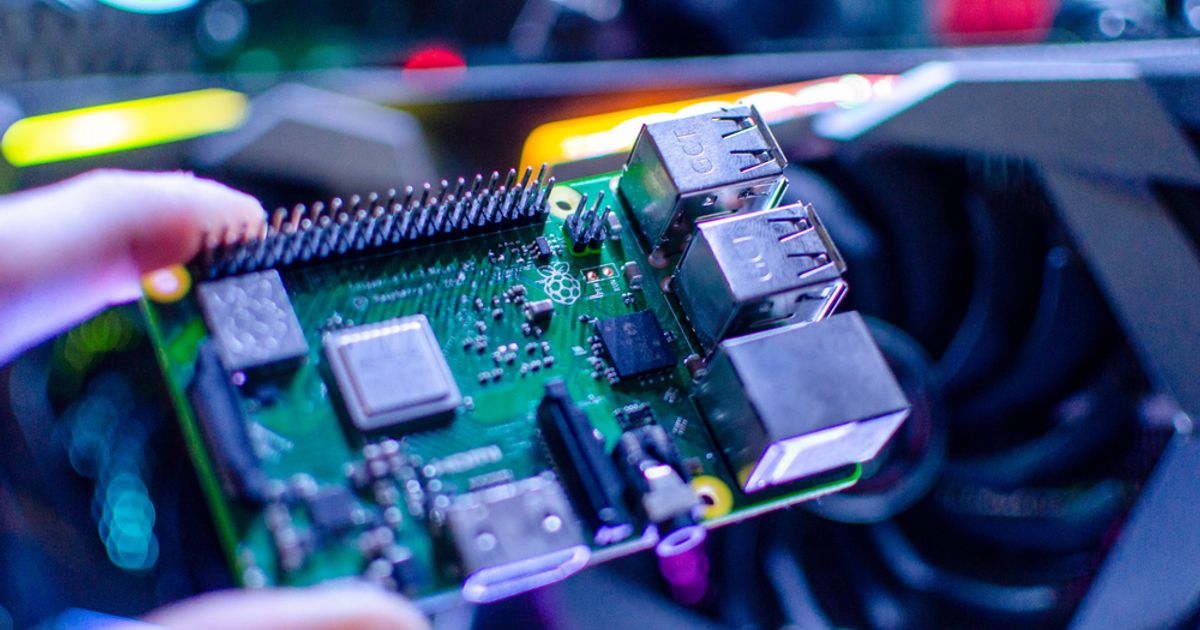

Raspberry Pi Holdings PLC (LSE:RPI) shares spiked 8% in one day and are up 59% over the past month after OpenClaw, an AI agent, inspired a 24‑hour clone called PicoClaw that reduces memory footprint by 99% (from ~1 GB to <10 MB), boots in one second (vs ~500+ seconds) and runs on low‑cost Raspberry Pi hardware (£13.50 for Zero W, £108 for Series‑5). PicoClaw — reportedly 95% AI‑generated and released under the MIT license — has gone viral, driving retail and developer interest and materially lifting investor sentiment toward Raspberry Pi; the development broadens the addressable use cases for ultra‑low‑cost edge devices but also raises questions about monetization and competitive dynamics.

Market structure: Winners are low-cost single-board computer vendors (Raspberry Pi Holdings PLC, LSE:RPI) and suppliers of low-power MCUs/SoCs (STM, NXPI, QCOM) as PicoClaw lowers the cost to deploy AI agents from ~$1k+/server to sub-£15 devices. Losers are marginal cloud inference volumes and high-margin managed agent services at hyperscalers (AMZN, GOOGL, MSFT) if edge substitution accelerates; pricing power shifts toward commodity silicon and embedded firmware. Supply/demand: near-term demand shock for Pi-class boards could lift device ASPs +10-30% if viral adoption scales in 1–3 months, while server rental demand may soften incrementally (single-digit % headwind). Cross-asset: credit spreads on small HW suppliers may tighten; equity volatility in cloud names could rise; modest FX flows into GBP on RPI headline moves; commodities impact (copper/silicon wafers) minimal short-term. Risk assessment: Tail risks include IP litigation (OpenClaw originators), export controls or platform takedowns, and security exploits from a widely-deployed MIT-licensed agent — any could force rollbacks within 30–90 days and crash related equities. Timing: immediate (days) = momentum/risk-on for RPI; short-term (weeks–months) = adoption and supply resets; long-term (years) = architectural shift to heterogeneous edge+cloud that reallocates ~5–15% of cloud inference revenue to edge. Hidden dependencies: reliance on microSD, boot firmware, and upstream SoC vendors; a supply bottleneck or firmware vulnerability is a single-point failure. Catalysts: GitHub forks, Raspberry Pi inventory reports, and hyperscaler counter-products or partnerships will accelerate/ reverse trends within 1–3 months. Trade implications: Direct plays — establish tactical longs in RPI (LSE:RPI) sized 2–3% of tech allocation to capture viral momentum, target +25–35% in 1–3 months, stop -12%. Buy selective exposure to edge-capable silicon: allocate 1–2% each to STM (STM) and NXPI (NXPI), target +20–30% over 12 months, stop -18%. Hedge cloud exposure with small protective option trades: buy 3–6 month put spreads on AMZN and MSFT (size 0.5–1% notional each) to limit downside if revenue mix shifts. Sector rotation: trim 2–4% from pure cloud service names (AMZN, GOOGL) and redeploy into hardware/embedded software names and cybersecurity plays. Contrarian angles: The market may be over-indexing on substitution; edge agents are complementary (latency/privacy) not full replacements — hyperscalers can repackage edge-to-cloud hybrid offerings, muting long-term cloud revenue losses. RPI’s rally risks being sentiment-driven: Raspberry Pi’s gross margins are low, so stock gains may mean-revert if hardware unit economics don’t improve; expect >25% intramonth drawdown risk. Historical parallel: past open-source microcontroller waves boosted device volumes but did not materially displace centralized compute (2012–2018); unintended consequences include security incidents that could trigger regulation and reduce adoption quickly.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.45