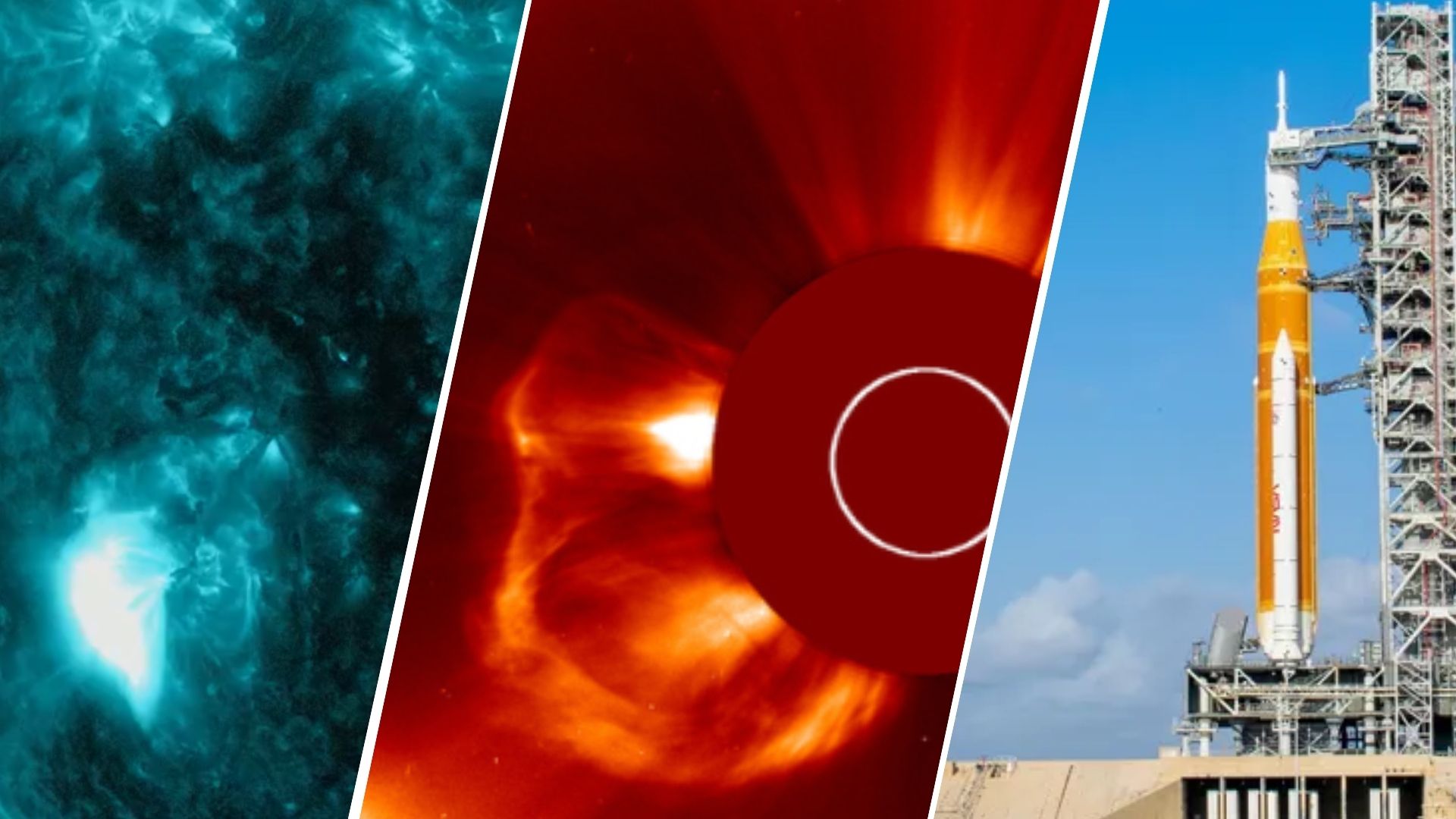

An X1.4 solar flare erupted March 30, peaking at 11:19 p.m. EDT (0319 GMT), causing HF radio blackouts across the sunlit side of Earth and launching a fast CME with a possible Earth-directed component. NASA's Artemis 2 launch (no earlier than April 1, 6:24 p.m. EDT) could face communication and early-orbit risks if solar activity intensifies; NOAA issued a G2 geomagnetic storm watch for March 31 and G1 conditions possible on March 30 and April 1. Active region 4405 is rotating into view, raising the chance of further impacts including auroras visible at lower-than-usual latitudes.

This episode sharpens a recurring second-order dynamic: episodic space weather shifts demand toward hardened, government-subsidized communications and away from fragile commercial satellite revenue streams. Expect a clustered reaction timeline — operational disruptions over 0–72 hours (HF/GNSS outages, temporary comm loss), and a separate market-repricing window over 1–12 months if any asset damage, launch delays, or insurance losses materialize. Supply-chain stress will be concentrated in a narrow set of suppliers: manufacturers of radiation‑hardened avionics, HF/VHF ground stations, and mission assurance contractors could see accelerated orders and margin tailwinds if agencies pre-position hardware or mandate retrofits; conversely, pure-play fixed-satellite-service operators and smallsat assemblers face concentrated downside from even single-vehicle losses because revenue per asset is high and replacement timelines are long. Budget flow is the key transmission mechanism — a few high-visibility anomalies can shift procurement into defense/bespoke space services for 12–36 months. Catalyst sequencing matters: near-term price moves will track CME arrival and geomagnetic indices (hours–days), while meaningful valuation rerates require tangible events (hardware failures, insured loss filings, or contract awards) that typically lag by weeks–months. Tail risk is asymmetric but low probability: a damaging CME that disables multiple GEO/LEO assets would create a rapid 20–50% revaluation in small/levered satellite names and a more muted 5–15% rerating in large, diversified defense contractors. The consensus underestimates the fiscal stickiness of procurement shifts once national security risk is invoked — agencies rarely reverse hardening investments once started.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.00