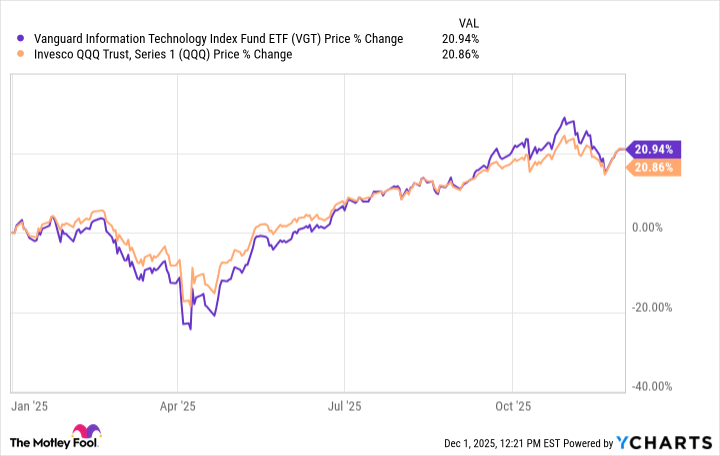

Vanguard Information Technology ETF (VGT) has risen nearly 21% year-to-date through November but is highly concentrated: Nvidia (18.18%, $4.366T), Apple (14.29%, $4.144T) and Microsoft (12.93%, $3.630T) together account for over 45% of the 314-stock fund. The article warns that this megacap concentration creates downside risk amid early-December market uncertainty and recommends less concentrated tech exposures such as QQQ, where the top three names constitute roughly a quarter of the ETF despite similar year-to-date performance.

Market structure: VGT’s cap-weighting has concentrated ~45% of the ETF in NVDA/AAPL/MSFT, turning a 314-stock vehicle into a quasi-mega-cap bet; a 10–20% correction in those three names would likely drag VGT down 4.5–9% instantly, far above a diversified tech basket. Passive flows amplify that: index rebalances and year-end window-dressing increase flow sensitivity to price moves in megacaps over the next 2–6 weeks. Semicap and software suppliers (LRCX, KLAC, INTU) are direct beneficiaries of sustained AI capex, while mid/small-cap software & hardware names suffer relative crowding-out. Risk assessment: Key tail risks are (1) renewed US–China export controls on high-end GPUs/ASML shipments, (2) an earnings-guidance reset from NVDA or MSFT, and (3) rapid Fed-driven multiple compression; any can produce >20% drawdowns for concentrated tech within months. Short-term (days–weeks) risks are positioning and volatility spikes around December rebalancing and earnings; long-term (quarters) risks hinge on secular AI capex sustaining revenue growth vs. margin reversion. Hidden dependency: VGT’s realized beta is effectively NVDA-beta + Apple/MSFT-beta; passive crowding can create feedback loops where outflows beget price declines. Trade implications: Reduce concentration risk and harvest dispersion — prefer QQQ (top-3 ~25%) or equal-weight tech exposure to cut single-stock sensitivity; selectively long semiconductor-equipment names (LRCX, KLAC) to capture supply-side tightness from AI infrastructure with 6–12 month horizons. Use options to hedge concentrated exposure: buy 1–3 month put spreads on NVDA or VGT ahead of key quarterlies and rebalance after IV compression. Reweight toward cyclicals or industrials if Fed signals sustained tightening to limit tech drawdown exposure. Contrarian angles: Consensus fear of concentration may be overdone if AI earnings continue to justify multiples — NVDA-style winners can continue to lead returns, meaning VGT could outperform if megacaps extend momentum. Historical parallel: 1999 concentration turned into dispersion after a shock, but unlike 1999 current leaders have strong free cash flow and buybacks, reducing bankruptcy tail. Unintended consequence: mass migration from VGT to QQQ or equal-weight ETFs increases liquidity in mid-cap tech and could produce short-term outperformance in underowned names; this creates pair-trade opportunities to long equal-weight tech vs. short cap-weighted VGT.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35

Ticker Sentiment