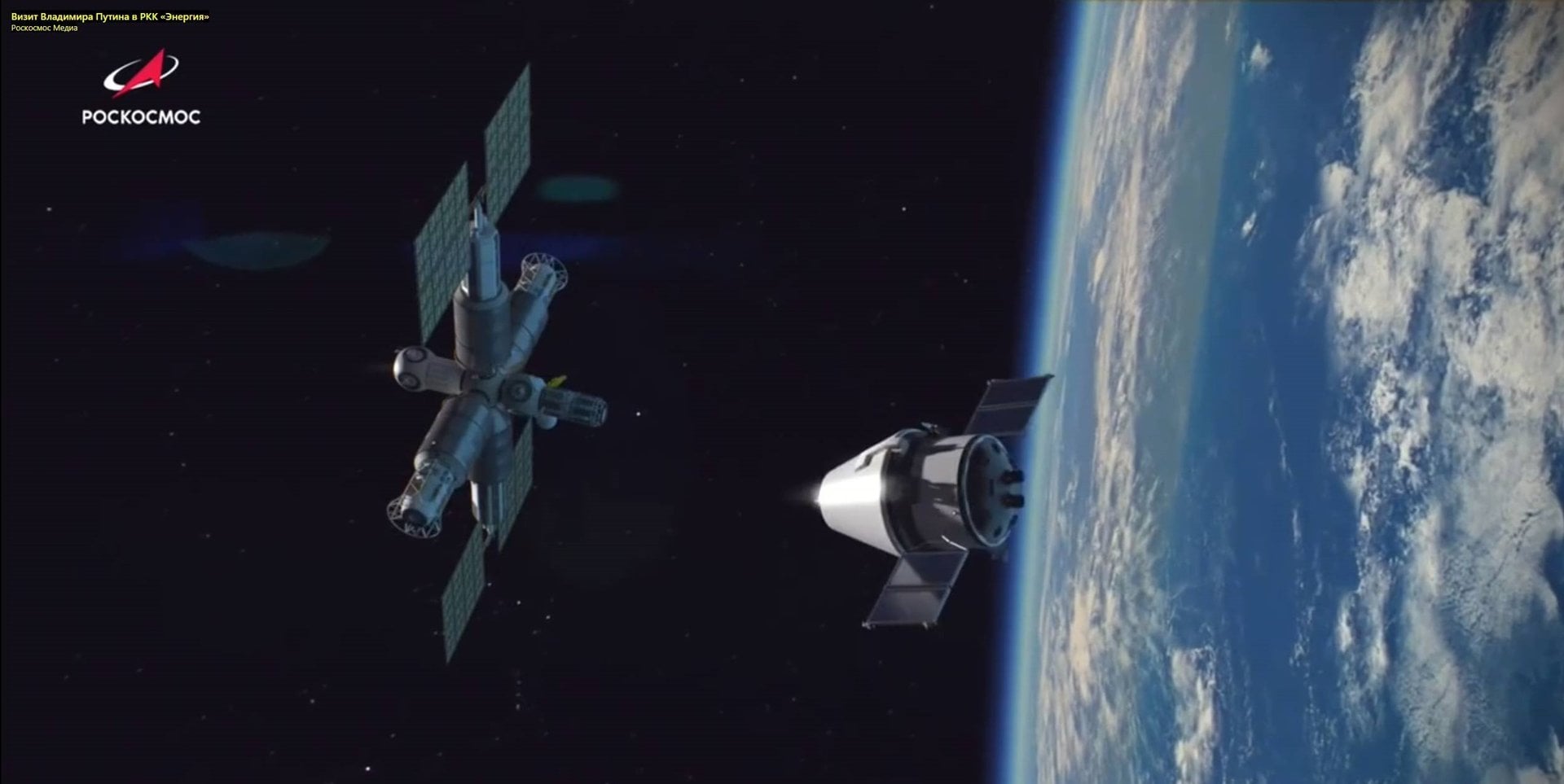

Russia announced plans to form a Russian Orbital Station (ROS) by separating its ISS modules — Zarya, Zvezda, Poisk, Rassvet, Nauka and Prichal — after the International Space Station retires in 2030, with the proposal disclosed by Oleg Orlov on Dec. 18 and an orbital inclination of 51.6° selected to enable launches from Plesetsk and Vostochny. The move follows earlier ROSS/OPSEK planning, reflects sanctions, damage to Baikonur and wartime budget pressure, and has prompted warnings about microbiological contamination, aging hardware and significant maintenance needs that could constrain scientific output and raise operational risk.

Market structure: The ISS retirement (2030) and Russia's plan to reuse modules shifts demand toward domestic launch, LEO habitats, and Western/Indian suppliers between 2025–2035. Winners: US/European defense primes (RTX, NOC, LMT), small‑sat launch/integration (RKLB, MAXR), composite/avionics suppliers; losers: Russian exporters, legacy ISS maintenance contractors, and speculative tourism plays that assume low CAPEX reuse. Expect 5–15% higher procurement pricing power for qualified Western vendors over 2025–2028 as governments de‑risk supply chains. Risk assessment: Tail risks include a major escalation in Ukraine (months) that triggers deeper sanctions and halts any joint programs, or a contamination/structural failure of recycled modules that raises orbital insurance premia by 50%+ and forces module write‑offs. Hidden dependencies: continued access to Baikonur alternatives (Vostochny/Plesetsk), RD‑family engine availability, and re/insurance capacity; budgets and Duma/Roscosmos funding votes in next 60–180 days are binary catalysts. Short‑term (days-weeks) market moves will be muted; medium/long (6–36 months) re‑rating likely. Trade implications: Position into US defense/space supply chain and LEO infrastructure: establish measured long exposure via equities and 12–24m call spreads (see decisions). Hedge FX and EM Russia exposure immediately (6–12m). Avoid or trim speculative space‑tourism equities (SPCE) and smallcaps lacking backlog; consider buying industry catastrophe/reinsurance names on weakness. Contrarian view: The market underestimates cost and timeline of refurbishing ISS modules—operational O&M could exceed new module capex, accelerating private/public demand for new stations and consolidating suppliers. History: post‑Cold War decoupling created multi‑year win streaks for Western primes; expect a similar 2–4 year window for outsized returns. Mispricing exists in speculative smallcaps; risk is consolidation not broad market growth.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.60