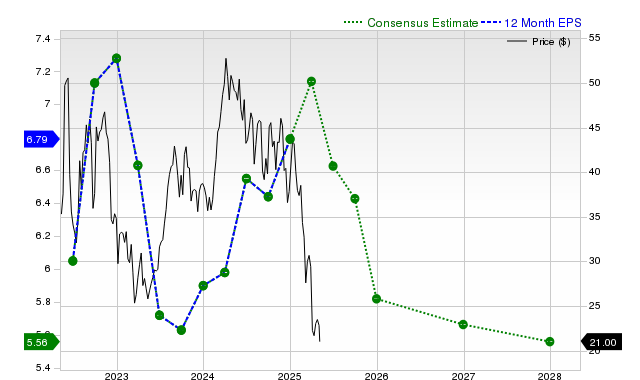

SM Energy (SM), an independent oil and gas firm, has recently underperformed the broader market and its sector, despite a history of beating analyst EPS and revenue estimates. While current fiscal year revenue growth is projected strong, earnings per share are forecast to decline year-over-year for both the current and next fiscal years, albeit with a recent positive revision for the current year. The stock holds a Zacks Rank #3 (Hold), indicating expected market-aligned near-term performance, and is assessed as trading at a discount to peers based on its Zacks Value Style Score of 'A'.

SM Energy (SM) presents a mixed financial profile, characterized by recent stock underperformance juxtaposed with strong operational results and a conflicting forward outlook. Over the past month, the stock returned -1.4%, lagging both its industry (+0.6%) and the S&P 500 composite (+0.9%). This is despite a history of positive surprises, including beating consensus EPS estimates for four consecutive quarters and delivering a +21.95% EPS surprise in its most recent report. The company's revenue picture is robust for the current fiscal year, with projections for +23.5% growth, including a +32% YoY increase in the current quarter. However, this top-line strength does not translate to profitability, as earnings per share are forecast to decline -13.8% in the current year and another -10.1% in the next. Analyst sentiment reflects this dichotomy, with a recent +2.7% upward revision to current-year EPS estimates but a -1.7% downward revision for the next fiscal year. While earnings face headwinds, the stock's valuation appears compelling, earning a Zacks Value Style Score of 'A', which indicates it is trading at a discount to its peers and supports its overall Zacks Rank #3 (Hold) rating.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

Neutral

Sentiment Score

0.00

Ticker Sentiment