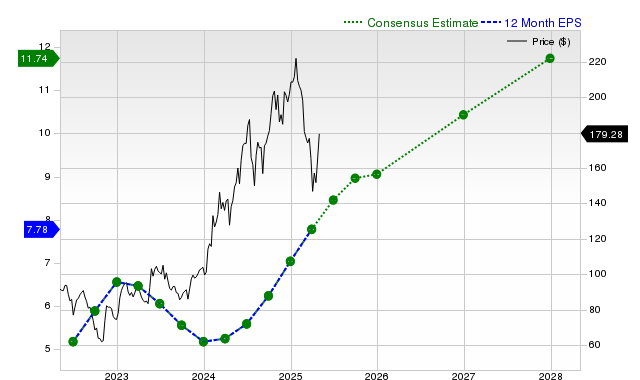

Taiwan Semiconductor (TSMC) reported robust trailing-quarter results with revenue of $33.1 billion (+40.8% YoY) and EPS of $2.92 (vs. $1.94 a year ago), beating consensus revenue and EPS by +5.06% and +12.74% respectively. Zacks consensus estimates call for current-quarter EPS of $2.72 (+21.4% YoY) and revenue of $32.6 billion (+21.3% YoY), with full-year and next-year earnings estimates of $10.14 (+44% YoY) and $12.19 (+20.2%), though those estimates were trimmed modestly (~-0.6%) over the past 30 days. Despite strong growth and consecutive beats, TSMC carries a Zacks Rank #3 (Hold) and a D value-style grade indicating a premium valuation, suggesting upside may be balanced by valuation and consensus positioning.

Market structure: TSMC’s beats tighten the premium node oligopoly — immediate beneficiaries are leading-edge users and capital-equipment suppliers (ASML, LRCX, KLAC) while trailing-node IDMs and memory vendors face further pricing pressure. Capacity remains the choke point: durable high-margin order flow implies pricing power for 3nm/5nm slots for the next 6–18 months, limiting near-term share gains by competitors. Risk assessment: Primary tail risks are geopolitical escalation around Taiwan, sudden export-controls widening, or a major fab outage; any of these could produce >30% downside in 1–3 months. Near-term (days–weeks) expect implied vol compression and guidance-driven swings; medium-term (3–12 months) watch customer order cadence and ASML delivery timing; long-term (12–36 months) the risk is capex-led oversupply that erodes ASPs and margins. Trade implications: Favor asymmetric exposure — express secular upside cheaply and monetize rich near-term premium. Prefer modest directional exposure sized 2–3% of portfolio, paired with income or defined-risk option structures and selective overweight to equipment suppliers; avoid naked long gamma until post-guidance clarity. Contrarian angles: Consensus pricing already embeds strong growth, so upside is crowded — a material miss or geopolitical shock would be amplified. Conversely, if AI/HPC demand continues, margins could outpace current estimates and justify re-rating; history shows foundry cycles flip from shortage to oversupply in ~12–24 months, so timing and structure matter more than outright bullishness.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment