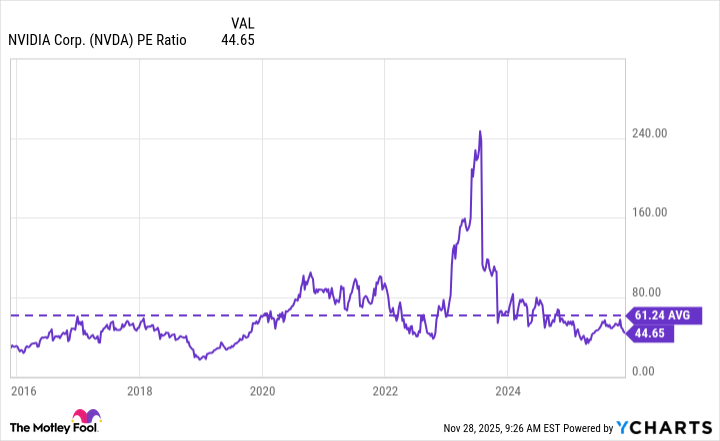

Alphabet’s Nov. 18 launch of Gemini 3 — trained exclusively on its in‑house TPUs — has been judged best‑in‑class and is driving strong demand for Google Cloud’s TPU capacity. Google Cloud reported Q3 2025 revenue of $15.1 billion, up 33.5% year over year, and an order backlog that surged 82% to $155 billion, while Anthropic and Meta are expanding TPU commitments (Anthropic up to 1 million TPUs; Meta reported talks to buy TPUs starting 2027). The development poses a competitive threat to Nvidia’s GPU dominance but Nvidia retains advantages (CUDA ecosystem, GPU versatility) and appears attractively valued (P/E 44.6 vs 10‑yr avg 61.2) alongside Alphabet (P/E 31.2), supporting a case for owning both names amid growing AI infrastructure spending.

Market structure: Alphabet (GOOGL/GOOG) is the immediate beneficiary — TPU exclusivity and a $155bn order backlog imply multi-year pricing power in cloud AI capacity, supporting cloud revenue growth (>30% YoY) and margins. Nvidia (NVDA) is exposed to share erosion for large-scale training clusters but retains ecosystem advantages (CUDA, versatility) that blunt rapid displacement; Jensen Huang's $4T TAM by 2030 implies room for multiple winners. Cross-asset: expect rising NVDA equity volatility and wider credit spreads for GPU suppliers if market-share fears spike; GOOGL credit/cash-flow outlook should improve, tightening its spreads; semiconductor capital goods (TSMC/ASML) demand is a secondary beneficiary. Risk assessment: Tail risks include regulatory intervention (antitrust or export controls) around TPU licensing, foundry shortages delaying TPU scale-up, and a faster-than-expected CUDA migration by frameworks (XLA/JAX) that accelerates switching. Near term (days–weeks) look for sentiment swings on partnership headlines (Anthropic/Meta); mid-term (6–18 months) is TPU capacity ramp; long-term (2–5 years) is sustained share shift if software portability reaches parity. Hidden dependencies: TPU proliferation hinges on software stack maturity and third-party sales strategy; Meta/Anthropic commitments are key catalysts. Trade implications: Tactical allocation favors GOOGL long-duration exposure (12–24 months) to capture cloud margin expansion and TPU pricing; keep NVDA long for platform exposure but hedge near-term downside via put spreads. Construct a relative-value pair (long GOOGL, short NVDA) to express platform-over-hardware preference if TPU adoption accelerates; size based on conviction and volatility (suggest 0.6 NVDA notional vs GOOGL). Options: buy NVDA 3–6 month 10% OTM put spread to hedge 20–30% downside; buy GOOGL 12–18 month calls (LEAP) to capture asymmetric upside. Contrarian angles: Consensus underestimates software lock-in — CUDA migration costs mean displacement will be gradual, so NVDA structural decline is not binary; current sentiment may be overstating immediate threat. Historical parallels: incumbent hardware winners (e.g., Intel/GPUs in past AI cycles) show that ecosystem and developer tooling slow transitions. Unintended consequence: Google selling TPUs could commoditize its cloud differentiation over time, inviting price competition and regulatory scrutiny — monitor backlog growth and TPU sell-through metrics as early warning signals.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment