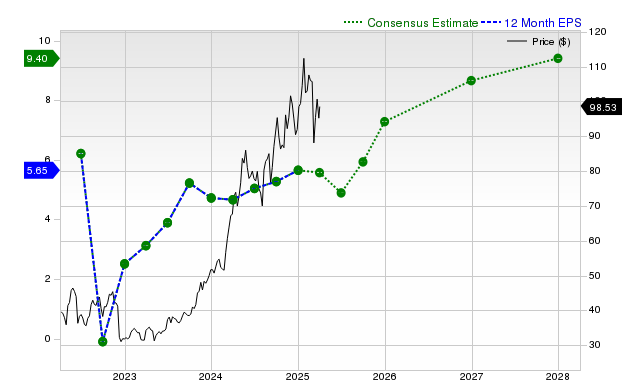

NRG Energy (NRG) has significantly outperformed its industry and the S&P 500 recently, posting a +10.7% return over the past month. While current quarter EPS estimates saw an 18.7% downward revision to $1.83, full-year estimates for the current and next fiscal years project strong growth at $7.93 (+19.4% YoY) and $9.25 (+16.6% YoY), respectively. The company has a consistent track record of beating revenue and EPS estimates, and its Zacks Value Style Score of 'B' suggests it trades at a discount to peers. Despite these positive indicators, its Zacks Rank #3 (Hold) implies a near-term performance in line with the broader market.

NRG Energy (NRG) exhibits a compelling but mixed financial profile, characterized by strong recent market outperformance against a backdrop of revised near-term earnings expectations. The stock has returned +10.7% over the past month, significantly outpacing the S&P 500's +2.6% gain and its peer group in the Zacks Utility - Electric Power industry, which contracted by 1.8%. This momentum, however, is contrasted by a sharp -18.7% downward revision in the consensus EPS estimate for the current quarter to $1.83, signaling potential near-term headwinds. Looking further out, the outlook appears robust, with full-year consensus EPS estimates projecting strong growth of +19.4% for the current year and +16.6% for the next. This long-term growth is underpinned by an aggressive revenue forecast, particularly for the next fiscal year, which anticipates a +31.3% increase. The company's operational execution is solid, having surpassed consensus revenue estimates for four consecutive quarters and EPS estimates in three of the last four. Furthermore, with a Zacks Value Style Score of 'B', the stock appears to be trading at a discount relative to its peers, suggesting that its recent price appreciation has not led to an overstretched valuation.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mixed

Sentiment Score

0.15

Ticker Sentiment