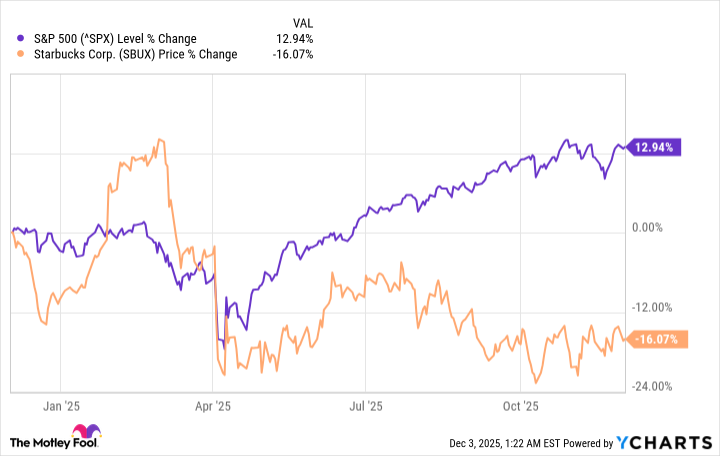

Starbucks posted fiscal 2025 GAAP net income of $1.86 billion, a 51% decline versus fiscal 2024, while net revenue rose by less than 3% to roughly $32.2 billion. Full-year global comparable-store sales fell 1%, with both the U.S. and China declining, and the stock has materially underperformed the S&P 500 over the one-, three- and five-year horizons. Management under new CEO Brian Niccol has launched a "Back to Starbucks" turnaround emphasizing in-store experience, but early execution appears to have had limited impact, leaving fundamentals and customer traffic trends as key downside risks for investors.

Market structure: Starbucks' 51% GAAP net-income collapse to $1.86bn and only ~3% revenue growth to $32.2bn with global comps down 1% signals weaker pricing power and footfall versus peers. Winners include low-cost channels (QSRs, supermarket coffee brands) and delivery/third‑wave independents that can undercut store economics; losers are mall/high‑street landlords and marginal company‑owned stores. Cross‑asset: expect modest equity beta lift and implied volatility in SBUX options; corporate credit spreads could widen modestly if the share price drop reflects sustained profitability pressure; global green coffee demand impact is immaterial near term but watch beans if comps worsen materially. Risk assessment: Tail risks include an operational shock (large union strikes or China re‑lockdowns) that could force >10% incremental annual EPS downside, or management misexecution of the “Back to Starbucks” rollout causing permanent traffic loss. Immediate (days) risk = headline volatility around monthly comps; short term (weeks–months) = guidance revisions and margin compression from labor/real‑estate actions; long term (12–24 months) = successful turnaround under Brian Niccol could restore margins. Hidden dependencies: loyalty/Digital penetration and store productivity metrics (avg ticket, visits per member) will determine recovery speed. Trade implications: Short‑bias is favored tactically: use options to control capital — e.g., a 6–9 month put spread 15–25% OTM to express downside (1–2% portfolio risk). Pair trade: go long CMG (Chipotle) and short SBUX to capture secular share shift; size long CMG at ~1% and short SBUX at ~2% for 3–12 month horizon. If long, sell 3‑month covered calls at +10% to monetize elevated IV; otherwise accumulate SBUX only on confirmed sequential comp improvement over two quarters. Contrarian angles: The market may be over‑pricing permanent traffic loss; Starbucks’ 100m+ loyalty base and supply scale are durable assets that could produce 30–50% upside if management pivots successfully within 12–24 months. Historical parallel: McDonald’s post‑2015 experience program turnaround — need to see 2 consecutive quarters of positive U.S. comps and improving store throughput before declaring a durable recovery. Beware unintended consequences: aggressive buybacks or cost cuts that hollow out experience could further erode brand equity and make recovery harder.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

strongly negative

Sentiment Score

-0.70

Ticker Sentiment