Boeing is demonstrating significant operational improvements under CEO Kelly Ortberg, including a turnaround in its Defense, Space & Security segment profitability and an FAA-approved increase in 737 MAX production rates from 38 to 42 per month, which is expected to accelerate deliveries against its substantial $619 billion backlog. These developments suggest positive near-to-medium term momentum for the stock. However, a key long-term challenge remains the company's ability to fund a $50 billion next-generation narrowbody development, given its current $30.3 billion net debt, and to strategically choose engine technology amidst competitor advancements, which could impact its future competitive position.

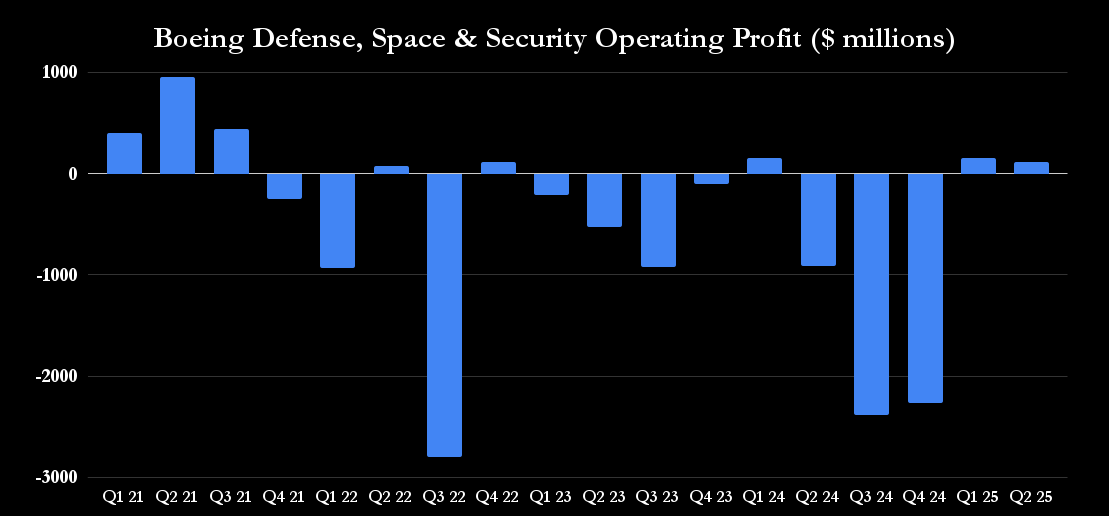

Boeing (BA) is demonstrating significant operational improvements under CEO Kelly Ortberg, who took the helm in August last year. The company's substantial $619 billion backlog at the end of Q2 underscores its long-term potential, with recent tangible improvements bolstering the investment case. This positive momentum is further supported by the FAA's approval to increase 737 MAX production rates from 38 to 42 aircraft per month, which is expected to accelerate deliveries against over 4,800 unfilled orders. A key driver of this turnaround is the Defense, Space & Security (BDS) segment, which has returned to profitability in recent quarters after years of underperformance. This improvement is attributed to management's focus on resolving issues with fixed-price development programs, which constitute 15% of the BDS portfolio, and the strategic replacement of the former BDS CEO with veteran Steve Parker. The new leadership is actively improving cost estimations, suggesting sustainability for these margin enhancements. Despite near-to-medium term tailwinds, Boeing faces significant long-term strategic challenges. Funding a projected $50 billion investment for a next-generation narrowbody aircraft over a decade is a concern, given the company's $30.3 billion net debt as of Q2. Additionally, a critical decision looms regarding engine technology, as competitor Airbus is actively pursuing open fan technology (RISE program with CFM International), while Boeing is believed to favor traditional ducted engines, potentially risking a competitive disadvantage if the open fan technology proves superior.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly positive

Sentiment Score

0.70

Ticker Sentiment