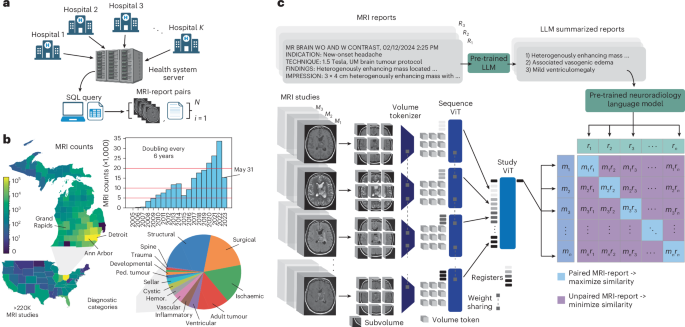

A University of Michigan team developed Prima, an AI foundation model for neuroimaging trained on a 221,147-study UM-220K dataset and prospectively tested on 29,431 MRIs, achieving a mean diagnostic AUC of 92.0% across 52 radiologic diagnoses and outperforming state-of-the-art models. Prima provides explainable differential diagnoses, worklist prioritization and referral recommendations, with model parameters and code released under an MIT license for investigational use though raw patient images remain restricted by IRB/data-use agreements. The performance and fairness results imply operational upside for radiology workflow efficiency and diagnostic accuracy, while commercialization and adoption will depend on regulatory clearance, data-sharing constraints and integration into hospital systems.

Market structure: Health‑system scale MRI foundation models materially shift economics toward compute/cloud and integrated OEMs. Primary beneficiaries: GPU vendors (NVDA), cloud hosts (MSFT, AMZN, GOOGL) and MRI OEMs (GE, PHG) via uplift in inference/upgrade demand; losers include niche, poorly capitalized med‑AI startups and staffing/teleradiology intermediaries facing margin compression. Expect 6–24 month higher demand for high‑end GPUs (constrained supply), and rising SaaS pricing power for inference services as hospitals pay per‑study fees. Risk assessment: Key tail risks are regulatory (FDA clearance delays or adverse CMS reimbursement decisions within 3–18 months), data‑privacy/IP litigation from training data provenance, and operational integration failures with PACS/EMR. Hidden dependencies: ongoing access to labeled reports, NVIDIA supply, and hospital IT integration; loss/constraint in any can cut addressable revenue by 20–40%. Catalysts: FDA AI frameworks, CMS CPT/reimbursement for AI triage, or enterprise contracts (each can accelerate adoption within 6–12 months). Trade implications: Tactical winners: NVDA (short‑dated call spreads 3–9 months), MSFT/AMZN/GOOGL (1–2% long positions, 6–18 months) for hosting/inference; strategic hardware plays: GE and PHG (1–2% longs, 9–24 months) for MRI upgrades and service revenue. Hedge regulatory risk with 6–12 month put protection on smaller healthcare‑IT names and prefer integrated incumbents over early‑stage pure‑play med‑AI stocks. Rotate capital from pure biotech R&D names into health‑tech/cloud over next 3–12 months. Contrarian angle: Consensus assumes rapid displacement of radiologists; real adoption is likely incremental (2–5 year curve) because of integration, liability and reimbursement friction — this undercuts valuations for early‑stage AI vendors and conversely means NVDA/cloud incumbents are underpriced for durable demand. Historical parallel: PACS/teleradiology adoption took multiple regulatory and reimbursement inflection points; watch for the same slow, stepwise revenue recognition and potential consolidation among med‑AI vendors.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.35