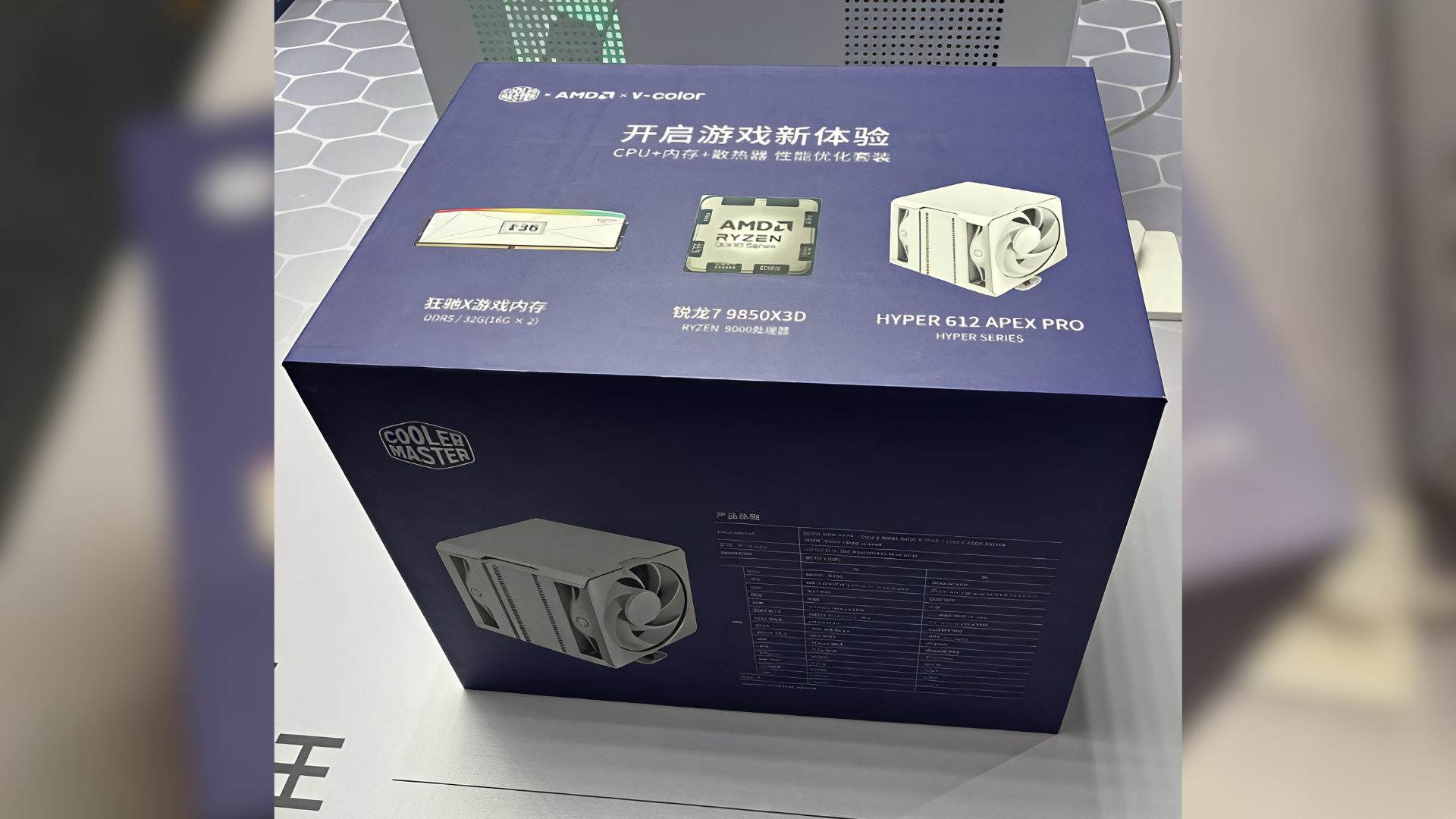

AMD is launching the Ryzen 7 9850X3D and has been spotted offering an official boxed bundle in China that pairs the $500 CPU with a Cooler Master Hyper 612 Apex cooler (~$79.99) and a 32 GB V-Color Manta XFinity DDR5-6000 kit (retailing ~ $500), which together total roughly $1,080 at standalone retail prices. The China-specific collaboration appears aimed at easing local memory shortages and providing an all-in-one purchase option; AMD has also stated the 9850X3D does not require high-speed DDR5, implying lower-cost DDR5 kits may be sufficient for gaming performance.

Market structure: Official AMD+Cooler Master+V-Color bundles in China point to two simultaneous forces — constrained DDR5 supply for premium kits (V-Color retailing ~$500 vs $200 launch) and AMD using packaging to manage channel optics and demand. Winners: DRAM manufacturers (Micron MU, Samsung, SK Hynix) on tight pricing and system integrators able to upsell; losers: niche high-end DRAM retailers and any OEMs forced to discount CPUs to move slow-selling memory. Cross-asset: sustained high DRAM prices support semiconductor equities and capital goods for fabs, while dampening discretionary PC spend and potentially pressuring consumer cyclicals in China over next 1-3 quarters. Risk assessment: Tail risks include China export restrictions or a sudden DRAM capacity ramp (TSMC/DRAM fab capex) that collapses prices >20% in 6-12 months, and AMD margin compression if it subsidizes bundles broadly. Immediate (days) risk is limited to sentiment noise; short-term (weeks/months) sees DRAM price volatility and inventory swings; long-term (quarters) hinges on fab capacity additions and AMD product adoption. Hidden dependency: AMD’s CPU unit economics depend on TSMC yields and third-party memory OEM inventory positions that can flip from shortage to glut quickly. Trade implications: Favor selective long exposure to memory makers (MU) for a 3–6 month DRAM tightness play while hedging AMD execution risk via option spreads. Tactical shorts: small caps tied to premium DDR5 SKUs (e.g., CRSR) where demand may reprice if mainstream CPUs de-emphasize high-speed DRAM. Time entries around DRAM contract-price prints (TrendForce/DRAMeXchange) over the next 30 days and AMD quarterly commentary within 45 days. Contrarian angles: Consensus treats high DRAM prices as uniformly bullish for all memory suppliers; miss is that AMD’s messaging that 9850X3D doesn’t need >4800 MT/s could structurally reduce TAM for premium DDR5 kits by >30% among gamers over 12 months. That suggests short-duration dispersion: long broad DRAM exposure, short niche premium kit vendors/retailers. Historical parallel: 2018 DRAM cycle where a short-lived capacity capex reversal led to a 40% price drop in 8 months — watch fab capex announcements as the key reversal signal.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.12

Ticker Sentiment