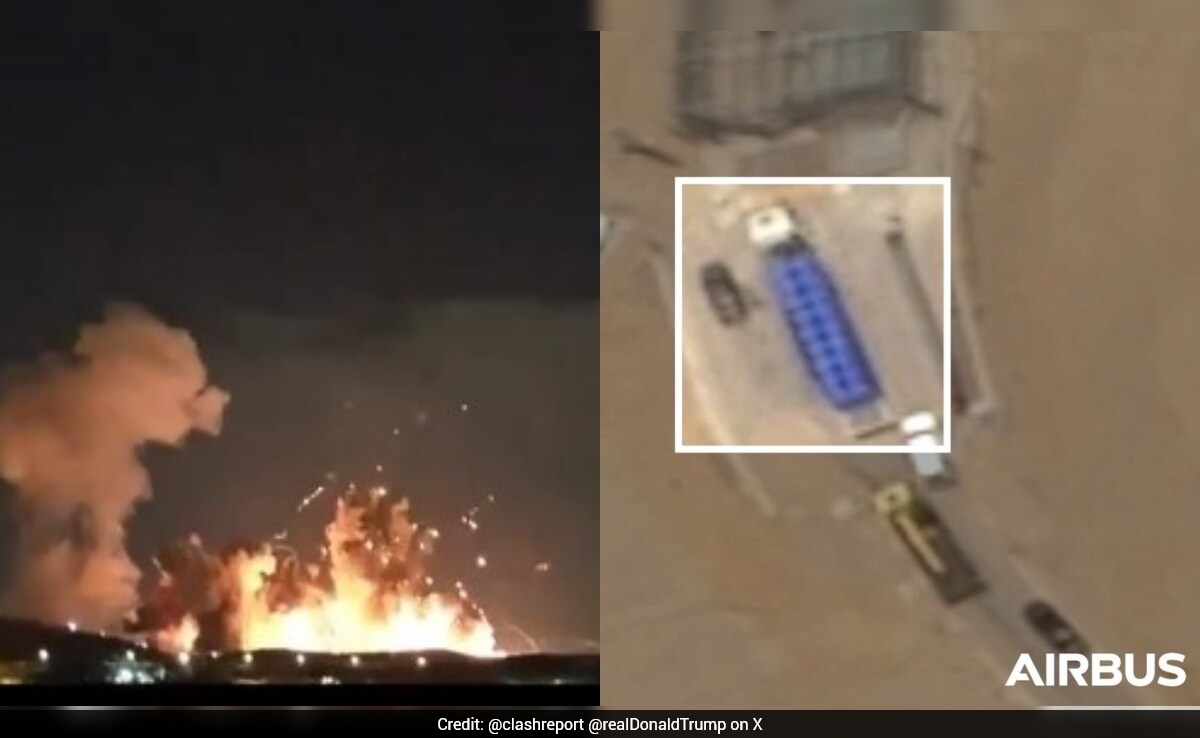

The US struck a large ammunition depot in Isfahan using 2,000-pound (≈907 kg) bunker-buster bombs, a major escalation in the Iran–US conflict. Satellite analysts say a truck likely moved up to ~534–540 kg of highly enriched uranium to an underground Isfahan facility days before June 2025 strikes, raising the risk the target included nuclear stockpiles. Iran has blocked the Strait of Hormuz — which handles roughly 20% of global oil flows — and markets warn oil could spike toward levels last seen in the 2008 commodity boom. Take a risk-off posture: this is a market-wide geopolitical shock with potential for rapid volatility across oil, shipping, and defense-related assets.

This strike materially raises the probability of sustained regional escalation that transmits to commodity markets via three channels: (1) chokepoint risk and insurance premia for tanker routes, (2) tactical missile/anti-ship attacks that reduce available fleet capacity, and (3) precautionary commercial rerouting that lengthens voyage times and raises bunker demand. Expect realized oil volatility to spike within 48-96 hours and implied vol to reprice higher for 1-3 month tenors; a 10-20% jump in tanker freight rates is plausible within the first two weeks if attacks persist. Second-order supply effects will favor floating storage/owners and midstream players able to capture time-charter premium; conversely, global just-in-time supply chains (chemicals, refined product arbitrage) will face margin compression from logistic re-routing and higher insurance costs. Industrial producers with significant feedstock hedges will temporarily win vs unhedged peers; large integrated majors will absorb price swings but independents capture more incremental free cash flow per $1 move in oil. Policy and counterparty risk creates a multi-month bid for defense OEMs and munitions supply chains but also raises single-event tail risks (port closures, sanctions-driven payment disruption) that can snap back quickly if a credible diplomatic off-ramp appears. Time-horizon: days for market shock and vol trades; weeks-to-months for freight/insurance repricing and defense capex re-rating; quarters for structural supply-chain reallocation and balance-sheet impacts on energy independents.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly negative

Sentiment Score

-0.75