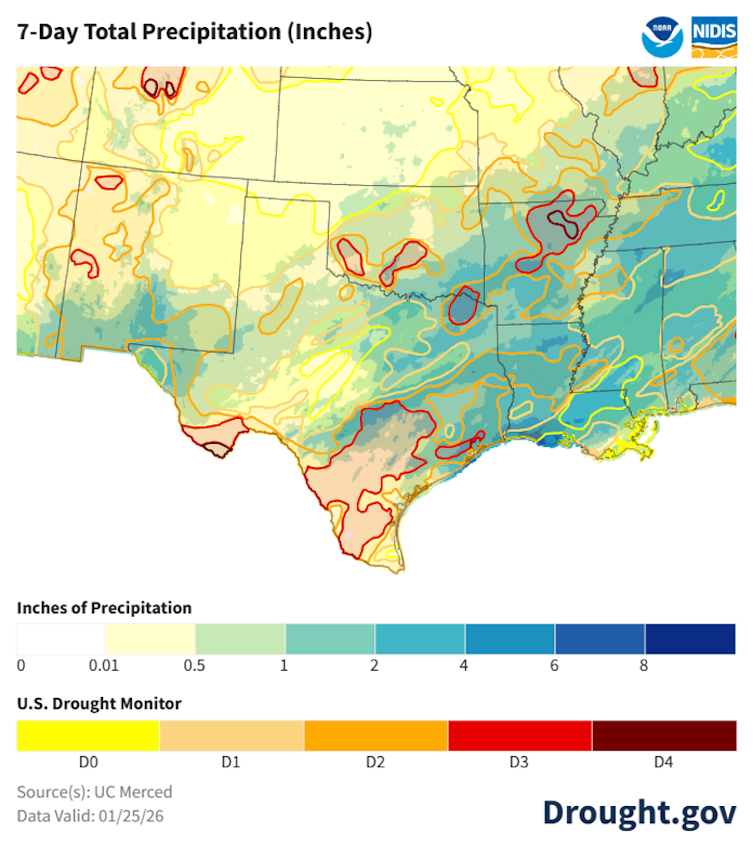

A multiyear drought across the Southern Plains since 2020 has inflicted roughly $23.6 billion in agricultural losses across Kansas, Oklahoma and Texas from 2020–2024, driving mass livestock liquidations (e.g., a 24-hour June 2022 auction of >4,000 cattle) and significant herd reductions (Texas 13.1M→12M; Oklahoma 5.3M→4.7M; Kansas 6.5M→6.15M). Major crop failures in 2022 included 25% of Texas corn and 45% of soybeans abandoned, and cotton output collapsing from a normal $2.4B to ~$640M after 74% abandonment; reservoirs and aquifers are at record lows (e.g., Elephant Butte 11%, Amistad 34%, Falcon 20%, Edwards Aquifer servicing ~2.5M people). Drivers are rising temperatures, repeated La Niña patterns and depleted water supplies, implying continued supply-side stress for agricultural commodities unless sustained multi-month precipitation arrives.

Market structure: The persistent Southern Plains drought tightens animal-protein and feed markets — Texas herd fell ~8.4% (13.1M→12M), Oklahoma ~11.3% and Kansas ~5.4% from 2020–24 — signalling a multi-year constrained beef supply and upward pricing power for processors/wholesalers. Winners: beef processors (margin capture), commodity traders and short-term livestock futures; water infrastructure/irrigation equipment and regulated utilities (capex-funded revenue). Losers: cow-calf ranchers, row-crop growers in the region, and regional banks with concentrated agricultural portfolios. Risk assessment: Key tail risks include a prolonged La Niña (worse drought, 1–3 year supply shock) or an early El Niño (rapid relief causing 20–40% mean reversion in futures within 12–18 months). Hidden dependencies: Rio Grande reservoir levels and Colorado snowpack drive irrigation capacity; municipal bond issuance and regulatory water restrictions can accelerate capex or impose costs on ag producers. Catalysts to watch in the next 30–90 days: NOAA ENSO updates, USDA Cattle-on-Feed (monthly), and May–July planting/WASDE reports. Trade implications: Near-term (0–6 months) favor long live-cattle and corn/soy call exposure; medium-term (6–24 months) overweight water utilities and irrigation OEMs for a multi-year capex cycle. Hedge regional-bank and ag-credit risk with targeted put protection. Use option spreads to control gamma given ENSO-driven volatility. Contrarian angles: Consensus expects permanently higher protein prices; that can be overstated if El Niño delivers above-normal fall/winter precipitation — a 12–24 month rapid herd rebuild is plausible once two consecutive good seasons occur. Water-capex beneficiaries are under-owned and may re-rate ahead of visible revenue in 12–36 months; conversely, fertilizer names may be over-owned into planting-cycle uncertainty.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

strongly negative

Sentiment Score

-0.60