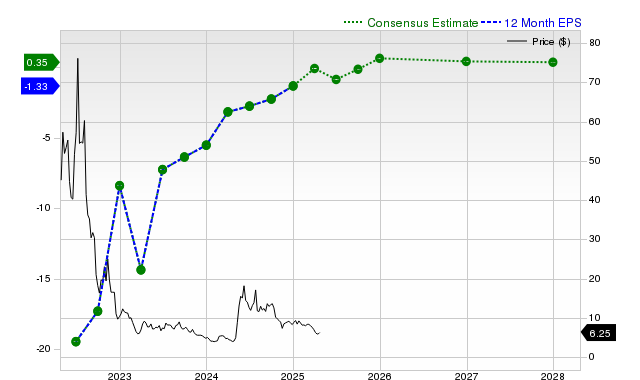

Novavax (NVAX) has recently outperformed, returning +17.3% over the past month, significantly exceeding the S&P 500. While the vaccine maker reported strong last-quarter results, beating revenue and EPS estimates by over 200% and 300% respectively, future earnings and revenue estimates present a mixed outlook with notable downward revisions for the next fiscal year. Despite this, the stock carries a Zacks Rank #3 (Hold), suggesting near-term performance in line with the broader market, and is assessed to be trading at a discount relative to its peers based on valuation metrics.

Novavax (NVAX) has exhibited strong recent price momentum, with shares returning +17.3% over the past month, significantly outpacing the S&P 500's +4.9% gain. This performance is backstopped by an exceptionally strong last reported quarter, where revenues grew 610.3% year-over-year to $666.66 million and EPS reached $2.93, beating consensus estimates by over 215% and 312% respectively. However, the forward-looking picture is deteriorating and presents a stark contrast. While the current fiscal year is projected to see a +301.6% YoY EPS increase, analyst estimates have been revised downward by 6.3% in the last 30 days. More critically, the outlook for the next fiscal year shows a dramatic contraction, with consensus estimates pointing to an 88.5% decline in EPS and a 48.6% drop in revenue. These future estimates have been aggressively revised downward over the past month, reflecting waning confidence in the company's growth sustainability. This mixed fundamental backdrop of strong trailing results versus a weak forward outlook is encapsulated by its neutral Zacks Rank #3 (Hold) and a 'B' grade for value, which indicates the stock is trading at a discount to peers but faces considerable uncertainty.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

0.00

Ticker Sentiment