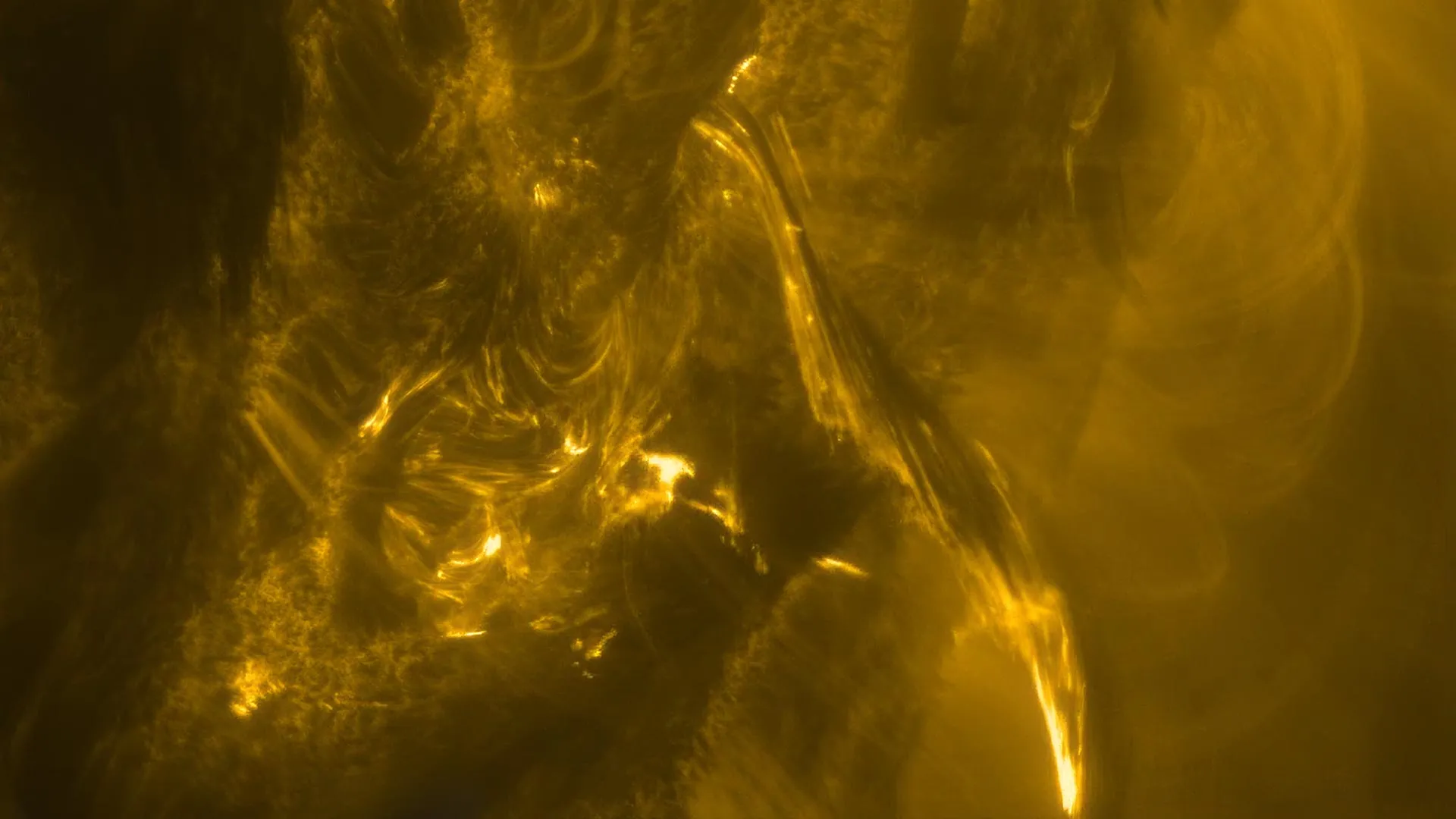

ESA's Solar Orbiter captured direct evidence that large solar flares can grow via a cascading 'magnetic avalanche,' based on high-cadence multi-instrument observations during a close pass on 30 September 2024 and reported 21 January 2026 in Astronomy & Astrophysics. The data — from EUI, SPICE, STIX and PHI — show sequential magnetic reconnection events accelerating particles to ~40–50% of light speed (≈431–540 million km/h) and producing prolonged streams of plasma blobs; the finding refines physical models of flare energy release and has operational implications for satellite operators, astronauts and power/communications infrastructure exposed to space weather.

Market structure: The primary winners are suppliers of space-weather sensors, radiation‑hardened electronics, and grid‑GMD mitigation gear (vendors can command +10–30% premium for hardened components); defense/space primes (LHX, LMT, NOC) and grid‑resilience OEMs (ETN, ABB) gain incremental durable demand. Losers are uninsured/under‑hardened smallsat operators and legacy satellite insurers that face higher loss frequency and tighter underwriting cycles, pressuring margins by potentially >5–10% during active years. Risk assessment: Tail risk remains low‑probability but high‑impact (Carrington‑class event <1% per decade) capable of multi‑week outages and multi‑% GDP disruptions to developed markets; price effects can be immediate (days) for satellite equities, short‑term (weeks–months) for insurance repricing, and long‑term (quarters–years) for capex cycles in grid and space sectors. Hidden dependencies: concentration in a few radiation‑hardened component suppliers and insurance Retro loss models; monitor NOAA SWPC Kp≥7 or >X‑class flare counts as operational triggers. Trade implications: Tactical allocation into defense/space suppliers and grid‑protection equipment is warranted: these names should outperform if government procurement and commercial hardening accelerate over 6–24 months. Cross‑asset: expect modest safe‑haven flows (USD, JPY, gold) and potential flight to quality in US T‑bonds during big storm alerts; commodity impacts (oil/gas) are second‑order unless extended grid outages occur. Contrarian view: The market likely understates multi‑year capex reallocation toward hardening—initial scientific results rarely move revenue next quarter but do shift procurement roadmaps over 12–36 months. Avoid crowded long‑defense consensus; where underwriting repricing is imminent, insurers may actually benefit after a 12–24 month premium reset, creating late‑cycle longs in reinsurers at cheaper multiples.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.05