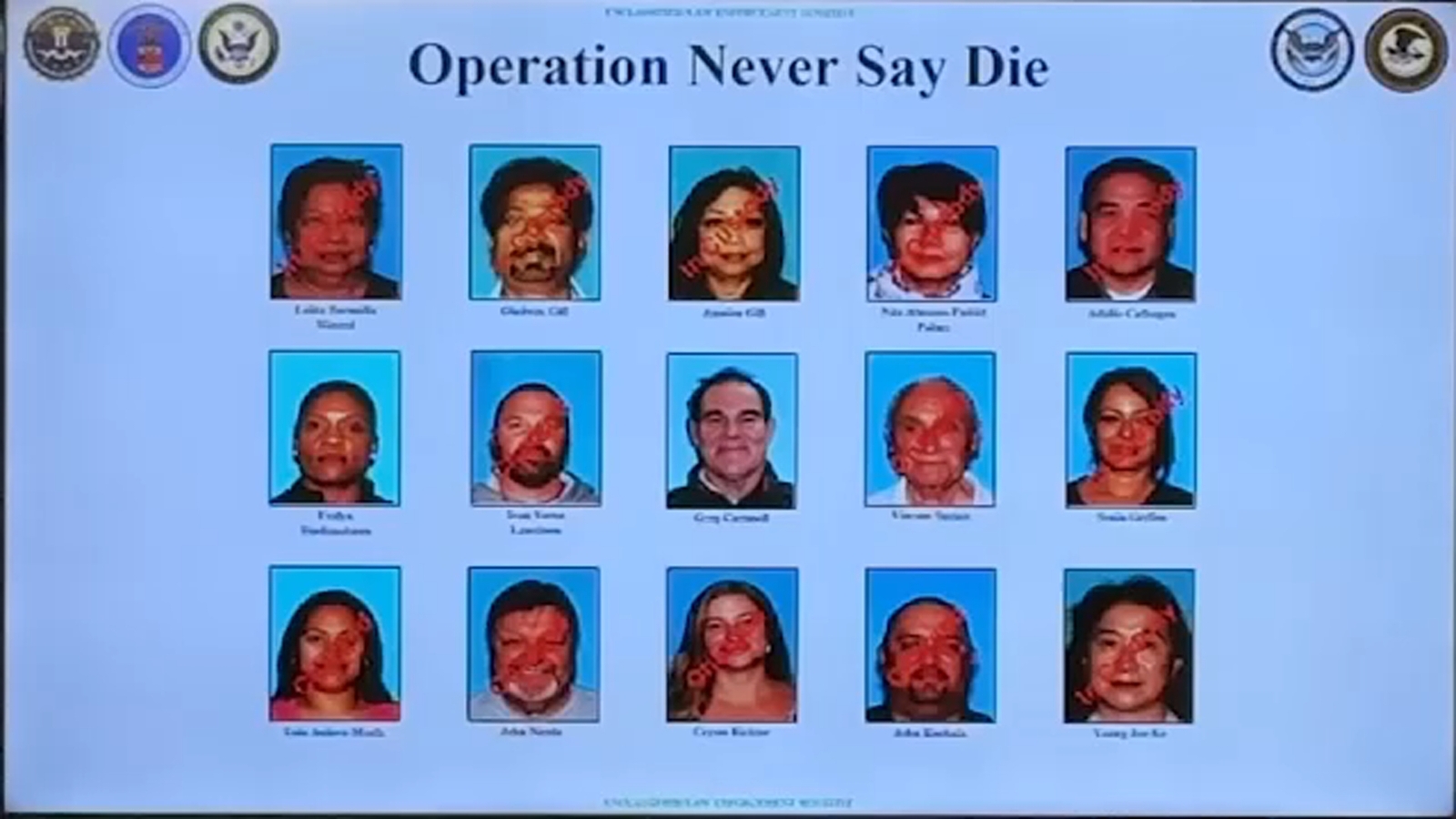

Federal authorities executed a major Southern California health-care fraud takedown: eight arrests and more than a dozen charges in an alleged Medicare/hospice scheme that federal officials say resulted in roughly $60 million in losses. DOJ alleges defendants recruited non‑terminal beneficiaries and submitted false hospice claims; CMS head Dr. Mehmet Oz announced a planned review of every hospice in California this year. Officials publicly faulted state and county leadership and noted hospice fraud accelerated during the COVID‑19 pandemic.

The immediate market impact will be concentrated in small- and mid-cap post‑acute operators where Medicare/Medicaid reimbursement is a majority of revenue; expect faster multiple compression there than in diversified health services names because investors will re‑price regulatory and recoupment tail risk into near‑term EBITDA. In the first 1–8 weeks this typically shows up as 10–25% underperformance vs large-cap managed care and hospital names as auditors and payors flag historical claims and force reserve builds. Over the next 3–12 months, payors and CMS contractors will tighten intake and prior‑authorization workflows, which lowers utilization growth and increases administrative expense for operators; healthy players with audit-ready revenue cycles will capture share while marginal providers face cash‑flow stress. That creates a two‑track market: short duration downside for exposed operators and a longer consolidation opportunity for strategic acquirers and for managed‑care plans that reduce improper payments and improve MLRs. Catalysts that matter: (a) state or federal policy bulletins that expand claim‑review windows (days–months), (b) large recoupment rulings or operator restatements (weeks–quarters), and (c) deals where stronger operators acquire smaller distressed providers (3–12 months). The consensus risk is not merely headline legal exposure but the operational shock from suspended referrals and tighter MA contracting — if that’s transitory, small caps will snap back; if structural, expect multi‑quarter underperformance and M&A activity to accelerate.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly negative

Sentiment Score

-0.65