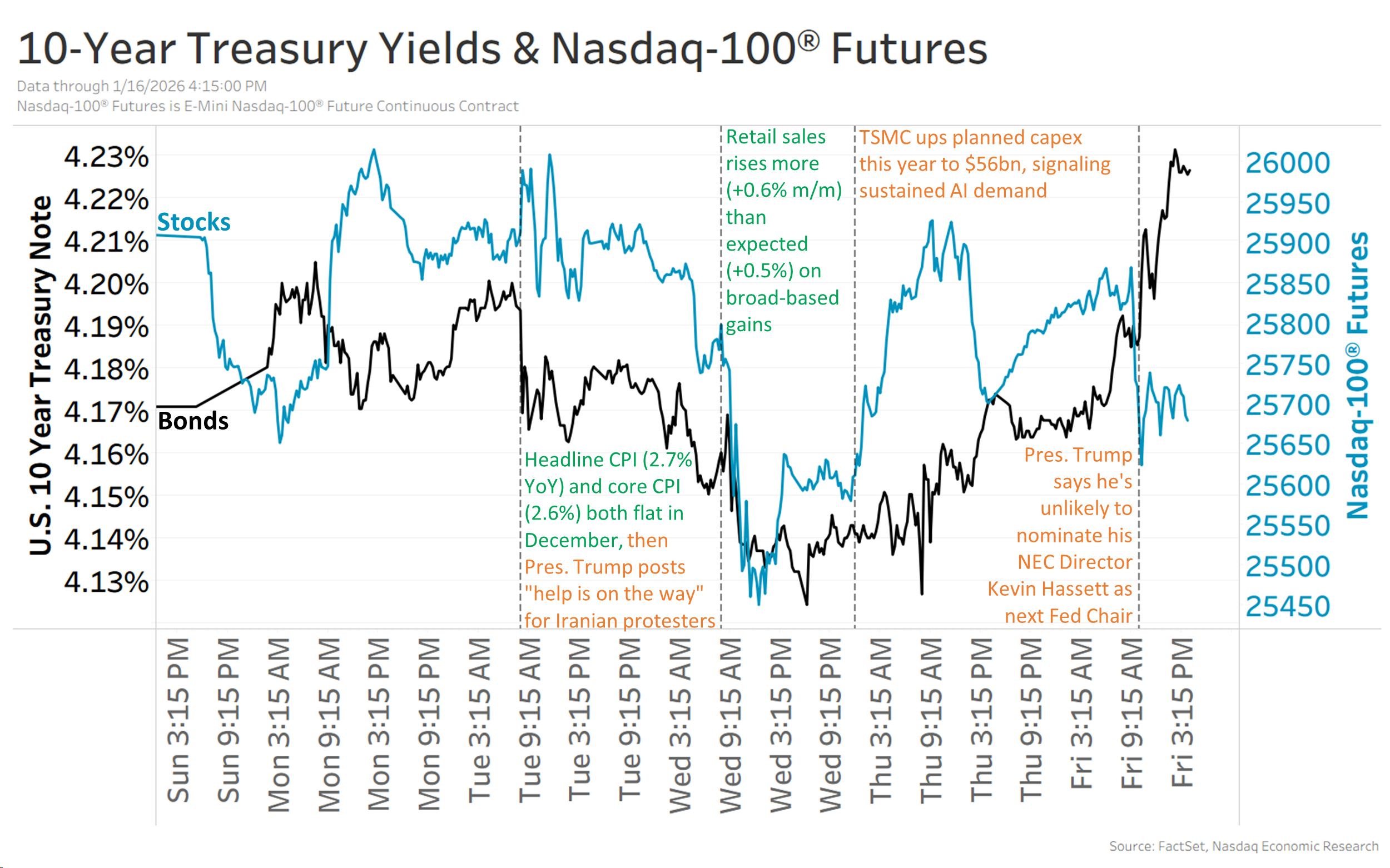

Headline CPI held steady at 2.7% YoY and core CPI at 2.6% YoY in December, while retail sales rose 0.6% m/m in November and manufacturing output unexpectedly grew 0.2% m/m in December versus a -0.1% print forecast. Those data points, combined with geopolitical noise, pushed market-implied Fed cuts down to ~45 bps for the year, sending the Nasdaq-100 roughly 1% lower and 10-year yields up ~5 bps above 4.2%. Separately, TSMC announced plans to boost capex by as much as 37% this year and materially expand capacity in 2028-29 on AI demand, underscoring technology-sector capex upside even as monetary policy expectations tighten.

Market structure: TSMC's announced up-to-37% capex increase and explicit 2028–29 capacity scaling crystallizes a two-phase cycle: tight near-term supply for advanced AI nodes (through 2026–27) supporting pricing power and equipment demand, followed by potential easing in 2028–29 that could compress foundry margins by an estimated mid-single-digit percentage. Macro data (CPI core 2.6% YoY, retail +0.6% m/m, 10y ~4.2%) and lower-than-expected Fed cut odds (≈45bps) raise discount rates for long-duration growth names, pressuring Nasdaq >1% downside sensitivity per 100bps move in yields. Risk assessment: Tail risks center on geopolitics (Taiwan-China escalation) and export-control shocks that could instantaneously remove >20–30% of advanced-node capacity, or conversely lead to supply-chain bifurcation with 10–20% higher costs for Western firms. Near-term (days–weeks) risks: Fed commentary and macro prints; medium-term (3–12 months): earnings and capex deployment; long-term (2–5 years): realized capacity additions and secular AI adoption curves. Trade implications: Favor selective long exposure to TSM (TSM) and upstream equipment (ASML, LRCX) to capture capex-driven revenue growth, funded by trimming long-duration mega-cap tech and buying rate-hedges; size 2–4% position in TSM with a 9–12 month horizon. Fixed income: prefer short-duration IG and floating-rate paper while using modest 2s10s steepener exposure if yields retrace >20bps. Options: consider 9–12 month call spreads 10–20% OTM on TSM/ASML and buy puts on QQQ to hedge macro rates risk. Contrarian angles: Consensus focuses on Fed and geopolitical downside, underweighting durable AI-driven capex which could lift semi-equipment revenues by >25% y/y for multiple quarters; however markets may be underpricing a 2028–29 supply rebalancing risk that could flip into margin pressure. Historical parallel: 2017–19 capex surge led to a 2–3 year overhang—position sizing and option structures should reflect asymmetric outcomes (large tail loss from geopolitics vs multi-quarter upside from AI demand).

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

-0.05

Ticker Sentiment