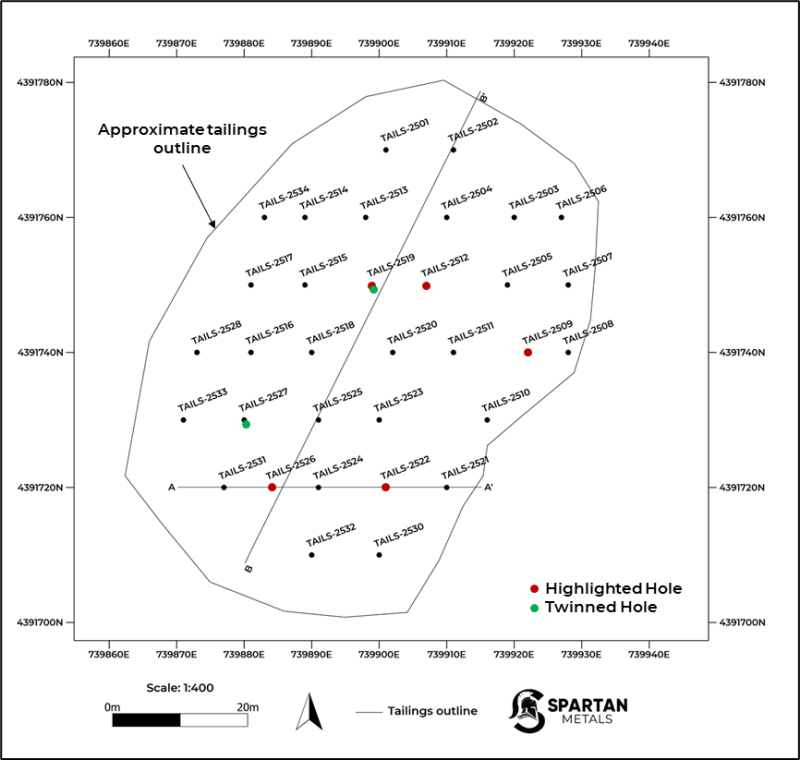

Spartan Metals reported assay results from 34 shallow drill holes into the Tungstonia tailings at its 100%-owned Eagle project in Nevada, returning a weighted average of 0.13% WO3, 10.6 g/t Ag and 626 ppm Rb across 133 samples with several higher-grade intervals (e.g., up to 0.42% WO3 and 123 g/t Ag). The company notes the 0.13% WO3 average is near reported operating cutoffs (Sangdong 0.15% WO3) and that applying a 0.15% cutoff yields a 0.20% WO3 average for 41 samples; Spartan is advancing metallurgical testing, 3D modelling and an initial resource/economic evaluation targeting completion in early 2026.

Market structure: Positive tailings assays (weighted 0.13% WO3, 10.6 g/t Ag, 626 ppm Rb; subset 0.20% WO3 if using 0.15% cutoff) makes Spartan (TSXV:W / OTCQB:SPRMF) and other US tungsten/rubidium juniors immediate potential winners because tailings lower capex and compress time-to-cash (months→1–2 years). Material market-share or global price impact is unlikely near-term — tungsten market is small but concentrated, so sustained domestic ramp-up over multiple years could shave premiums on Chinese material and raise bargaining power for US defense purchasers. Cross-asset: expect idiosyncratic equity moves in juniors, modest positive sentiment for defense suppliers (6–12 month), and negligible immediate FX or sovereign bond impact; industrial commodity and small-cap mining volatility will increase. Risk assessment: The single largest binary is metallurgy: gravity/leach recovery <40–50% for W/Rb or Rb locked in refractory phases would render economics negative; expect metallurgical results within 60–90 days and a maiden resource in early 2026. Permitting/BLM tailings reprocessing and environmental liabilities create 6–18 month regulatory tail risk; financing risk is high (microcap dilution likelihood >30% if capital required). Tail risks include discovery of mixed-host refractory tungsten, unfavourable reagent costs, or a sustained collapse in W pricing (>25%) that removes project optionality. Trade implications: For tactical exposure, establish a small speculative long in SPRMF (1–2% portfolio) ahead of metallurgy, scale to 3–4% only after metallurgy shows >=50% W recovery and twin-hole confirmatory mineralogy; set a hard exit if recoveries <40% or if company issues dilutive financing >C$1.5M. Consider a relative-value pair: long SPRMF 1% / short Almonty (TSX:AII) 0.5% to isolate idiosyncratic upside, re-weight at metallurgy/resource milestones (60–120 days and early‑2026). For volatility traders, buy 9–12 month call spreads on AII (e.g., 20%/35% OTM) as a tungsten-price proxy; rotate 1–3% from general small-cap mining into defense contractors (LMT, RTX) over 6–12 months. Contrarian angles: Consensus under-weights the speed and economics of tailings reprocessing — a successful metallurgy + low strip/processing cost could create near-term free-cash-flow optionality and a rapid re-rate; conversely the market may be over-optimistic about tonnage — historic mine output implies limited tailings inventory and M&I resource could be <100–250kt, capping upside. Historical parallels: many tailings plays fail on metallurgy (rarely become producers), so asymmetric reward favors small, staged bets with milestone-based scaling. An unintended consequence: positive metallurgy could trigger M&A from mid-tier miners within 6–12 months, compressing takeover arbitrage spreads.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.32