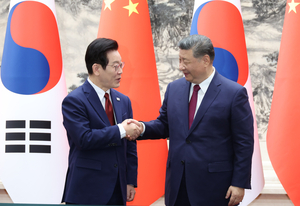

South Korean President Lee Jae Myung and Chinese President Xi Jinping held a 90-minute summit in Beijing where they agreed to gradually reopen cultural and content exchanges, opened consultations on China-built structures in the jointly managed Provisional Measures Zone of the West (Yellow) Sea, and pledged continued cooperation on North Korea and fishing enforcement. The talks — attended by senior security, economic and technology ministers, including officials responsible for AI, commerce and industry — signal a coordinated push to steady bilateral ties and rebuild practical economic and technological cooperation. For investors, the outcome modestly reduces geopolitical tail risk between Seoul and Beijing and raises a limited upside catalyst for South Korean media and content companies should Beijing ease the informal Hallyu restrictions.

Market structure: Immediate winners are Korean exporters of culture and consumer services — listed media/entertainment (e.g., HYBE 352820.KS, CJ ENM 035760.KS) and tourism-linked names — plus broader Korean equity exposure (EWY) as bilateral flows normalize; losers are Chinese domestic streaming incumbents if cross-border licensing flows increase. Pricing power for top-tier Korean IP owners can expand quickly (we model incremental licensing revenue of +10–25% over 6–12 months if bans ease), while marginal content producers face more competition and possible compression in licensing margins. Risk assessment: Key tail risks are a North Korea provocation or a US-China flare-up that re-tightens Chinese controls (assigned combined ~20% probability over 12 months) which could wipe 5–15% off Korean media/tourism names. Near-term (days) volatility is likely around diplomatic headlines; medium-term (3–9 months) is driven by licensing agreements and travel reopenings; long-term depends on structural tech cooperation and supply-chain policy shifts. Trade implications: Implement directional Korea exposure via EWY call spreads (3–9 months) and selective longs in HYBE/CJ ENM sized to conviction (1–3% positions), funded by modest shorts in China internet exposure (KWEB or BABA) to hedge regulatory asymmetry. FX: expect KRW appreciation of 2–4% over 3–6 months if sentiment holds; use small forward positions or FX ETFs to capture this. Contrarian angles: Consensus underestimates speed and multiplier of cultural reopening — THAAD-era precedents show 20–40% rebounds in top Korean entertainment stocks within 6–12 months after policy reversals. Beware the market overstating a full, permanent lift; China may reopen selectively, so favor large-cap IP owners with diversified revenue (concerts, merchandising, streaming), and keep option hedges to protect against abrupt reversals.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.25