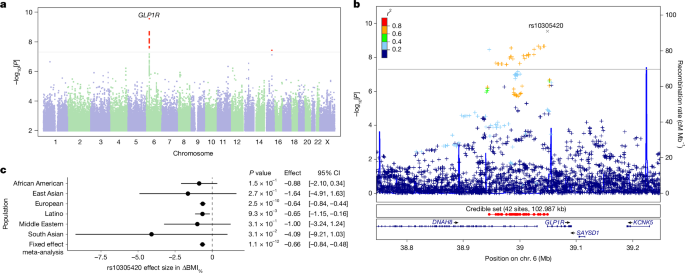

A GWAS of 27,885 23andMe participants identified a GLP1R missense variant (rs10305420, P = 2.9×10⁻¹⁰) associated with greater weight loss (~−0.641% BMI per T allele, ~−0.76 kg per allele) and GLP1R and GIPR variants linked to nausea/vomiting (GIPR rs1800437 associated with vomiting on tirzepatide, P = 4.2×10⁻⁹, OR ≈1.84). Findings were replicated in All of Us (rs10305420 P = 0.001) and incorporated into predictive models that explained ~25% of variance in BMI loss (AUC ~65–68% for nausea/vomiting models), though most predictive power came from non-genetic factors. Implication: biologically plausible pharmacogenetic markers could enable stratified prescribing for GLP‑1/GIP therapies, but effect sizes are modest and near‑term market impact is limited.

This paper creates a credible regulatory and commercial wedge: drug-target genetics converts a broad obesity market into stratified sub-markets where efficacy and tolerability can be predicted up-front. That creates immediate optionality for companies that can supply low-cost, rapid genotyping and for biopharma teams that incorporate companion diagnostics into label and payer conversations — sequencing capex and integration with EHR/telehealth become revenue drivers rather than peripheral R&D spend. For GLP1/GIP developers the practical second-order effect is segmentation of lifetime patient value. A reliable genetic stratifier reduces churn (fewer discontinuations) for patients predicted to tolerate and respond, but raises acquisition costs because prescribers and payers may demand testing before reimbursing high-cost chronic therapy. That bifurcates winners: vertically integrated players who control drug, testing and telehealth pathways (or have exclusive diagnostics partnerships) will capture margin expansion; pure-play drugmakers without diagnostics partnerships face higher commercial R&D and potential utilization headwinds. On the technology side, platforms that aggregate real-world efficacy and link genotype-to-outcome (HealthKit-style data pipes) gain strategic leverage: they become gatekeepers for post-market evidence needed for coverage decisions. Privacy and regulatory pushback are non-trivial tail risks that can materialize within 6–24 months, but if resolved favorably, they cement durable data moats and recurring revenue for device/cloud incumbents.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.35

Ticker Sentiment