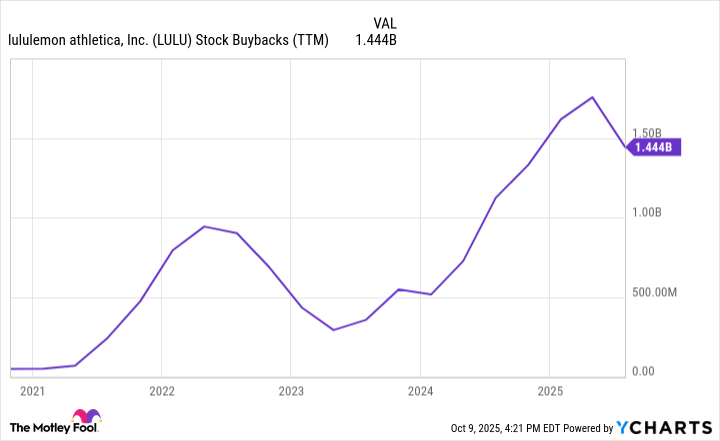

Lululemon's stock has experienced a significant decline amid slowing North American revenue and increased competition, yet the company reported 1% year-over-year growth in the region, outperforming peers. The athleisure brand is demonstrating robust international expansion, particularly in China with 24% constant dollar revenue growth, and holds substantial untapped potential in Europe and Latin America. Management is actively enhancing shareholder value through a $1.444 billion share buyback program over the past year, representing a 7% yield, while the stock's current P/E of 12 is notably below the S&P 500's average of 30, positioning it as a compelling long-term growth prospect despite near-term market challenges.

Lululemon (LULU) shares have declined 66% from recent highs, primarily due to slowing North American revenue and heightened competition in the athleisure sector. Despite broader consumer spending trends impacting the apparel space, LULU's Americas revenue still grew 1% year-over-year last quarter, significantly outperforming competitors like Athleta, which saw a 9% decline. This suggests Lululemon is gaining market share in the premium segment, supported by a new marketing partnership with American Express. The company exhibits robust international expansion, particularly in China, where revenue surged 24% year-over-year in constant dollar terms, reaching $1.5 billion over the last twelve months. Significant untapped potential exists in Europe and Latin America, exemplified by a new flagship store in Milan. Management projects total annual sales could reach $20 billion to $30 billion within the next decade, driven by this global growth and a potential North American recovery. Lululemon's valuation appears compelling, with a trailing price-to-earnings (P/E) ratio of 12, substantially below the S&P 500 average of 30. The company actively enhances shareholder value through capital allocation, having repurchased $1.444 billion worth of stock over the last 12 months, representing a 7% buyback yield against its $20 billion market capitalization. This strategy is expected to accelerate earnings per share growth despite anticipated tariff-related headwinds.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly positive

Sentiment Score

0.80

Ticker Sentiment