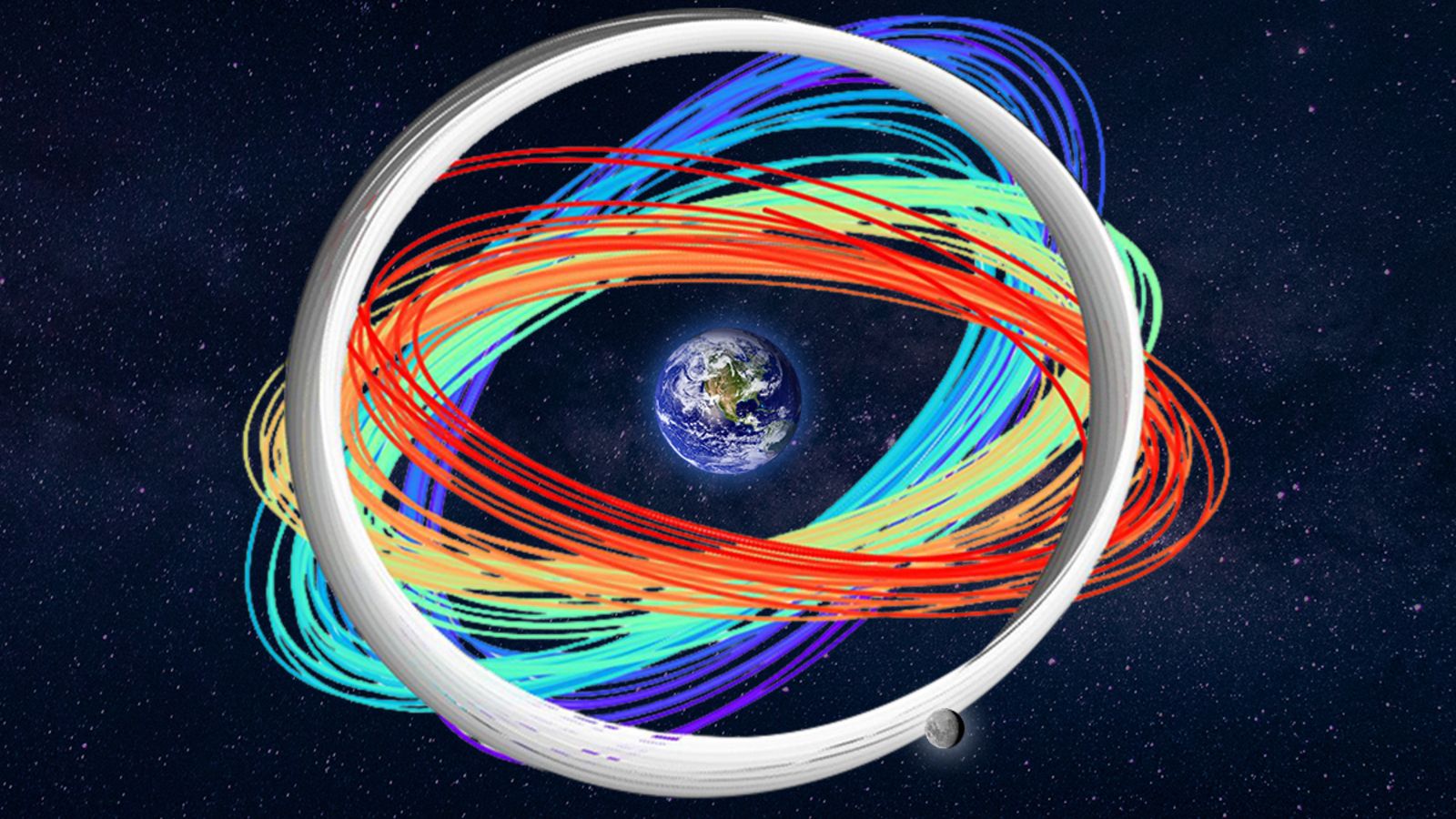

Lawrence Livermore National Laboratory used supercomputers Quartz and Ruby to simulate roughly 1 million cislunar satellite trajectories, consuming ~1.6 million CPU hours (a single machine would have taken ~182 years) and completing in three days. Results show ~54% of trajectories were stable at one year but only 9.7% remained stable over six years—equating to about 97,000 potentially viable cislunar orbits—highlighting the significant dynamical uncertainty (Earth–Moon–Sun gravitational interactions and Earth’s nonuniform gravity) that will shape commercial and national plans for off‑Earth infrastructure.

Market structure: Cislunar orbital instability reshuffles winners toward firms with simulation, launch, and risk-management scale rather than low-cost consumer-LEO plays. Expect defense primes (LMT, NOC, RTX) and established satellite integrators (MAXR, LHX) to capture higher-margin government and commercial cislunar services; constrained stable slots (~97k) imply scarcity pricing for qualified providers and ground/in-orbit insurance premiums rising 20–50% relative to LEO assumptions over 2–5 years. Risk assessment: Tail risks include a regulatory bottleneck (space-traffic management, spectrum allocation) or a geopolitical ASAT event that would force fleet recalls and spike replacement demand; probability medium but impact extreme (>$5–10B industry shock). Near-term (0–6 months) market impact likely muted; medium-term (6–24 months) depends on FY budget cycles and successful demos; long-term (2–7 years) is constructive for well-capitalized integrators and launch cadence scaling. Trade implications: Direct plays favor long positions in defense primes (LMT, NOC, RTX) and infrastructure/imagery (MAXR) and launch (RKLB) with 12–24 month horizons; short selective small-cap satcom entrants with weak balance sheets (e.g., ASTS-like names) where re-flight/insurance risk is highest. Use LEAP calls (12–24 months) to express asymmetric upside on MAXR/RKLB and calibrated put hedges on legacy commercial satellite operators if insurance spreads widen >30%. Contrarian angles: Consensus fixes on instability as a deal-killer; data shows ~97k viable orbits — large enough to support multi-billion-dollar markets, so initial fear is likely overdone. Historical parallel: LEO constellations (Iridium/OneWeb) required heavy capital but government anchor-tenants eventually monetized capacity; unintended consequence: congestion and liability costs concentrate power with large primes, accelerating consolidation and M&A in 2–4 years.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.10