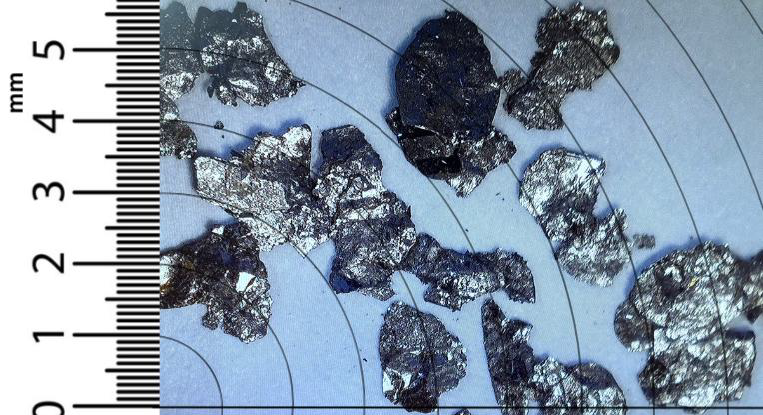

First Canadian Graphite expanded airborne EM and magnetic surveys over newly acquired Berkwood claims and announced preliminary dry-separation metallurgical results from Zone 3 showing graphitic carbon (Cg) ranging 6.43%–39.66%, average total carbon (Ct) 32.47% and average Cg 22.90% across eight grab samples, with >85% of separated flakes coarser than 80 mesh. The company cites an existing in‑pit resource of 1,755,300 tonnes indicated at 17.00% Cgr and 1,526,400 tonnes inferred at 16.39% Cgr, and Volt Carbon reports prior dry‑air classification purities of ~95%–98.5%; however the Zone 3 tests are preliminary, conducted in a non‑ISO lab by a related party, and First Canadian plans further metallurgical optimization and drilling in Spring/Summer 2026.

Market structure: The Volt Carbon dry-separation results (avg Ct 32.5%, avg Cg 22.9%; Cg range 6.4–39.7%; >85% >80 mesh) materially de-risks Berkwood’s product quality vs typical flotation-only juniors. If verified at scale (threshold: >95% purity and >40% mass recovery into +80 mesh), Berkwood can command 10–25% premium on large-flake pricing, benefitting First Canadian Graphite (GBMIF/FCI) and dry-processing technology providers; incumbent flotation-focused juniors and toll processors face margin pressure. Macro supply impact is limited near-term—project tonnage ~3.28 Mt (indicated+inferred) is small vs global graphite market—but successful dry-processing adoption is a structural negative for water-intensive processors over 12–36 months. Risk assessment: Key tail risks are (1) scale-up failure of dry air classification (50–70% chance of lower recoveries in bulk), (2) Indigenous/permitting delays (10–25% chance of >12-month delay), and (3) financing dilution (probable within 6–12 months for exploration). Short-term (0–3 months) catalysts are airborne EM results and partner interest; medium term (3–12 months) is drill metallurgy and independent verification; long term (>12 months) are permits, financing and offtake. Hidden dependency: lab not ISO-certified and Volt is related party—independent ProGraphite verification is the decisive credibility gate. Trade implications: Tactical long-biased exposure to GBMIF (TSXV:FCI / OTC:GBMIF) is warranted but small—speculative allocation 1–3% of risk capital with explicit triggers: upsize to 3–6% if third-party labs confirm >95% purity and +40% recovery to +80 mesh within 6 months, or if airborne EM yields new drill targets >200m strike. Hedge via a 1:1 pair short in TORVF-sized peer (or broader graphite junior basket) to neutralize macro graphite beta; if liquid options exist, use 4–6 month call spreads to limit premium outlay around drill-release windows. Contrarian angles: Consensus may overvalue grab-sample metallurgy; market underprices execution and scale risk—if bulk samples show <25% recovery to +80 mesh, share price could fall 40–60% quickly. Conversely, successful independent verification plus a small partner JV could re-rate GBMIF by 2x within 6–12 months given large-flake premiums and low environmental footprint. Watch for unintended consequence: rapid investor enthusiasm prompting dilutive financings—use financing size (>C$5–10M) as a sell/trim trigger within 60 days.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.30

Ticker Sentiment