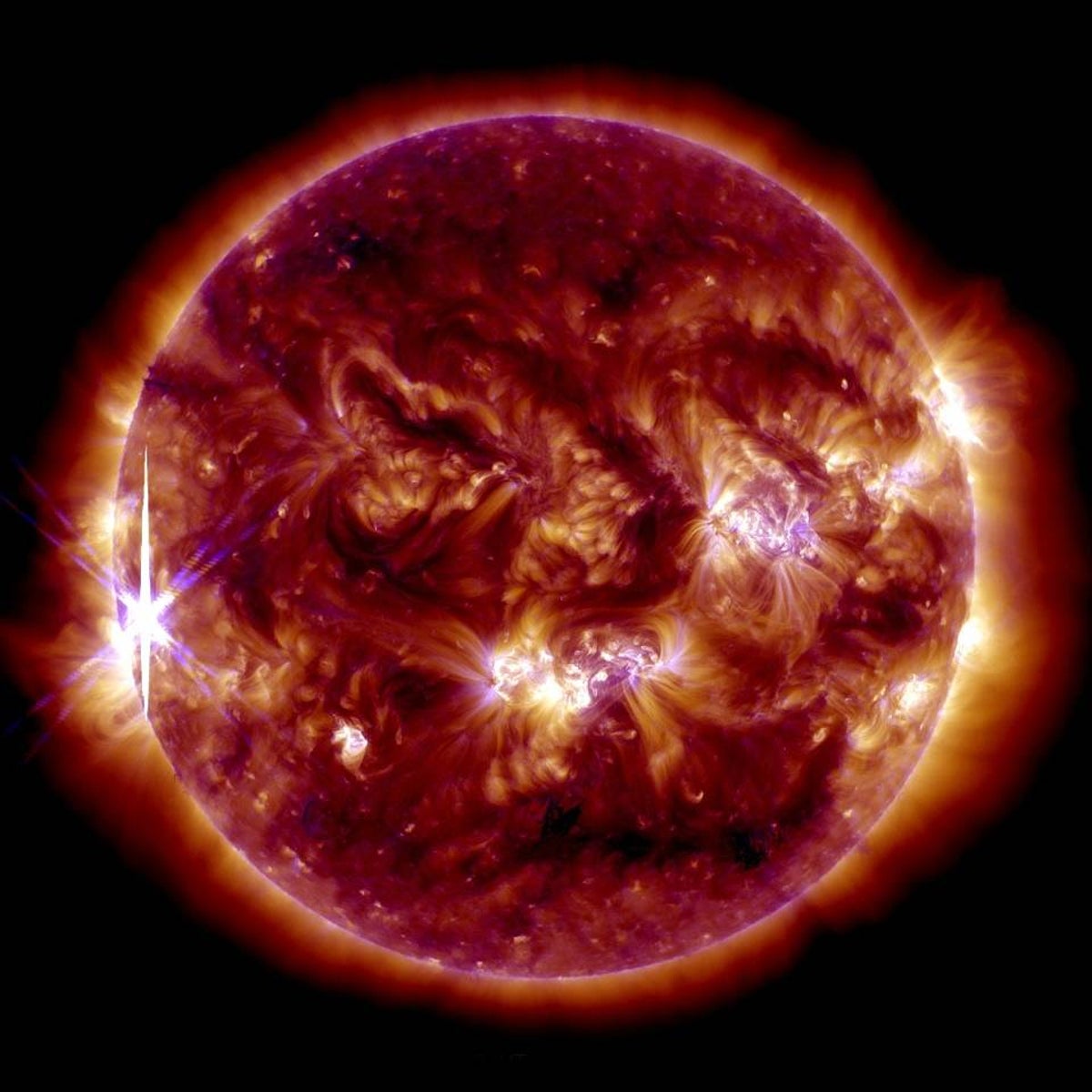

The sun produced multiple X‑class solar flares on Sunday, including an X8.1 eruption at 6:37 PM EST — the brightest flare since October 2024 and among the top 20 since 1996 — following an earlier X‑class event observed by NASA at 7:33 AM EST. NOAA’s Space Weather Prediction Center is monitoring the active region and expects most expelled plasma to reach Earth on Thursday, potentially creating auroras, with further strong activity possible as the solar cycle winds down.

Market structure: Major X-class flares increase near-term revenue/policy tailwinds for grid-hardening and space-resilience vendors (Eaton ETN, ABB ABB) while raising operating costs and disruption risk for airlines (AAL, UAL), GPS-reliant logistics and civilian satellites (VSAT, IRDM). Pricing power could shift modestly toward industrials and defense vendors if utilities accelerate transformer/SCADA spend; expect a 3–12 month pull-forward of replacement/refurbishment orders, not sustained secular demand. Cross-asset: expect short-lived safe-haven flows into USTs and gold (GLD) on confirmed geomagnetic storms, occasional spikes in natural gas and jet fuel if routings change; FX moves likely small unless a major outage triggers risk-off. Risk assessment: Tail risk remains a low-probability/high-impact Carrington-class event; model a 0.5–2% annualized probability but >$100B global economic shock if realized. Immediate window (days) risks are satellite comms/GPS anomalies and flight reroutes; short-term (weeks) risks include insurance claims and component lead-time shocks, long-term (quarters) involves utility capex and regulatory remediation. Hidden dependencies include transformer spare inventories (single-digit weeks) and concentrated suppliers; catalyst set: NOAA SWPC G-scale alerts, airline NOTAMs, FCC anomaly reports. Trade implications: Direct plays favor 2–3% tactical longs in ETN/ABB over 3–12 months and 1% gold (GLD) as a hedge; short 1–2% via 30–45d puts on AAL/UAL for operational disruption. Pair trade: long ETN vs short AAL to capture relative outperformance; options: buy 30–60d ATM calls on ETN and 30d 10–15% OTM puts on AAL/UAL, trim after CME passage (+7 days). Rotate 1–3% from growth/autonomous names into utilities and defense (RTX, LMT) if multiple G3+ alerts are issued. Contrarian angles: Consensus will likely underprice long-tail grid-replacement demand because of long lead times for large transformers (months–years); that suggests underowned industrials could re-rate 10–25% on incremental policy spend. Conversely, immediate market panic shorts on airlines may be overdone if the CME misses Earth or weakens — cap exits at 50% option premium gain or 7 days post-event. Historical parallels (1989 Quebec blackout, 2003 storms) show asymmetric outcomes: large regional impacts but rapid market normalization, so position sizes should be modest and time-boxed.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.00