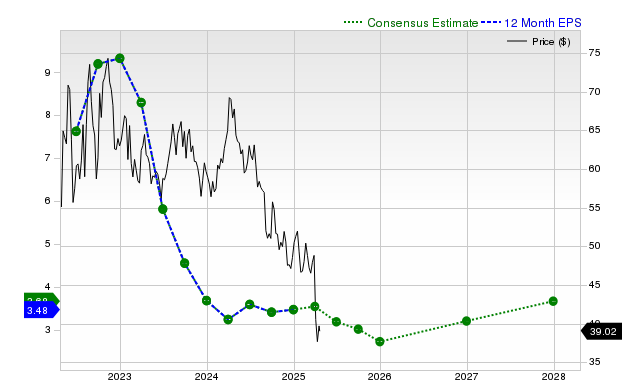

Occidental Petroleum (OXY) shares have outperformed the S&P 500 and its industry over the past month, returning +6.3%. Despite this recent strength, the company faces projected year-over-year declines for the current quarter's EPS (-51%) and revenue (-7.2%), though full-year earnings estimates have seen slight upward revisions recently. While OXY has consistently beaten EPS consensus in prior quarters and is graded 'A' for value, indicating a discount to peers, its Zacks Rank #3 (Hold) suggests near-term performance is expected to be in line with the broader market.

Occidental Petroleum (OXY) has demonstrated significant recent stock price momentum, with a +6.3% return over the past month that outpaced both the S&P 500 composite and its industry group. However, this performance is juxtaposed with a challenging near-term fundamental outlook. Consensus estimates for the current quarter point to a substantial year-over-year contraction, with earnings per share (EPS) projected to decline by 51% to $0.49 and revenue by 7.2% to $6.64 billion. For the full fiscal year, analysts anticipate a 34.7% drop in EPS and a 0.9% dip in revenue. While the company has a strong history of positive EPS surprises, as seen in its +39.29% beat last quarter, it missed revenue expectations in the same period. The earnings estimate revision trend is mixed; the current quarter's estimate has been revised down 4.8% in the last 30 days, but the full-year estimate has been revised up 1.3%. Despite the weak growth profile, the stock holds a Zacks Value Style Score of 'A', indicating it trades at a discount to its peers. The overall picture, synthesized into a Zacks Rank #3 (Hold), suggests the stock is likely to perform in line with the market, balancing its attractive valuation against deteriorating earnings forecasts.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

0.15

Ticker Sentiment