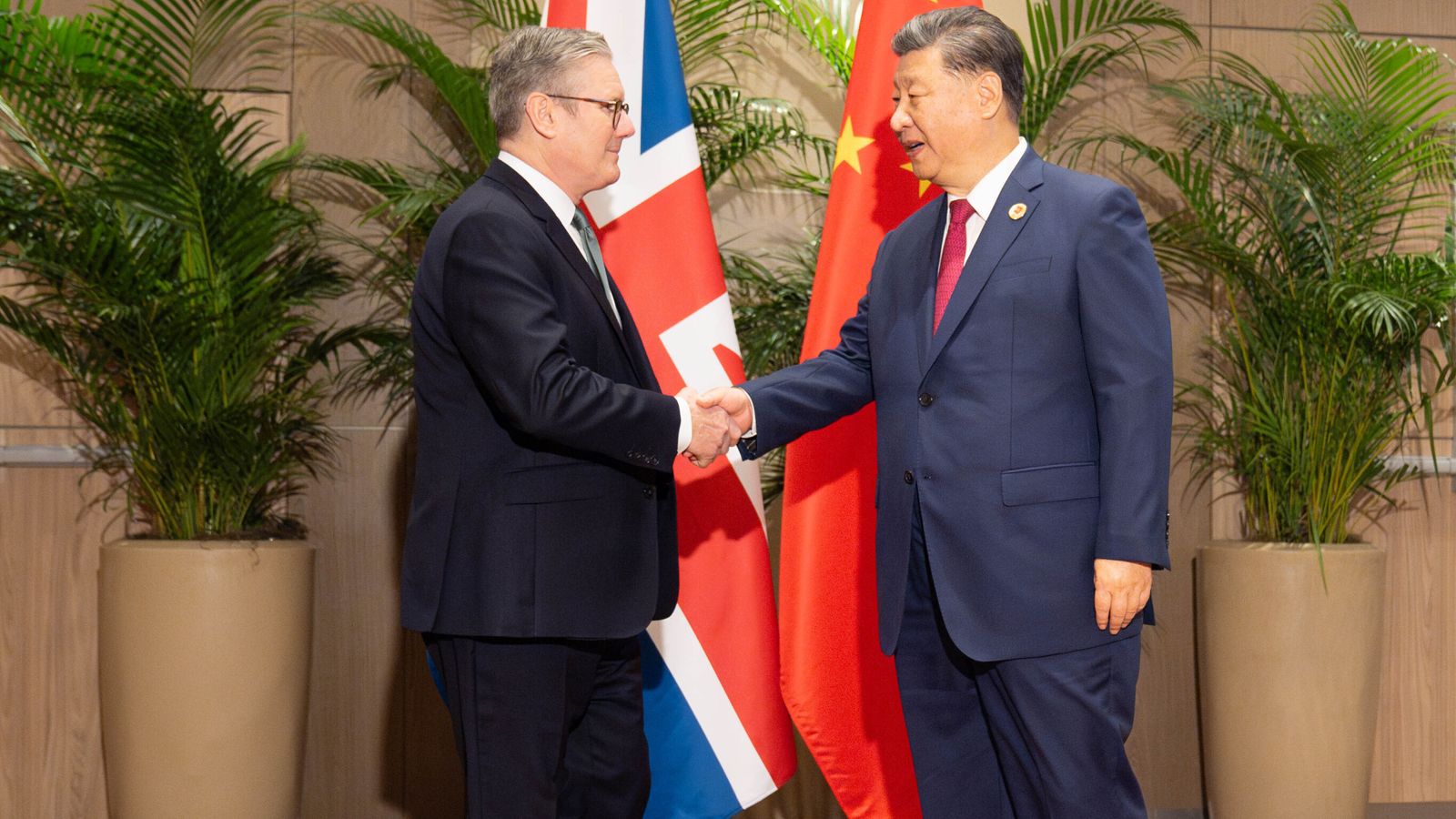

UK Prime Minister Keir Starmer's visit to China is primarily focused on reviving trade and investment ties—particularly services (legal, financial, education) and targeted sector deals such as renewable energy—while avoiding a full bilateral free‑trade agreement. The trip is constrained by significant political and national‑security frictions (espionage concerns, controversy over a new Chinese embassy in London), human‑rights disputes (Jimmy Lai), and geopolitical issues (Taiwan, Russia/Ukraine), so expect incremental market‑access measures rather than sweeping commitments; implications are strategically important but unlikely to trigger immediate large market moves.

Market structure: A cautious UK–China thaw primarily benefits UK services exporters (financial/legal/education) and non-Chinese infrastructure suppliers at the expense of China-centric tech names. Expect 5–15% relative re-rating potential over 6–12 months for winners (HSBA.L, PSON.L, ERIC/NOK) if incremental market-access deals materialize; China internet ETFs (KWEB, FXI) face continued downside pressure in the next 1–3 months due to optics and regulatory risk. Risk assessment: Tail risks include a diplomatic shock (e.g., escalation over Jimmy Lai or UK visa/embassy security incidents) that could trigger 10–30% drawdowns in China-exposed equities and abrupt regulatory decoupling. Near term (days–weeks) volatility will hinge on announcements during/within 30 days of the visit; medium term (3–12 months) depends on US policy spillovers and supply-chain repricing for semis/rare earths. Trade implications: Tactical trades favor short-duration China beta hedges and selective long exposure to defense/telecom suppliers and UK banks/education. Volatility will spike around announcements — use ST IR hedges (puts on KWEB/FXI) and call spreads on ERIC/NOK or long HSBA.L with tight stop-losses to monetize asymmetric policy signaling. Contrarian angle: Markets will overprice both the diplomatic optics and the policy breakthrough—China prefers symbolic gestures; real structural liberalisation is unlikely. That creates a mispricing window: short headline-sensitive China ETFs vs long specific UK service exporters and western telecom/defense suppliers into the 30–90 day news cycle.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mildly negative

Sentiment Score

-0.25