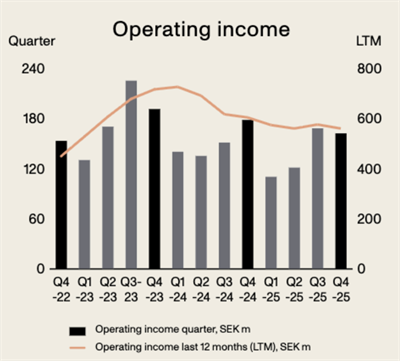

Duni Group reported FY2025 net sales of SEK 7,685m (up 1.4% YoY; +6.0% at fixed FX) and operating income of SEK 560m (down from SEK 604m), with EPS of SEK 6.64 (vs SEK 5.48) and adjusted EPS SEK 6.87 (vs 7.56). Q4 sales fell to SEK 1,965m (down 4.5% YoY; +1.5% at fixed FX) and operating income to SEK 162m, with management citing currency headwinds, weaker restaurant demand and negative mix effects partially offset by acquisitions (Poppies, LinePack, ByGreen) and efficiency measures. The Board proposes an unchanged dividend of SEK 5.00 per share and has set new Group targets effective 2026; risks include continued soft end‑market demand and FX pressures, while acquisitions and cost actions underpin medium‑term recovery prospects.

Market structure: Duni (Nasdaq Stockholm: DUNI) is consolidating the fragmented tableware/food-packaging niche via three acquisitions, which increases scale vs smaller local players and improves negotiated input/logistics pricing. Current weakness (Q4 organic -7.0%, FY organic -2.1%) signals demand softness in out-of-home dining (German visits -4%), pressuring pricing power for mid‑price SKUs but favoring larger multi-channel groups that can shift mix to retail and premium sustainable lines. Risk assessment: Key tail risks are a deeper European consumer downturn (GDP drop >1% YoY), reversal of the Germany VAT cut, or raw-material shocks (pulp/petrochemical price spikes >20%) that compress margins beyond the ~200–400bp uplift management targets. Immediate risk window (days-weeks) is FX volatility (SEK vs EUR/THB) and possible one-off restructuring costs; medium-term (3–12 months) depends on integration execution and synergy delivery; long-term hinges on sustainable demand recovery and ESG-driven premium pricing. Trade implications: Expect modest upside if Duni converts acquisitions into 200–300bp margin expansion by H2 2026 — this favors relative longs in DUNI and selective short exposure to smaller pure-play disposables. Cross-asset: packaging credit spreads could widen 25–75bp if margins miss, while SEK weakness would boost reported sales but hurt input-cost-importers; pulp and bio-plastics prices are key commodity monitors. Contrarian angles: Consensus focuses on weak organic growth, underweighting structural benefits from scale, retail mix and sustainability premium (BioPak/Poppies). If Duni delivers visible margin recovery by two consecutive quarters (target: operating margin ≥8.5%), market may underprice re-rating of ~20–30% in EV/EBIT multiples. Conversely, integration failure would be a sharp de‑rating catalyst; valuation is therefore binary over 6–12 months.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.05