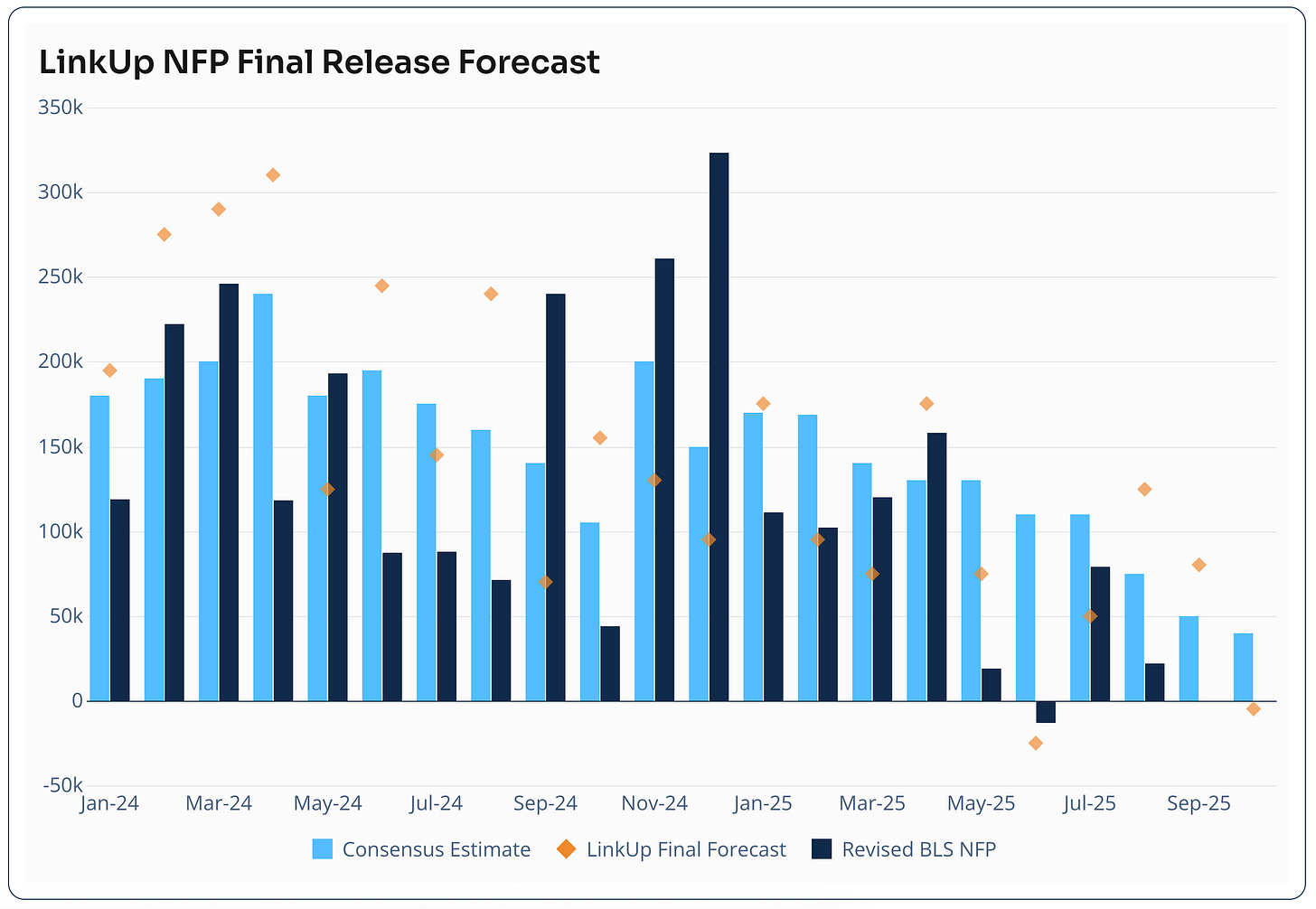

The federal shutdown has left the BLS October employment report incomplete, forcing the Fed to rely on private indicators that show clear cooling: ADP reported only +42,000 private jobs in October, Revelio Labs estimated a net loss of >9,000 jobs, LinkUp showed −5,000 listings and Indeed job postings have rolled back to 2021 levels. With job creation stalling across logistics, healthcare, retail and professional services and inflation remaining sticky—especially in services—the Fed faces a tradeoff between protecting employment and containing inflation; the piece expects a cautious path of easing with a likely December cut and a possible additional 25 bps in early 2026 conditional on further labor softening. Investors should position for volatility: favor high-quality fixed income and defensive sectors while avoiding speculative, high-beta assets as policy stays data-dependent.

Market structure: Cooling private payrolls (ADP 42k, Revelio -9k, job postings back to 2021 levels) shifts near-term winners to duration, high-quality corporates (LQD), and defensive sectors (XLU, XLP, XLV) while penalizing small caps, unprofitable tech, and crypto. If the Fed delivers a 25bp cut in Dec and another 25bp in early 2026 (author expectation), 10yr yields could compress 40–80bp over 3–6 months, boosting long-duration returns while steepening/flattening dynamics depending on growth surprises. Supply/demand: a demand-led slowdown (hiring freezes across logistics, healthcare, retail, professional services) implies lower labor-driven consumption, pressuring EBITDA margins in cyclical sectors, tightening credit spreads for lower-quality paper. Risk assessment: Immediate (days) risk is headline volatility from Fed comments and missing BLS prints; short-term (weeks–months) risk is an inflation surprise (services/wage pickup) that would reprice easing and widen risk premia; long-term (quarters) structural risks include AI-driven productivity deflation and demographic stagnation. Tail scenarios: (1) sticky services inflation → no cuts and a policy surprise, (2) rapid job losses → recession and credit stress, (3) liquidity shock in regional banks amplifying credit tightening. Hidden dependencies include bank lending standards, consumer delinquencies lagging employment, and market reliance on private labor signals. Trade implications: Favor a 2–4% tactical allocation to long-duration Treasuries (TLT/IEF) and 2–3% to LQD, size depending on yield triggers; enter puts on small-cap indices (IWM) or sell high-beta tech exposure (QQQ) via collar if labor prints worsen two months in a row. Use pair trades: long XLU (utilities) vs short XLY/XRT (consumer discretionary/retail) for 3–6 months; buy 3–6 month protective put spreads on QQQ or Feb-2026 10% OTM puts on IWM for tail protection. Time entries around Fed communications and monthly private labor indicators (ADP, Revelio, Indeed) — act if sequential two-month payroll trend <+25k. Contrarian angles: Consensus assumes easing is inevitable; miss is that sticky service inflation could keep policy tight and leave bonds vulnerable — bonds may be overpriced for a scenario where wages reaccelerate. Conversely, markets may underprice structural disinflation from AI and demographics, which would reward long-duration growth assets if realized. Historical parallels: 2015–16 tightening pauses show that partial easing can hit cyclicals differently and create multi-month dispersion; unintended consequence: premature cuts could reignite shelter/services inflation, forcing late hikes and generating big intra-year volatility.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25

Ticker Sentiment