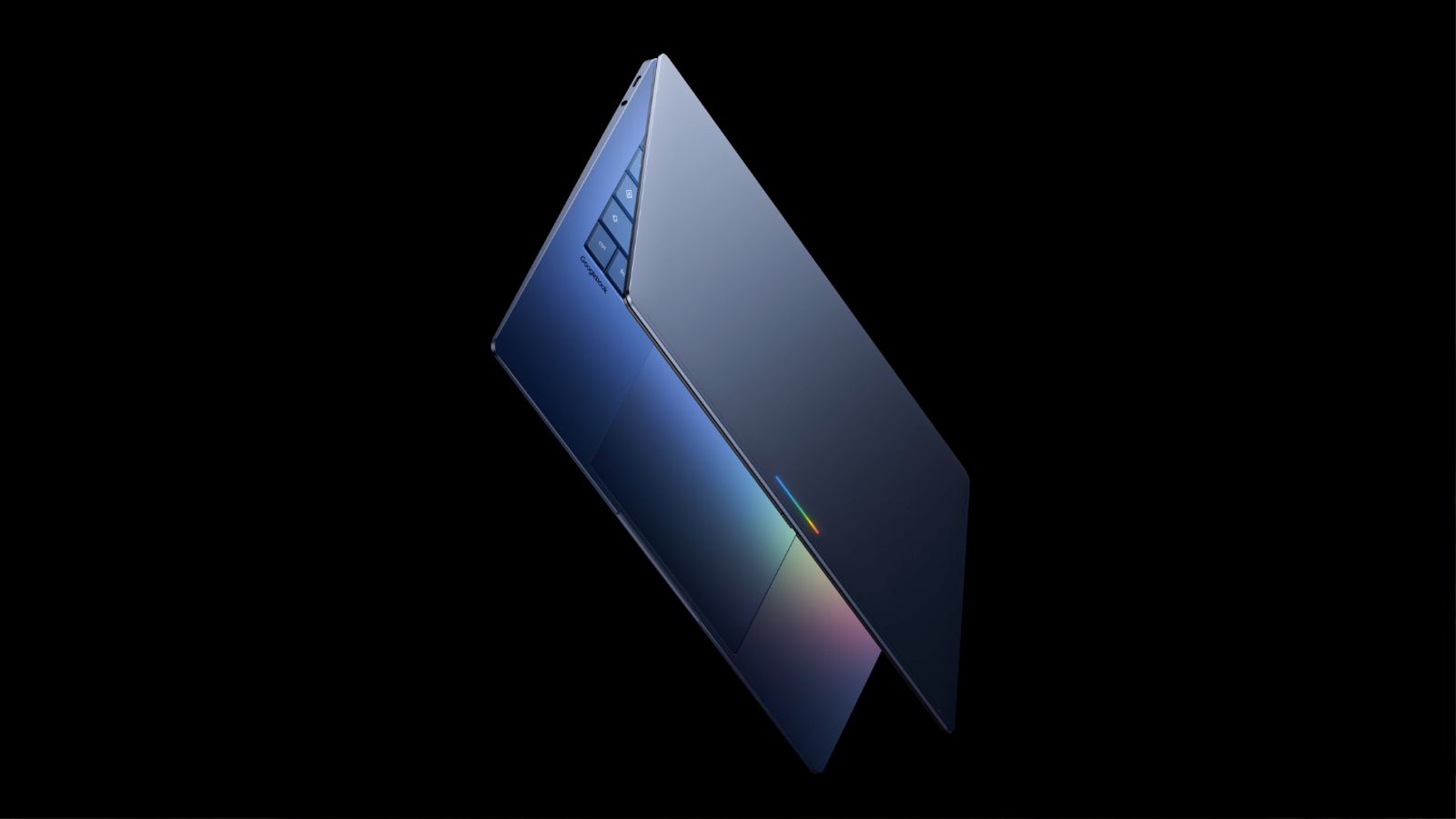

Google announced a new Googlebook laptop line built around Gemini, with a combined Android-ChromeOS foundation, Magic Pointer controls, and deeper integration with Gmail, Calendar, and Android phones. The first models will be produced with Acer, ASUS, Dell, HP, and Lenovo and are set to launch this fall. Pricing was not disclosed, but Google signaled a premium build that could position the devices against Apple’s MacBook Neo.

This is less about a single laptop launch and more about Google trying to turn Android into a cross-device operating system that can monetize attention across phone, laptop, and services. If the integration works, the durable benefit accrues to GOOGL because it raises switching costs and increases the surface area for Gemini subscriptions, search queries, and workspace attachment. The strategic threat is not immediate unit share loss for Apple; it is that Google can compress the product gap around ecosystem continuity, which has historically been one of Apple’s highest-conviction moats. The second-order winner is likely the ODM/PC supply chain if Google follows the usual playbook of multiple partners and premium positioning. DELL and HPQ can see a modest mix benefit from a halo effect and incremental commercial interest, but the real upside is if Googlebooks legitimize premium Android laptops and expand the category beyond a niche SKU. That said, margins for hardware partners may be capped if Google uses this launch primarily to defend ecosystem share rather than build a high-ASP franchise; volume could grow without translating into outsized profit pools. A key risk is execution drag: the product needs to be meaningfully better than “ChromeOS with AI” for consumers to pay up, and the fall launch leaves only a short window before holiday share decisions are made. If app continuity, widget creation, or phone-to-laptop mirroring is clunky, the market will quickly re-rate this as a demo-led announcement rather than a demand catalyst. Another overhang is pricing: if Google undercuts Apple aggressively, it could pressure hardware margins across the category while still failing to shift premium buyers. The contrarian take is that the near-term market may over-index on AAPL losing share, when the more probable outcome is a small but real improvement in Google ecosystem stickiness and search monetization per user. The bigger medium-term question is whether this turns Android into a credible productivity platform for enterprise, which would be a slower burn but more durable than consumer share gains. If that thesis holds, the first-order impact should show up in engagement metrics and cloud/app attach before it shows up in laptop shipment share.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.35

Ticker Sentiment